TL;DR:

- Most investors mistakenly see dividends as free money rather than a transfer of value.

- Understanding dividend dates and metrics like yield, payout ratio, and growth rate is crucial for smart investing.

- Successful dividend strategies focus on business quality, sustainability, and reinvestment rather than chasing high yields.

Most investors assume dividends are a bonus, a little extra cash that shows up in your account for doing nothing. But 75% of investors fundamentally misunderstand how dividends actually work, treating them as free money when they’re really just a transfer of value. When a $100 stock pays a $5 dividend, the stock price drops to $95. Your total value hasn’t changed yet. What matters is what happens next, specifically how you use that income strategically to build real, lasting wealth. This guide walks you through everything you need to know to invest smarter with dividends.

Table of Contents

- What are dividends and how do they work?

- Types of dividends and how investors benefit

- Dividend metrics: Yield, payout ratio, and growth rate

- Dividend investing strategies and portfolio impact

- Why most investors misunderstand dividends (and how to get real value)

- Take your dividend knowledge further

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Dividends explained | Dividends are profit payments to shareholders and not ‘free money’ as stock prices adjust when paid. |

| Types and strategies | Cash, stock, and special dividends offer multiple ways to earn or compound gains based on your investing approach. |

| Smart metrics matter | Dividend yield, payout ratio, and growth rate reveal sustainable investment opportunities—avoid risky high yields. |

| Portfolio benefits | Dividend investing cushions income, lowers risk, and can boost long-term returns with the right strategies. |

What are dividends and how do they work?

Dividends are one of the oldest wealth-building tools in investing, but they’re surprisingly misunderstood. At their core, dividends are periodic payments companies make to their shareholders, drawn from company profits. Think of it like owning a small slice of a business. When that business earns money, it has two basic options: reinvest the profits back into growth or share them with the owners. When a company chooses to share them, that’s a dividend.

Understanding how dividends work goes deeper than just receiving cash in your brokerage account. Most dividend-paying companies distribute payments on a quarterly schedule, though some pay monthly or annually. The form of the payment can also vary.

Here are the most common dividend formats:

- Cash dividends: The most straightforward form. Money is deposited directly into your brokerage account on the payment date.

- Stock dividends: Instead of cash, you receive additional shares. This dilutes the share price slightly but doesn’t require the company to spend cash.

- Property dividends: Rare, but some companies distribute physical assets or subsidiary shares.

- Liquidating dividends: Paid when a company winds down operations, returning capital to shareholders.

The four dates every dividend investor must know

The calendar around dividends trips up a lot of new investors. Miss one key date and you could buy a stock expecting a dividend and receive nothing. Here’s how it breaks down:

| Date | What it means |

|---|---|

| Declaration date | Company officially announces the dividend amount and key dates |

| Ex-dividend date | You must own shares before this date to qualify for the dividend |

| Record date | Company finalizes the list of eligible shareholders (usually 1 day after ex-date) |

| Payment date | Dividend is actually deposited into your account |

The ex-dividend date is the most critical for investors. If you buy shares on or after that date, you won’t receive the upcoming dividend. And here’s something many investors don’t expect: the stock price is adjusted downward by roughly the dividend amount on the ex-dividend date. This is the market’s way of accounting for the value leaving the company. It’s not a loss, it’s a redistribution.

Understanding dividend investing basics from the ground up helps you avoid the most common timing mistakes and sets a solid foundation for every strategy we’ll discuss next.

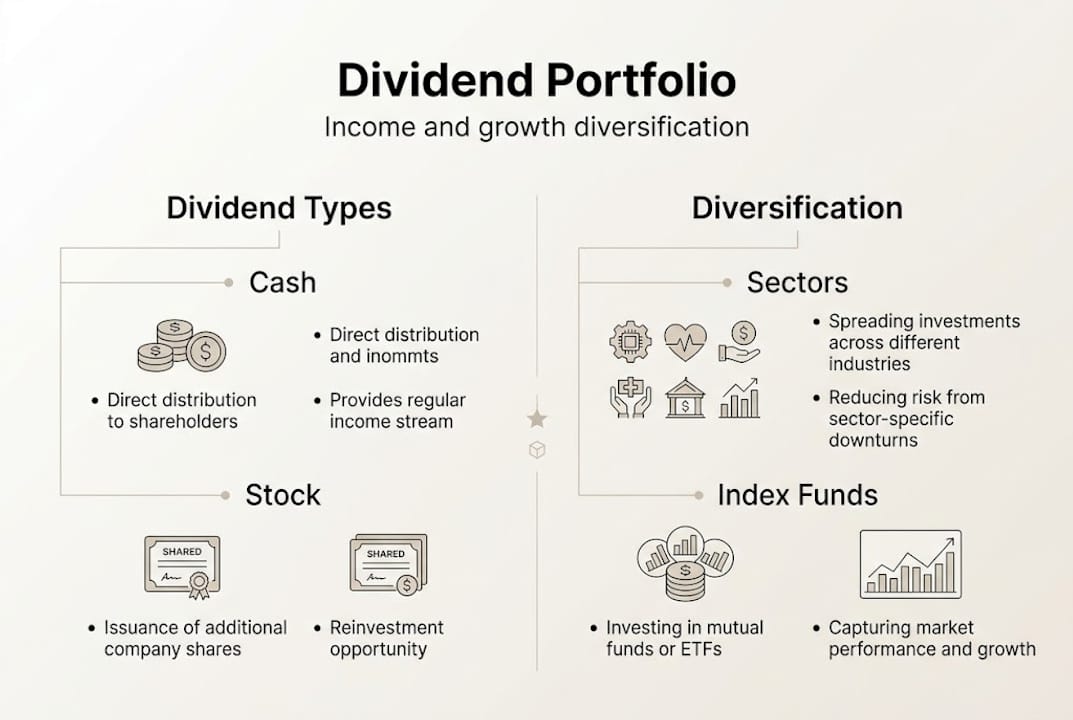

Types of dividends and how investors benefit

With a clear grasp of basic mechanisms, let’s explore the different types of dividends and how you can use them to your advantage.

Not all dividends serve the same purpose, and knowing the distinction can meaningfully change how you structure your portfolio. The two primary forms are cash and stock dividends, but the more important question is what you do with them once you receive them.

According to iShares, dividend options for investors include withdrawing the cash for living expenses, reinvesting via a Dividend Reinvestment Plan (DRIP) to compound returns, or redirecting the funds into other investments. Each approach serves a different financial goal.

The power of DRIP: A DRIP automatically uses your dividend payment to purchase additional shares, often at no commission and sometimes at a slight discount. Over 20 or 30 years, this compounding effect can be dramatic. You earn dividends on a larger share base, which generates even more dividends. It’s a snowball effect that rewards patience.

Beyond the standard cash and stock forms, there are other types investors should recognize:

- Special dividends: One-time payments companies issue when they’ve accumulated excess cash. They’re not recurring, so don’t build them into your income expectations.

- Preferred dividends: Paid to holders of preferred shares before any common stock dividends. These are often fixed and guaranteed by contract, making them more like bond interest than equity income.

- Dividend cuts: When a company reduces or eliminates its dividend, it’s almost always a red flag. Markets react sharply because a cut signals that management no longer trusts its own cash flow.

Professor Aswath Damodaran’s research highlights a concept called sticky dividend policy, where mature companies maintain or raise dividends out of habit or shareholder pressure, even when earnings no longer support the payout. This “me-tooism” leads to unsustainable payouts that eventually collapse. For investors trying to earn passive income reliably, spotting these sticky payout patterns early is essential.

Pro Tip: Before buying a dividend stock, look at how the dividend has behaved over the last two or three economic downturns. A company that maintained or grew its payout during recessions is far more reliable than one that doubled its yield in the last bull market.

| Dividend type | Reliability | Best for |

|---|---|---|

| Cash dividend | High (if earnings stable) | Income-focused investors |

| Stock dividend | Moderate | Growth-focused investors |

| Special dividend | Low (one-time) | Windfall capture, not planning |

| Preferred dividend | Very high (contractual) | Conservative, bond-like exposure |

Dividend metrics: Yield, payout ratio, and growth rate

Now that you know the types and payout methods, let’s decode the numbers that reveal the real quality of dividend stocks.

Numbers don’t lie, but they can mislead if you don’t know what you’re looking at. Three metrics separate confident dividend investors from those chasing yield into traps.

1. Dividend yield

This is calculated as the annual dividend divided by the current stock price. A stock paying $4 per year that trades at $80 has a 5% yield. Simple. But yield moves in two directions: it rises when the dividend increases or when the stock price falls. A rising yield caused by a falling stock price is often a warning sign, not an opportunity.

2. Payout ratio

This tells you what percentage of earnings a company pays out as dividends. According to Motley Fool, the ideal payout ratio sits between 30% and 60%. Below 30% suggests the dividend has room to grow. Above 70% raises sustainability questions. Above 100% means the company is paying out more than it earns, which can’t continue indefinitely.

3. Dividend growth rate

This measures how fast a company increases its dividend year over year. A company growing its dividend by 7% annually will double its payout in roughly a decade. For long-term investors, a moderate, growing dividend often outperforms a high, static one.

Here’s how to use these three metrics together in practice:

- Screen for a yield between 2% and 5%. Anything above 7 to 8% deserves extra scrutiny.

- Check the payout ratio. If it’s above 70%, ask why. Is it a stable utility, or a declining business propping up its dividend?

- Review the five-year dividend growth rate. Consistent growers signal management confidence in future cash flows.

- Compare dividend growth to earnings growth. If dividends are growing faster than earnings for years, that’s a warning sign.

- Cross-check with free cash flow. Earnings can be manipulated; cash flow is harder to fake.

Key stat: Reinvested dividends account for roughly 40% of long-term stock market returns, and dividend-paying stocks have historically shown lower volatility than non-payers. The US median payout ratio hovers near 35%, reflecting a balance between rewarding shareholders and funding growth.

Pro Tip: Don’t evaluate yield in isolation. Always pair it with the payout ratio and free cash flow coverage. A 3.5% yield from a company with a 40% payout ratio and 10 years of dividend growth is far superior to a 7% yield from a company paying out 90% of erratic earnings.

Thinking about building a steady income strategy around dividends? Understanding these three metrics is your starting point. Combined with smart portfolio diversification benefits, dividend metrics help you construct a portfolio that balances growth and safety.

Dividend investing strategies and portfolio impact

Once you understand how to evaluate dividends, the next step is using them as strategic tools within your investment portfolio.

Strategy makes the difference between investors who collect modest income and those who systematically build wealth. The following approaches are proven, practical, and adaptable to different risk tolerances and timelines.

Dividend aristocrats: These are companies in the S&P 500 that have increased their dividend for 25 or more consecutive years. Names like Johnson & Johnson, Procter & Gamble, and Coca-Cola have maintained rising payouts through recessions, financial crises, and pandemic shutdowns. They won’t deliver explosive growth, but they offer consistency that’s genuinely rare.

Sector diversification: Dividend income tends to concentrate in a few sectors if you’re not careful. Utilities, consumer staples, healthcare, and real estate investment trusts (REITs) are the heaviest dividend payers. Dividend-paying stocks in these sectors are typically mature, stable firms that generate predictable cash flows. The risk? These sectors can underperform during bull markets driven by tech growth. A thoughtful blend prevents over-concentration.

Blending dividends with index funds: You don’t have to choose between dividend stocks and broad market exposure. Many investors hold a core index fund for growth and add a dividend-focused ETF or a selection of individual dividend payers for income. This hybrid approach captures both market returns and income stability.

Tax strategy matters: Qualified dividends, those paid by U.S. companies and held for a sufficient period, are taxed at 0%, 15%, or 20%, depending on your income bracket. Ordinary dividends are taxed as regular income, which can be significantly higher. This makes account placement critical. REITs and master limited partnerships (MLPs), which require tax-advantaged accounts like IRAs to shelter their less favorable dividend treatment, should generally not sit in taxable brokerage accounts.

Key strategies at a glance:

- Prioritize companies with payout ratios below 60% and free cash flow coverage above 1.5x

- Diversify across at least three to four dividend-heavy sectors to reduce concentration risk

- Hold REITs and high-income securities in tax-advantaged accounts when possible

- Focus on total return (price appreciation plus dividends) rather than yield alone

- Reinvest dividends during accumulation years; switch to withdrawals in retirement

“Dividend stocks often provide lower volatility and an income cushion that pure growth stocks simply cannot match, particularly during bear markets when price appreciation reverses but dividends may continue flowing.”

Learning to diversify investments strategically while incorporating dividends is where investing shifts from reactive to intentional. Smart investors also look at how to diversify investments naturally across asset classes, not just within dividend stocks.

Why most investors misunderstand dividends (and how to get real value)

Here’s the uncomfortable truth: most people who invest in dividend stocks are doing it for the wrong reasons, or with the wrong mental model.

As noted earlier, 75% of investors believe dividends are essentially free money. They buy high-yield stocks expecting a windfall, not realizing the stock price adjusts to reflect the outflow. The real value of dividends isn’t the cash itself, it’s what that cash becomes when you put it back to work over time.

The investors who truly win with dividends aren’t chasing 9% yields. They’re building positions in companies with moderate, growing, sustainable payouts and reinvesting every dollar during their wealth-building years. They understand that a 3% yield growing at 8% annually beats a 7% static yield from a struggling company within just a few years.

Another mistake we see constantly: treating dividends as a substitute for a growth strategy. Dividends work best as a complement to a broader plan. By themselves, they won’t build a retirement portfolio. Paired with compounding, sector diversification, and a long time horizon, they become a genuinely powerful force.

Our view at Finblog is that the smartest dividend investors focus first on business quality, second on dividend sustainability, and third on yield. In that exact order. A mediocre business paying a fat dividend will eventually hurt you. A great business paying a modest, growing dividend will reward you for decades.

Explore winning diversification strategies to see how dividend investing fits into a complete portfolio framework for 2026 and beyond.

Take your dividend knowledge further

Dividends are one piece of a larger investing puzzle, and understanding them deeply gives you a real edge over the majority of investors who still treat them as an afterthought. Whether you’re building an income-generating portfolio, optimizing for tax efficiency, or just starting to explore equity investing, the principles in this guide give you a strong foundation.

At Finblog, we publish practical, evidence-backed resources designed specifically for investors like you. If you want to go deeper, our dividend guide for beginners walks through the full investment process, from screening your first dividend stock to building a diversified income portfolio. Sign up for our newsletter to get the latest insights delivered directly to your inbox.

Frequently asked questions

What are dividends and who pays them?

Dividends are periodic payments companies make to shareholders from their profits, and they’re most commonly paid by mature, stable businesses with predictable cash flows.

How do I know if I’ll receive a dividend?

You must own shares before the ex-dividend date to qualify; companies publish all four key dates (declaration, ex-dividend, record, and payment) well in advance.

Can dividends grow over time?

Yes. “Dividend aristocrats” have increased dividends for 25 or more years consecutively, and companies with consistent earnings growth often raise their payouts annually.

Are dividends taxed differently?

Qualified dividends are taxed at preferential rates of 0%, 15%, or 20%, while ordinary dividends are taxed as regular income, making account placement a key part of your strategy.

Is it risky to buy stocks just for high dividends?

Very. Yields above 8% are frequently warning signs of unsustainable payouts or a declining stock price, and chasing them often leads to dividend cuts and capital losses.