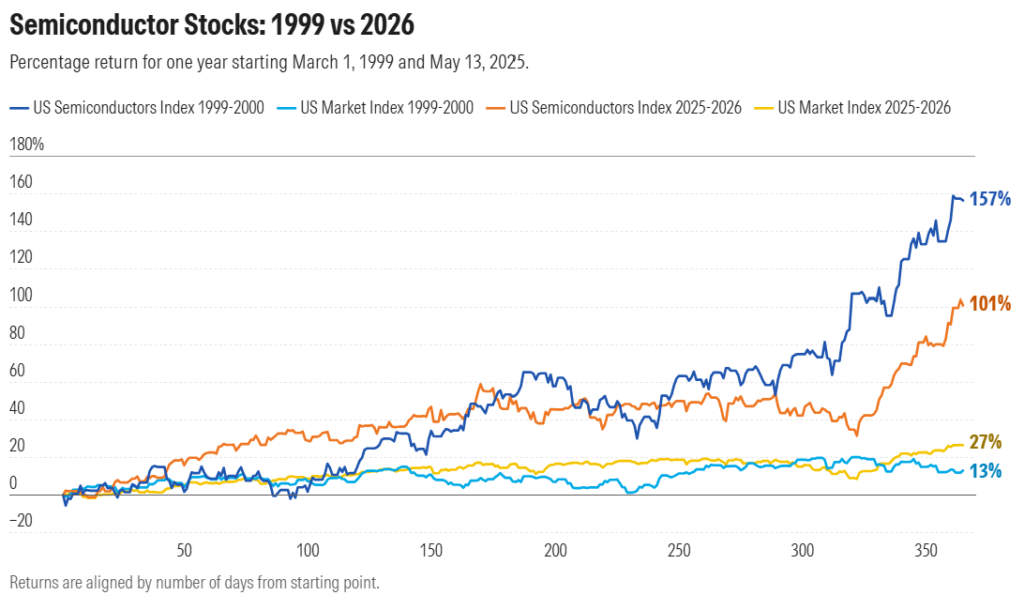

The latest AI rally is starting to bring back memories of 1999. Semiconductor stocks have surged, AI IPOs are exploding, and market leadership is increasingly concentrated in a small group of companies. But while comparisons to the dot-com era are growing, analysts argue today’s market may look stronger underneath the surface.

The contrast is becoming harder to ignore.

On one side: AI excitement, soaring chip stocks, and blockbuster IPOs.

On the other: Rising bond yields, inflation concerns, and growing pressure from higher oil prices.

AI Stocks Continue Dominating Returns

The scale of the rally has become remarkable. Among US stocks covered by Morningstar:

- 63 stocks gained more than 100% since the end of 2024

- Around half are directly tied to AI

- 18 stocks rose over 200%

- 8 gained more than 300%

- 9 of the top 10 performers are AI names

AI infrastructure remains the main driver. The strongest moves continue coming from: Chips, Data centers, AI hardware, Server infrastructure

Recent IPO activity reinforced the trend after Cerebras Systems surged sharply following its market debut.

Why Investors Keep Mentioning 1999

There are similarities. Like the internet boom, AI is viewed as a transformative technology with economy-wide impact.

Markets also show familiar signs:

- Leadership concentrated in a few companies

- High valuation multiples

- Infrastructure suppliers leading gains

But Morningstar analysts see one important difference.

Unlike the dot-com period, some AI leaders still appear supported by improving long-term growth expectations and higher fair value estimates.

That does not mean every stock is justified. Analysts warned that some hardware names may have moved too far ahead of fundamentals. Examples mentioned included: SanDisk, Micron Technology

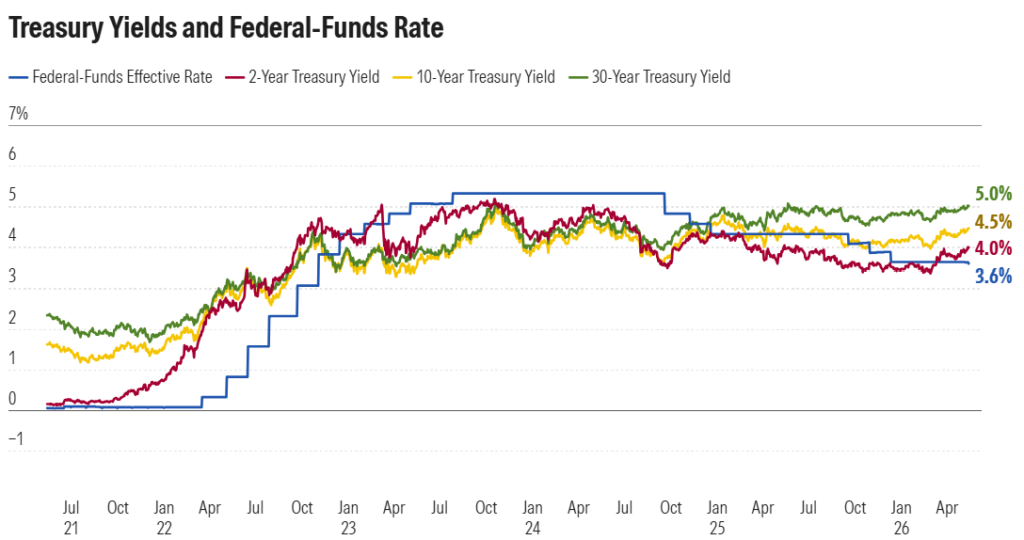

Bond Markets Are Sending a Different Message

While AI pushes stocks higher, bonds are moving the opposite way.

The 30-year Treasury yield moved above 5%, while the 10-year yield approached 4.6%, reaching the highest levels in about a year.

Inflation remains part of the story. But analysts say another issue is growing: More government debt issuance.

The US deficit is projected near $2 trillion in 2026, while total national debt approaches $39 trillion, increasing supply pressure in bond markets.

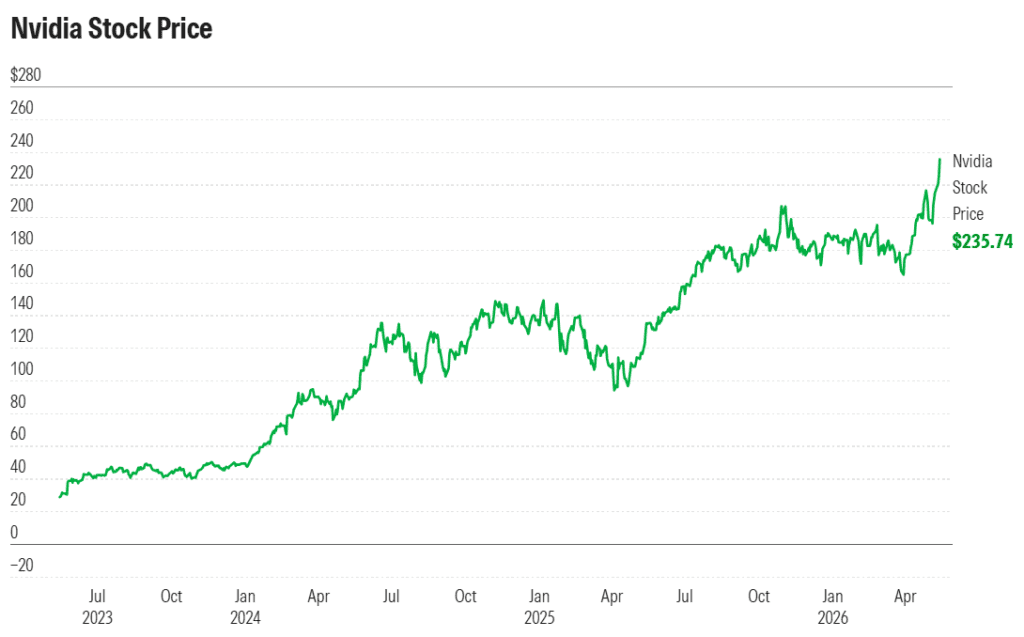

Nvidia Becomes the Next Test

Markets now turn toward NVIDIA earnings. Investors will watch:

- AI server demand

- Revenue progress toward long-term targets

- Supply-chain strength

- Whether another beat-and-raise quarter arrives

The company remains one of the biggest symbols of the AI trade.

Markets are still following AI. The difference now is that investors are asking a harder question:

Is this another bubble… or the early stage of a larger technology cycle?

Reference: Morningstar Markets Brief by Tom Lauricella and analysis from Dave Sekera and Brian Colello.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.