TL;DR:

- The time value of money shows that a dollar today is worth more than in the future.

- Comparing cash flows requires adjusting for time, interest rates, and inflation.

- Applying TVM consistently helps improve saving, investing, and borrowing decisions.

Most people assume a dollar is always a dollar, no matter when they get it. That assumption costs them thousands over a lifetime. The time value of money (TVM) is one of the most powerful ideas in personal finance, and it shapes every decision from choosing a savings account to evaluating a loan offer. Once you understand that money today is worth more than the same amount in the future, you stop making comparisons on face value alone. This article breaks down TVM clearly, shows you the core math, and walks through real decisions where applying it gives you a serious edge.

Table of Contents

- What is the time value of money?

- Core concepts: present value, future value, and rates

- How to compare cash flows at different times

- Everyday applications: TVM in your personal finance decisions

- Why most people undervalue the time value of money (and how to fix it)

- Ready to master TVM and upgrade your finances?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| A dollar today is worth more | Money received sooner can be invested or spent for greater value than the same amount later. |

| Always adjust for timing | You must bring all cash flows to a common date before making financial comparisons. |

| TVM powers better decisions | Understanding TVM helps you choose smarter strategies for investing, borrowing, and saving. |

| Small rates make a big difference | Even modest interest rates or inflation can dramatically change the value of money over time. |

What is the time value of money?

The time value of money is the principle that a dollar in your hand today is worth more than a dollar you’ll receive a year from now. This isn’t just theory. It reflects three real forces working on every dollar you own or owe.

Why does TVM exist? Here are the three core reasons:

- Inflation quietly erodes purchasing power. What costs $100 today may cost $103 next year.

- Investment opportunity means money you hold now can be put to work immediately, generating returns.

- Risk increases over time. A payment promised in the future carries more uncertainty than one already in your hand.

Think of it this way: if a friend owes you $500, would you rather they paid you today or two years from now? Today, clearly. You could deposit it, invest it, or use it immediately. Waiting means losing all the value that money could have created in the meantime.

This is also why loan interest exists. When a bank lends you money, they are giving up today’s value. The interest you pay is their compensation for that tradeoff.

The math behind TVM is built on compound interest, where interest earns interest over time. TVM calculations rely on compound interest and the need to move payments to a common point in time. That movement is what makes fair comparisons possible.

“Compounding and discounting are two sides of the same coin. Move money forward with interest, or move it backward to find today’s value.” This is the engine that makes TVM calculations work.

Many people fall into traps because they ignore TVM when making financial choices. You can avoid those traps by reading up on personal finance myths that quietly drain wealth over time.

Pro Tip: Never compare two cash flows at different points in time without first adjusting both to the same date. Comparing raw numbers across time leads to bad decisions every time.

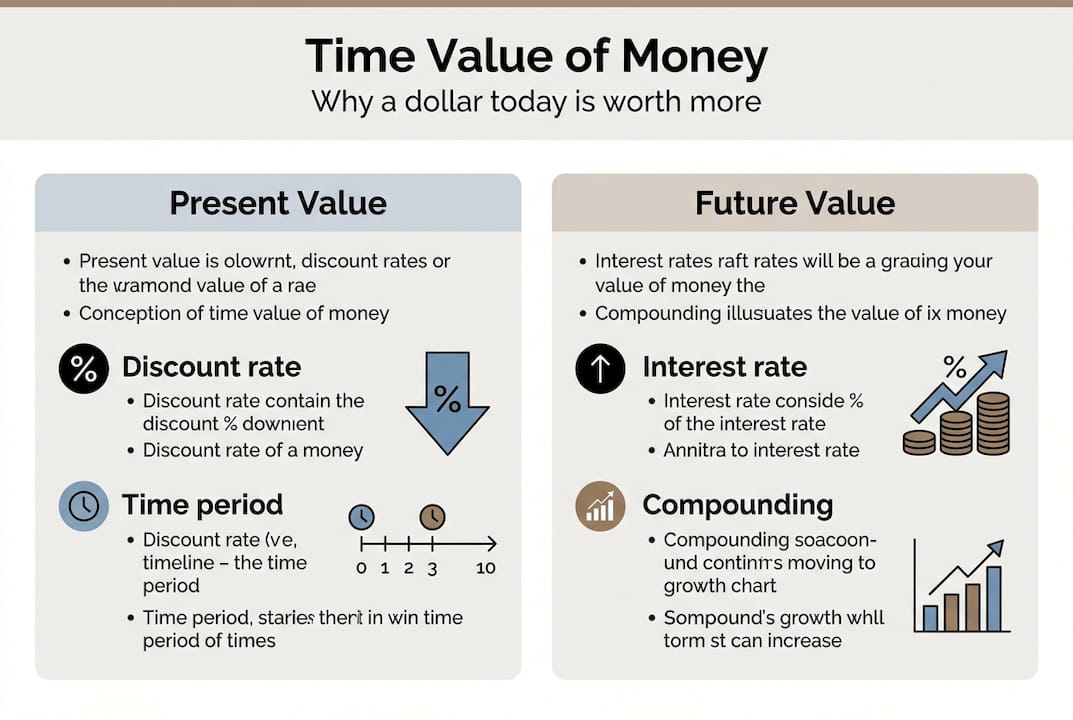

Core concepts: present value, future value, and rates

With a clear grasp on why TVM matters, you’ll need to understand the core concepts and math behind it.

Present value (PV) is what a future sum of money is worth today, after accounting for interest or inflation. Future value (FV) is how much a sum of money today will grow into by a specific future date, given a set rate.

Think of PV and FV as two directions on the same timeline. Compounding moves money forward (today to future). Discounting moves it backward (future to today).

The interest rate is the price of time. A higher rate means money grows faster, and it also means future payments are worth less in today’s terms. Rate selection matters enormously. Even a one or two percentage point difference compounds into thousands of dollars over a decade.

Here is what $100 today grows to at a 5% annual interest rate:

| Time period | Future value at 5% |

|---|---|

| Today (Year 0) | $100.00 |

| After 1 year | $105.00 |

| After 3 years | $115.76 |

| After 5 years | $127.63 |

That 27.6% gain over five years comes from doing nothing but applying TVM correctly. Now imagine that rate applied to a retirement account over 30 years.

To calculate PV or FV, follow these steps:

- Identify the cash amount you want to evaluate.

- Choose the interest or discount rate that reflects opportunity cost or inflation.

- Count the number of time periods (usually years).

- Apply the formula: FV = PV x (1 + r)^n, or rearrange for PV.

- Interpret the result in context of your decision.

As the BOE Training resource confirms, you must use a common date and rate to compare cash flows meaningfully. Without that discipline, the numbers are misleading.

When developing an investment strategy, your choice of discount rate should reflect realistic returns for your risk tolerance. For context, explore personal finance trends to see how rate environments are shifting and how they affect TVM calculations. Pairing this knowledge with the right financial planning tools makes the math far easier to apply.

How to compare cash flows at different times

Once you’ve mastered the basics, you’ll often need to compare different payment or investment options in real life.

The most common mistake is comparing raw numbers across time. If someone offers you $1,000 today or four payments of $300 per year starting now, which is better? At face value, the payments total $1,200. But TVM changes everything.

Unequal cash-flow timing means you need to convert to present or future value before comparing. Once you discount those four $300 payments back to today at a 5% rate, their combined present value is closer to $1,063. The lump sum of $1,000 today, once invested at 5%, may surpass that figure depending on what you do with it.

Here is a simplified comparison at a 5% discount rate:

| Option | Nominal total | Present value |

|---|---|---|

| $1,000 lump sum today | $1,000 | $1,000 |

| Four $300 annual payments | $1,200 | ~$1,063 |

The payment stream looks richer on paper, but the gap narrows significantly once you account for time.

Common mistakes people make when comparing cash flows:

- Comparing nominal totals instead of time-adjusted values

- Forgetting that early payments are worth more than later ones

- Using the wrong discount rate for the risk level involved

- Ignoring inflation when dealing with long time horizons

Understanding this also connects to the debate around timing the market, where the same logic applies: when you put money to work matters as much as how much you put in. Before acting on any comparison, evaluating investment opportunities with TVM as your framework leads to smarter outcomes.

Pro Tip: When presented with different payment structures, always bring every option to the same value date before comparing. That single habit eliminates most financial comparison errors.

Everyday applications: TVM in your personal finance decisions

Knowing how to use TVM in comparisons is powerful. Now see how it helps with your own money decisions.

TVM is not just for finance professionals. It applies every time you choose between spending now versus saving, taking a loan versus paying cash, or accepting a bonus in installments versus a lump sum. TVM applies to common decisions like saving, investing, and choosing loans.

Here are four everyday decisions shaped by TVM:

- Choosing a loan offer. A lower monthly payment is not always cheaper. TVM reveals the total cost once you factor in the rate and term.

- Evaluating a job bonus. A $10,000 lump sum today beats $10,000 paid over five years in almost every TVM calculation.

- Deciding whether to pay off debt or invest. If your loan rate is 7% and your expected investment return is 9%, TVM favors investing. Reverse those numbers and the math changes completely.

- Planning for retirement. Starting five years earlier can double your outcome because of compounding. TVM makes that concrete, not just motivational.

Two pitfalls derail most people here. First, they ignore inflation. A payment you’ll receive in 10 years should be discounted not just for opportunity cost but also for the purchasing power it will lose. Second, they forget opportunity cost. Every dollar sitting idle is a dollar not growing.

Explore short-term investment options if you want to put idle cash to work quickly. For a broader view, understanding how to set financial priorities helps you decide where TVM logic applies most urgently. And if you’re still deciding between holding cash or investing, the saving vs investing breakdown is worth reading before you act.

Pro Tip: Free online TVM calculators let you plug in your rate, periods, and cash amounts in seconds. Use them before any financial decision involving payment timing.

Why most people undervalue the time value of money (and how to fix it)

Here is the uncomfortable truth: most people treat TVM as a classroom concept, not a daily tool. They think it only matters to portfolio managers or CFOs. It doesn’t. Every time you delay investing, accept deferred payment without asking for more, or compare loan offers by monthly payment alone, you are ignoring TVM and paying for it quietly.

The deeper issue is that the losses are invisible. Inflation and foregone returns don’t show up as a line item on your bank statement. You never see the $40,000 your retirement account didn’t grow to because you started five years late.

The mental model that fixes this is simple: always ask, what could this money earn today versus tomorrow? That one question reframes every financial choice. It shifts you from passive to active thinking about your money’s timeline.

The same logic that drives smart market timing decisions applies here. Long-term wealth building is impossible without making TVM instinctive, not just understood. Practice applying it even to small decisions and the habit compounds just like the money does.

Ready to master TVM and upgrade your finances?

Understanding the time value of money is only step one. Applying it consistently across your saving, investing, and borrowing decisions is where real wealth momentum builds. At Finblog, we publish practical guides, strategy breakdowns, and tool comparisons designed for people who want to make smarter money moves, not just understand the theory. If you want to put TVM to work right now, start by exploring our picks for top planning tools that help you model scenarios quickly and confidently. Bookmark the site and sign up for our newsletter to get new insights delivered straight to you.

Frequently asked questions

What formula is used to calculate the time value of money?

The most common formulas are present value (PV) and future value (FV), both of which use the interest rate and number of periods to move money forward or backward in time. TVM calculations rely on compound interest and PV/FV formulas to make those adjustments.

Why is the time value of money important?

It helps you make smarter financial choices by showing that money today can grow, lose value, or be invested compared to waiting for money in the future. The time value of money underpins smart investing and financial choices at every level.

How does compound interest relate to TVM?

Compound interest is the method that moves money forward through compounding or backward through discounting for TVM calculations. TVM calculations rely on compound interest for moving payments forward or back in time.

Can TVM be used for everyday decisions?

Yes, TVM helps you compare saving, investing, or loan options anytime you’re choosing between money now or later. TVM applies to common decisions like saving, investing, and choosing loans.

Recommended

- Personal Finance Myths Debunked for Smarter Money Decisions – Finblog

- Saving vs investing: key differences for smarter money – Finblog

- How to set financial priorities for smart wealth building – Finblog

- 7 Proven Time Management Hacks for Finance Professionals – Finblog

- When Is the Right Time to Withdraw Money from Your Business?