Inflation quietly erodes your investment returns, turning today’s gains into tomorrow’s losses. While markets rise, your purchasing power can still fall if inflation outpaces growth. The good news is you can protect your wealth using proven strategies that have worked across decades and economic cycles. This guide reveals how real estate, stocks, and gold serve as effective inflation hedges, backed by recent research showing which assets perform best during crisis and non-crisis periods. You’ll learn practical steps to build a resilient portfolio that preserves and grows wealth despite rising prices in 2026.

Table of Contents

- Understanding Inflation And Why Hedging Matters

- Assets And Strategies Proven To Hedge Inflation Effectively

- Preparing And Implementing Your Inflation Hedging Plan

- Monitoring, Common Pitfalls, And Optimizing Inflation Hedging

- Discover Tailored Inflation Hedging Insights And Strategies

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Real estate hedges inflation effectively | Property values and rents rise with inflation across various economic conditions |

| Stocks provide superior long-term protection | Equities outperform real estate in protecting against sustained inflation over time |

| Gold excels during economic crises | Precious metals preserve value when other assets become volatile or decline |

| Diversification optimizes portfolio resilience | Combining multiple asset classes balances protection across different economic phases |

| Understanding timing matters critically | Short-term and long-term inflation impacts require different hedging approaches |

Understanding inflation and why hedging matters

Inflation measures how much prices increase over time, typically tracked through the Consumer Price Index. When inflation runs at 3% annually, your $100,000 investment needs to earn at least 3% just to maintain its purchasing power. Many investors focus solely on nominal returns without considering how inflation affects investments and wealth preservation.

The difference between nominal and real returns determines your actual wealth growth. A stock portfolio returning 8% nominally only delivers 5% real return when inflation hits 3%. Bonds and cash holdings suffer even more, often producing negative real returns during high inflation periods. Your savings account earning 1% interest actually loses 2% in purchasing power when inflation reaches 3%.

Effective portfolio strategy requires incorporating inflation protection from the start. Common misconceptions include believing all assets naturally keep pace with inflation or that short-term price movements indicate long-term hedging effectiveness. Research shows specific assets consistently protect wealth while others fail during sustained inflation.

Key inflation impacts on your portfolio include:

- Fixed income investments lose value as future payments buy less

- Cash holdings steadily decline in purchasing power

- Stock valuations can compress despite revenue growth

- Real assets like property and commodities tend to appreciate

- International investments face currency devaluation risks

Assets and strategies proven to hedge inflation effectively

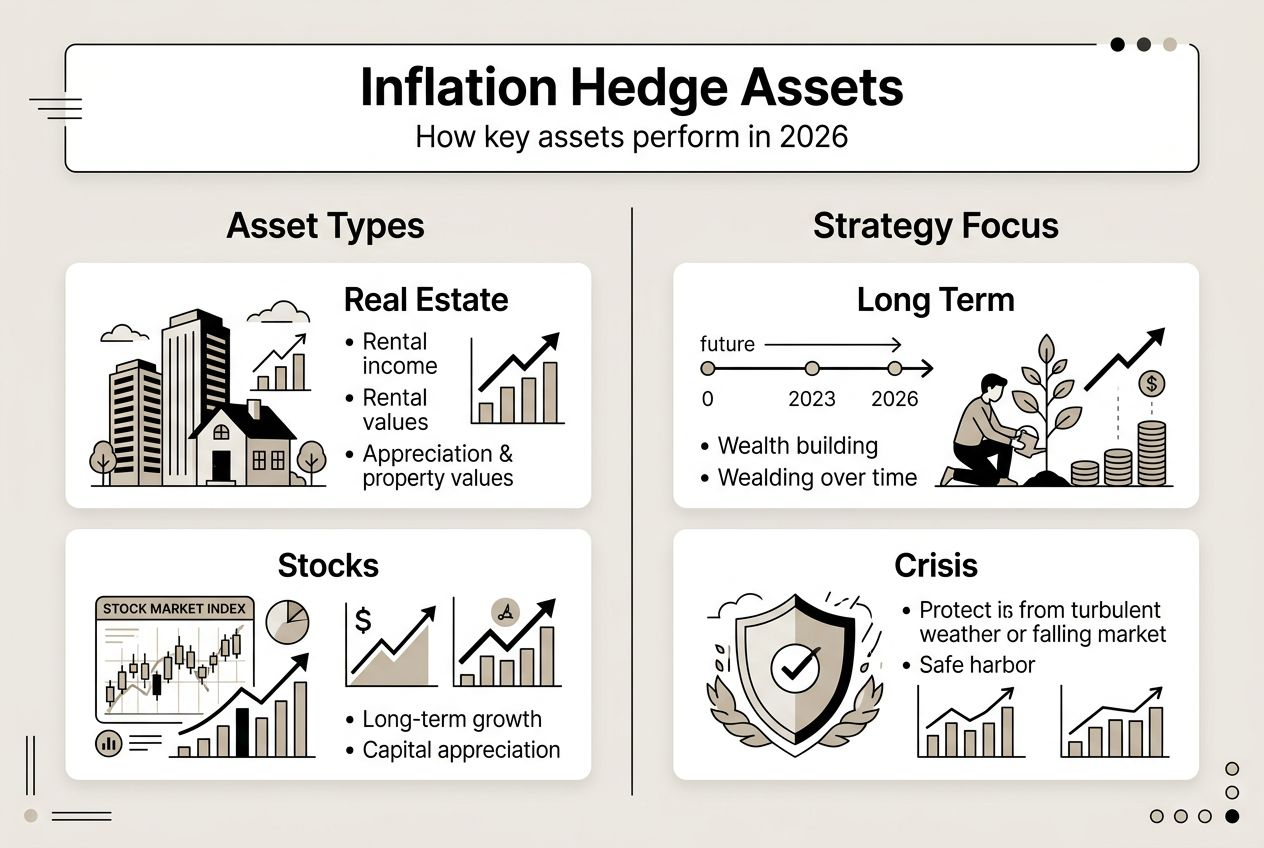

Real estate provides an effective hedge against inflation in the long run, during both crisis and non-crisis periods. Property values typically rise alongside general price levels, while rental income adjusts upward to reflect current market rates. This dual benefit makes real estate particularly attractive for investors seeking steady inflation protection.

Stocks deliver even stronger long-term inflation hedging than real estate, according to the same research. Companies can raise prices to maintain margins, and productive assets generate real economic value that compounds over time. While stock prices fluctuate more in the short term, equities consistently outperform property investments over extended periods when measuring real returns.

Gold serves as the ultimate crisis hedge, preserving wealth when economic uncertainty spikes. The precious metal shines brightest during downturns and periods of extreme inflation, offering protection when stocks and real estate stumble. However, gold produces no income and can underperform during stable economic growth phases.

| Asset Class | Short-Term Hedging | Long-Term Hedging | Crisis Performance | Non-Crisis Performance |

|---|---|---|---|---|

| Real Estate | Moderate | Strong | Strong | Strong |

| Stocks | Weak | Very Strong | Moderate | Very Strong |

| Gold | Strong | Strong | Very Strong | Moderate |

| Bonds | Weak | Very Weak | Moderate | Weak |

| Cash | Very Weak | Very Weak | Weak | Very Weak |

Pro Tip: Allocate across all three core hedging assets to balance protection regardless of economic conditions. A portfolio combining 40% stocks, 30% real estate, and 10% gold with 20% bonds provides robust inflation defense while maintaining growth potential.

The key to successful inflation investing strategies lies in understanding how each asset performs across different timeframes. Real estate delivers consistent protection, stocks excel over decades, and gold safeguards wealth during turbulent periods. Your inflation hedging investments guide should reflect these performance characteristics.

Consider how gold inflation hedge in recessions protects portfolios when other assets decline. During the 2008 financial crisis, gold prices surged while stocks and real estate plummeted. This inverse correlation provides essential portfolio stability during the times you need it most.

Diversification across inflation hedging assets creates a more resilient portfolio than concentrating in any single investment. Real estate generates income, stocks compound growth, and gold preserves capital. Together, they address inflation across all economic scenarios you’ll encounter over your investment lifetime.

Preparing and implementing your inflation hedging plan

Start by evaluating your current portfolio’s inflation exposure. Calculate what percentage sits in cash, bonds, stocks, real estate, and commodities. Most investors discover they hold too much in inflation-vulnerable assets like bonds and cash, leaving wealth exposed to purchasing power erosion.

Deciding allocation percentages requires balancing your timeline, risk tolerance, and economic outlook. Younger investors with 30-year horizons can emphasize stocks for superior long-term inflation protection. Those nearing retirement might increase real estate and gold exposure to reduce volatility while maintaining inflation defense.

Economic cycles and crisis periods demand different hedging approaches. During stable growth, stocks and real estate perform best. When recession threatens or inflation spikes unexpectedly, gold allocation becomes more valuable. Understanding long vs short term investing helps you match hedging strategies to your specific timeframe.

Monitoring and rebalancing maintains your intended inflation protection over time. Asset performance varies, causing allocations to drift from targets. Annual reviews ensure your portfolio remains properly hedged as market conditions evolve and your personal circumstances change.

Implementation steps for effective inflation hedging:

- Calculate current portfolio allocation across all asset classes

- Determine target percentages based on timeline and risk tolerance

- Research specific investments within each hedging category

- Execute purchases systematically to avoid market timing risks

- Document your strategy and rebalancing triggers

- Schedule quarterly reviews to track performance

- Adjust allocations when drift exceeds 5% from targets

- Consider tax implications before making changes

Pro Tip: Work with a financial advisor when adding complex assets like direct real estate investments. Professional guidance helps you avoid costly mistakes in property selection, financing, and management that can undermine inflation hedging benefits.

Your inflation portfolio strategy should evolve as economic conditions shift. The Federal Reserve’s monetary policy, government spending levels, and global supply chains all influence inflation trajectories. Staying informed allows you to adjust hedging tactics before major wealth erosion occurs.

Comparing real estate vs stocks reveals important tradeoffs. Real estate requires larger capital commitments, involves management responsibilities, and offers less liquidity. Stocks provide instant diversification, easy rebalancing, and lower transaction costs. Both deserve portfolio space for comprehensive inflation protection.

Effective inflation hedging requires understanding both short and long term portfolio impacts and current market conditions. What works during temporary inflation spikes differs from strategies needed for sustained price increases. Build flexibility into your plan to adapt as economic realities unfold.

Monitoring, common pitfalls, and optimizing inflation hedging

Recognizing when inflation hedges underperform helps you respond appropriately rather than panic. Gold might lag during strong economic growth, while stocks can struggle during stagflation. These temporary weaknesses don’t invalidate the assets’ long-term hedging value, but understanding normal performance patterns prevents overreaction.

Common mistakes undermine even well-intentioned hedging strategies. Overexposure to any single asset creates concentration risk that defeats diversification benefits. Neglecting how assets perform differently during crisis versus non-crisis periods leads to inappropriate allocations. Ignoring fees and transaction costs erodes returns, especially with actively managed real estate or gold investments.

Ongoing portfolio review and adjustment keeps your inflation hedging effective. Markets shift, personal circumstances change, and new investment options emerge. Quarterly check-ins identify drift from target allocations, while annual deep reviews assess whether your overall strategy still matches your goals and economic outlook.

| Scenario | Typical Performance | Recommended Action |

|---|---|---|

| Stable growth, low inflation | Stocks strong, gold weak | Maintain diversification, rebalance to targets |

| Rising inflation, strong economy | Real estate and stocks strong | Consider reducing bond exposure |

| Recession with deflation risk | Gold strong, stocks weak | Increase gold allocation temporarily |

| Stagflation environment | Real estate moderate, stocks weak | Balance all three core hedges equally |

| Recovery from crisis | Stocks surge, gold declines | Rebalance gains into lagging assets |

Understanding inflation hedge performance during crisis versus non-crisis times proves critical to avoiding pitfalls. Assets that protect wealth during economic turmoil often underperform during stable periods. This natural variation shouldn’t trigger constant portfolio changes that generate taxes and fees.

Pitfalls to avoid in inflation hedging:

- Chasing last year’s best performing asset class

- Abandoning strategies during temporary underperformance

- Ignoring tax consequences of frequent rebalancing

- Overweighting gold beyond 10 to 15% of portfolio

- Neglecting international diversification within stock holdings

- Assuming past inflation patterns predict future trends

- Failing to account for personal spending inflation rates

- Using leveraged investments without understanding risks

Optimizing your inflation hedging means finding the right balance between protection and growth. Pure preservation through gold and cash guarantees you won’t keep pace with productive economy growth. Pure growth through stocks leaves you vulnerable during inflationary crises. The optimal mix provides adequate protection without sacrificing long-term wealth building.

Tax efficiency enhances inflation hedging effectiveness. Real estate offers depreciation deductions, stocks provide long-term capital gains treatment, and gold held over one year qualifies for preferential rates. Structuring your hedging strategy within appropriate account types maximizes after-tax real returns.

Staying disciplined through market volatility separates successful inflation hedgers from those who abandon strategies at the worst times. When stocks plunge during a crisis, your gold holdings should rise. When gold stagnates during growth periods, your stocks should surge. Trust the diversification to work across complete economic cycles rather than reacting to short-term movements.

Discover tailored inflation hedging insights and strategies

Finblog provides comprehensive guides and expert analysis to help you navigate inflation challenges and protect your wealth in 2026. Our research-backed insights translate complex economic concepts into actionable strategies you can implement immediately. Whether you’re building your first inflation-hedged portfolio or optimizing an existing strategy, Finblog investment insights deliver the knowledge you need.

Access practical wealth protection strategies that address your specific financial situation and goals. Our expert team analyzes current market conditions, economic trends, and asset performance to provide timely guidance. Build a resilient portfolio using our expert inflation hedging guide that combines proven principles with current opportunities.

Frequently asked questions

How can I use real estate to hedge against inflation effectively?

Real estate hedges inflation by appreciating asset values and rental income adjustments, effective in various market conditions. Diversify across property types like residential, commercial, and REITs to optimize protection. Geographic diversification reduces regional economic risks while maintaining broad inflation hedging benefits.

What role does gold play in an inflation-hedged portfolio?

Gold offers reliable long-run protection primarily during economic crises and downturns. It preserves value when stocks and real estate become volatile, acting as portfolio insurance. Limit gold to 10 to 15% of total assets and complement it with income-producing investments for balanced protection and growth.

How often should I rebalance my inflation-hedged portfolio?

Rebalance at least annually or after major economic changes that shift asset allocations beyond 5% from targets. Regular reviews ensure your portfolio remains aligned with both inflation protection goals and personal financial objectives. Quarterly monitoring helps you identify when rebalancing becomes necessary without triggering excessive trading costs.

Can bonds provide any inflation protection in 2026?

Traditional bonds struggle during inflation as fixed payments lose purchasing power. Treasury Inflation-Protected Securities adjust principal values with CPI changes, offering some defense. Consider TIPS for the bond portion of your portfolio, but recognize stocks and real estate provide superior long-term inflation hedging.

Should I adjust my inflation hedging strategy as I approach retirement?

Yes, shift toward more stable hedges like real estate and increase gold allocation slightly as retirement nears. Reduce stock concentration to lower volatility while maintaining enough equity exposure for long-term growth. Your portfolio still needs inflation protection for 20 to 30 years of retirement spending.