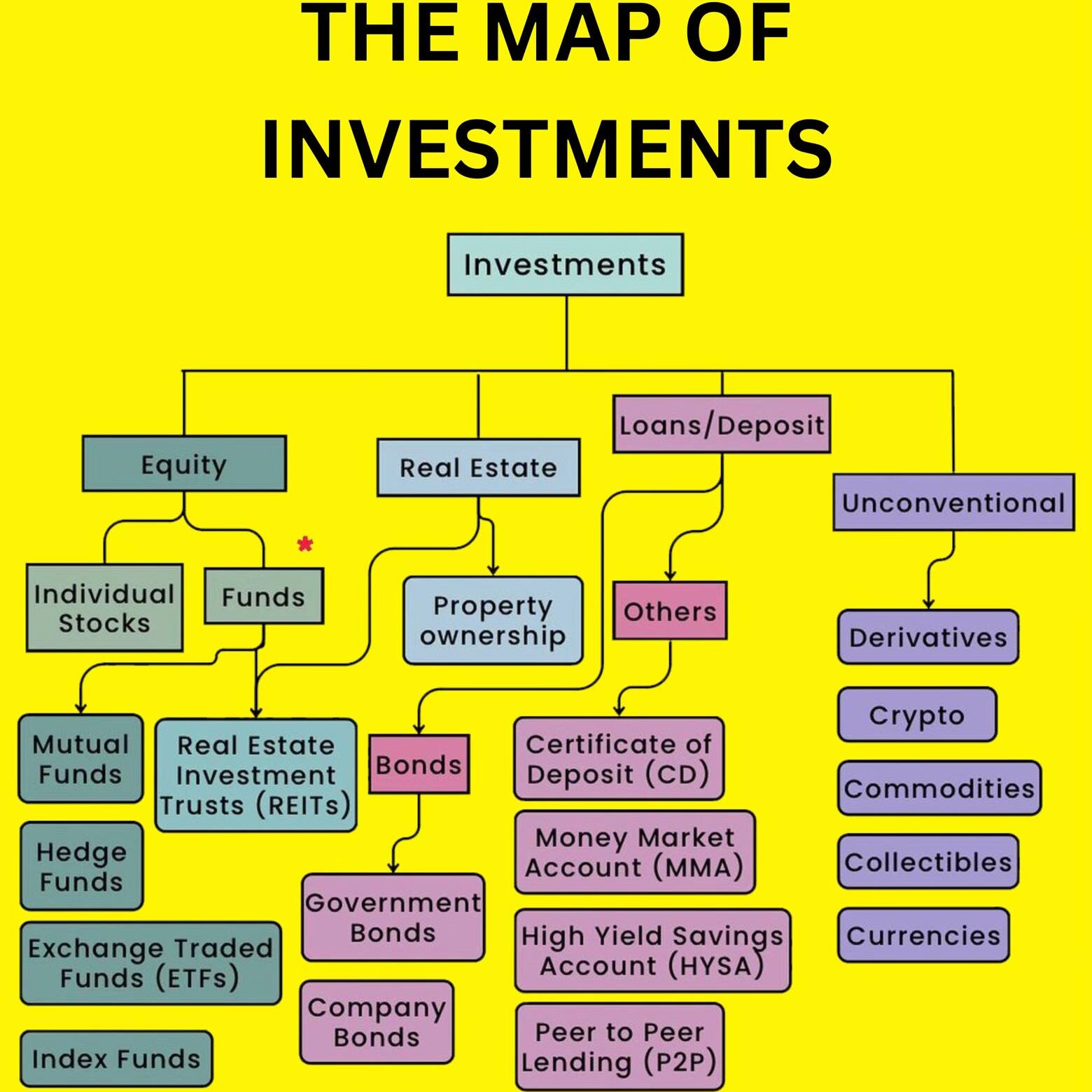

CD vs. mutual fund — both are popular investment options, but which suits your financial goals? Certificates of Deposit (CDs) offer stability and guaranteed returns, while mutual funds provide growth potential but come with risks. Here’s an in-depth look at their differences, benefits, and risks.

What Is a CD (Certificate of Deposit)?

A Certificate of Deposit (CD) is a savings product offered by banks and credit unions. When you invest in a CD, you agree to lock in your money for a fixed term in exchange for a guaranteed interest rate.

Features of CDs:

- Guaranteed Returns: Fixed interest rates that remain constant for the term.

- Low Risk: FDIC-insured up to $250,000 per depositor, per bank.

- Liquidity Limitations: Early withdrawals incur penalties.

Example: If you invest $10,000 in a 2-year CD at 4%, you’ll earn $800 in interest by the end of the term.

| Advantages | Disadvantages |

|---|---|

| Safe and predictable returns | Limited liquidity |

| No market volatility | Lower long-term growth |

| Insured by the FDIC | Penalties for early access |

What Is a Mutual Fund?

A mutual fund pools money from multiple investors to buy a diversified portfolio of stocks, bonds, or other securities. Managed by professionals, mutual funds aim to achieve higher returns over the long term.

Features of Mutual Funds:

- Growth Potential: Suitable for long-term goals like retirement.

- Risk Exposure: Returns are not guaranteed and depend on market performance.

- Diversification: Reduces risk by spreading investments across various assets.

Example: Investing $10,000 in a mutual fund with an average annual return of 7% can grow to $14,025 in 5 years (assuming compounding).

| Advantages | Disadvantages |

|---|---|

| Higher growth potential | Subject to market risks |

| Professional management | Management fees and expenses |

| Diversification | Returns not guaranteed |

CD vs. Mutual Fund: Key Differences

| Factor | Certificate of Deposit (CD) | Mutual Fund |

|---|---|---|

| Risk | Minimal risk, FDIC-insured | Subject to market fluctuations |

| Returns | Fixed and predictable | Variable, depending on market performance |

| Liquidity | Restricted during the term, penalties for early withdrawals | Generally liquid but may involve exit charges |

| Time Horizon | Best for short- to medium-term savings | Ideal for long-term investment goals |

| Management | No active management needed | Professionally managed |

| Insurance | Protected by FDIC or NCUA | No insurance against loss |

Suitability: Who Should Choose CDs vs. Mutual Funds?

CDs Are Ideal For:

- Conservative Investors: Those who prioritize safety over high returns.

- Short-Term Goals: Perfect for saving money for near-term needs like a down payment or tuition.

- Low-Risk Tolerance: Investors who want guaranteed returns without market exposure.

Mutual Funds Are Ideal For:

- Growth-Oriented Investors: Those willing to accept risks for higher returns.

- Long-Term Goals: Suitable for retirement planning or wealth building over decades.

- Diversification Seekers: Investors looking to spread risk across multiple asset classes.

Risk and Return Comparison

| Investment | Risk Level | Potential Returns |

|---|---|---|

| CDs | Low | Typically 2%–5% annually |

| Equity Mutual Funds | High | 7%–10% or more, on average |

| Bond Mutual Funds | Moderate | 4%–6%, depending on interest rates |

For instance, during a market downturn, CDs continue to deliver guaranteed returns, while mutual funds may lose value.

Tax Implications

- CDs:

- Interest earned is taxed as ordinary income.

- Taxes are paid annually, even if the interest is not withdrawn.

- Mutual Funds:

- Dividends and capital gains are taxable.

- Tax-advantaged accounts like IRAs can defer or eliminate tax liabilities.

Recent Trends in 2024

- CD Rates Increasing: Rising interest rates in 2024 have made CDs more attractive, with yields exceeding 5% for long-term CDs.

- Mutual Fund Innovations: ESG (Environmental, Social, and Governance) mutual funds are gaining popularity, offering ethical investment options with competitive returns.

How to Choose Between a CD and a Mutual Fund

- Define Your Goals:

- Short-term savings? CDs are better.

- Long-term wealth-building? Opt for mutual funds.

- Assess Your Risk Tolerance:

- Low risk: CDs.

- High risk but higher returns: Mutual funds.

- Consider Liquidity Needs:

- Need frequent access to funds? Avoid CDs.

- Flexible investments? Mutual funds provide liquidity.

- Understand Fees and Penalties:

- CDs: Early withdrawal penalties.

- Mutual Funds: Management fees and possible exit charges.

Example Scenarios

- Retirement Planning: A young professional saving for retirement may benefit from mutual funds due to their growth potential.

- Emergency Savings: CDs are better for parking emergency funds you don’t want exposed to market risks.

- Balancing Portfolios: Combining CDs and mutual funds can balance safety and growth, catering to short- and long-term financial goals.

Related articles:

- What percent of 18-29-year-olds are investing in the stock market?

- Why is it important to start investing as early as possible?

- How Much Money Should You Have Saved by Age 30?

- Common Mistakes People Make When Investing and How to Avoid Them

- Behaviors That Prevent Smart Investing Decisions and How to Overcome Them

- How to Get a Startup Business Loan with No Money Online: A Step-by-Step Guide

- How to Invest in Gold and Silver: A Step-by-Step Guide

- How To Invest $1,000 And Grow Your Money in 2025

Sources: