Choosing the right tax deduction could mean extra money stays in your pocket each year. For many American working professionals, understanding the difference between the standard deduction and itemizing can make a clear impact on their overall financial picture. By focusing on common tax deductions such as mortgage interest, state and local tax contributions, and retirement savings, you can take strategic steps to reduce your tax bill and strengthen your investment future.

Table of Contents

- What Are Common Tax Deductions?

- Standard Versus Itemized Deductions

- Popular Deduction Categories For 2026

- Eligibility Rules And Income Phaseouts

- Avoiding Costly Deduction Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Understanding Deductions | Tax deductions reduce taxable income, with common categories including mortgage interest and charitable donations. |

| Standard vs. Itemized Deductions | Choose between standard deductions for simplicity or itemizing for potentially greater savings, based on your expenses. |

| Above-the-Line Deductions | These deductions lower your adjusted gross income and include contributions like Health Savings Accounts and retirement accounts. |

| Avoiding Errors | Maintain meticulous records and seek professional assistance to avoid costly mistakes in claiming deductions. |

What Are Common Tax Deductions?

Tax deductions are strategic financial tools that help reduce your overall tax liability by lowering your taxable income. Tax deductions apply to specific expenses that the Internal Revenue Service (IRS) allows taxpayers to subtract from their gross income before calculating their final tax bill.

Understanding these deductions can potentially save you hundreds or even thousands of dollars annually. The two primary methods for claiming deductions are:

- Standard Deduction: A flat dollar amount that reduces taxable income

- Itemized Deductions: Specific expenses that can be individually claimed

Some of the most common tax deductions for working professionals include:

- Mortgage interest payments

- State and local tax contributions

- Charitable donations

- Student loan interest

- Retirement account contributions

- Healthcare expenses exceeding a certain percentage of income

- Business-related expenses for self-employed individuals

The value of these deductions directly depends on your personal financial situation and marginal tax rate. Understanding tax implications can help you make more informed financial decisions.

Pro tip: Keep meticulous records of potential deductible expenses throughout the year to maximize your tax savings during filing season.

Standard Versus Itemized Deductions

When filing taxes, taxpayers face a critical decision between claiming the standard deduction or itemizing their expenses. Tax deduction strategies vary depending on individual financial circumstances and total qualifying expenses.

The standard deduction is a predetermined, flat amount that reduces taxable income based on your filing status. For 2026, this amount differs depending on whether you’re single, married filing jointly, or head of household. Most taxpayers find the standard deduction simpler and more straightforward.

Itemized deductions, in contrast, require more detailed record-keeping but can potentially offer greater tax savings for some individuals. Common itemized deductions include:

- Mortgage interest payments

- State and local tax contributions

- Medical expenses exceeding 7.5% of adjusted gross income

- Charitable donations

- Unreimbursed job-related expenses

- Investment-related interest expenses

Key Comparison Points:

- Complexity: Standard deduction is simple; itemizing requires detailed documentation

- Potential Savings: Itemizing wins if total deductions exceed standard amount

- Eligibility: Some taxpayers are restricted from claiming standard deductions

Taxpayer statistics show only about 10% of individuals ultimately choose to itemize, typically those with significant deductible expenses.

Pro tip: Calculate both standard and itemized deductions to determine which method provides the maximum tax savings for your specific financial situation.

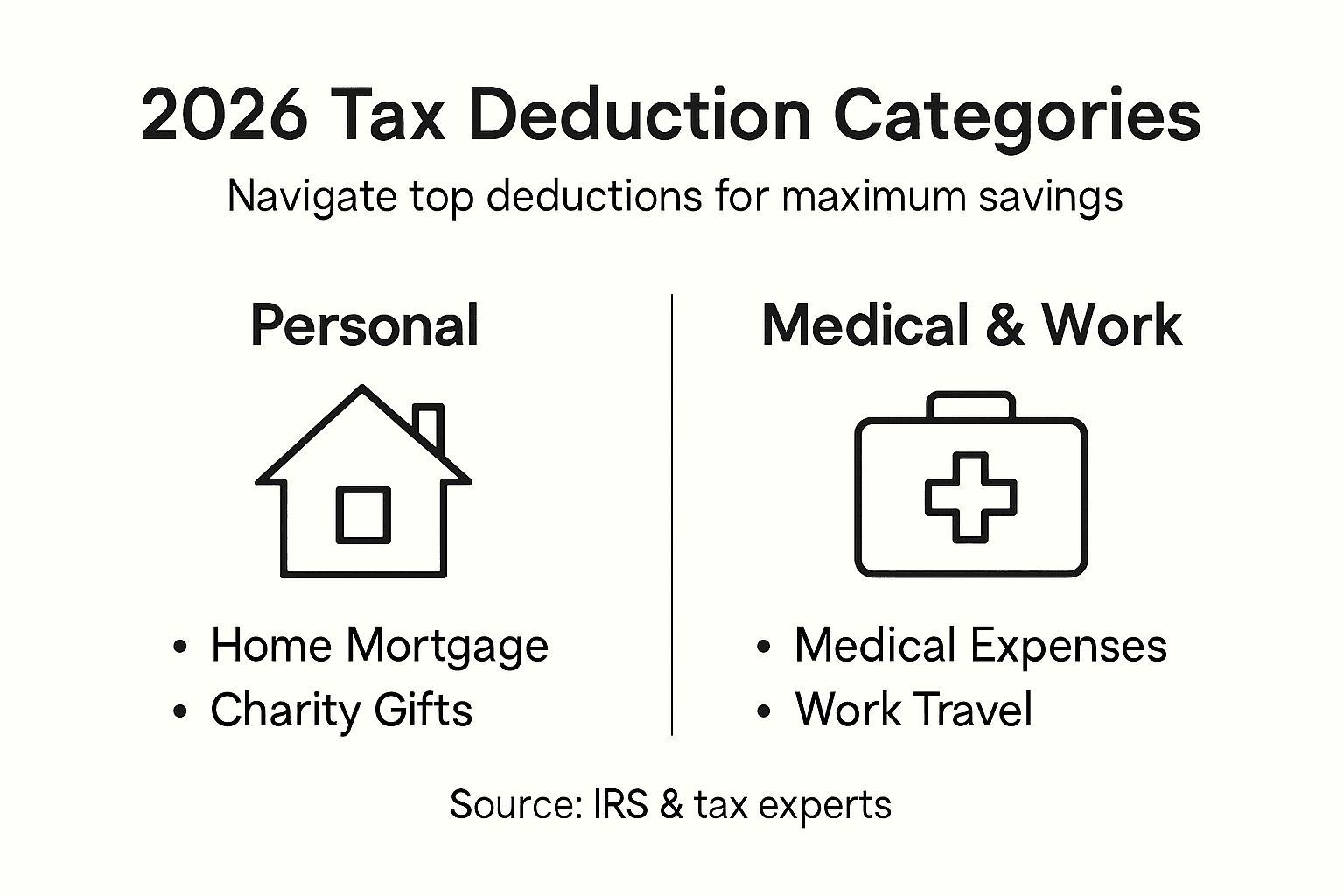

Popular Deduction Categories for 2026

Navigating tax deductions requires understanding the various categories available to reduce your taxable income. Tax deduction opportunities evolve each year, with 2026 offering several key strategies for financial optimization.

The most prominent deduction categories for 2026 fall into two primary classifications: above-the-line deductions and itemized deductions. Above-the-line deductions are particularly advantageous because they reduce your adjusted gross income before calculating other tax obligations.

Popular Above-the-Line Deduction Categories include:

- Health Savings Account (HSA) contributions

- Retirement account contributions (401k, IRA)

- Student loan interest payments

- Educator expense deductions

- Self-employment health insurance premiums

- Early withdrawal penalties from savings accounts

Itemized Deduction Categories for 2026 encompass:

- Mortgage interest payments

- State and local tax contributions

- Charitable donations

- Medical expenses exceeding 7.5% of adjusted gross income

- Investment-related interest expenses

- Certain gambling loss deductions

Deduction strategies for seniors have also expanded, with additional benefits like increased deductions for those 65 and older. These modifications can significantly impact overall tax liability for older taxpayers.

Here’s a concise comparison of above-the-line versus itemized deductions for 2026:

| Category Type | When Deducted | Typical Expenses Covered | Impact on Adjusted Gross Income |

|---|---|---|---|

| Above-the-Line | Before AGI calculation | HSA, student loan interest, IRA | Lowers AGI and tax liability |

| Itemized Deductions | After AGI, if chosen over standard amount | Mortgage interest, medical bills | Only benefits if total higher |

Pro tip: Consult a tax professional to ensure you’re maximizing all available deduction categories specific to your unique financial situation.

Eligibility Rules and Income Phaseouts

Tax deductions are not one-size-fits-all strategies. Deduction eligibility rules vary significantly based on income levels, filing status, and specific taxpayer circumstances.

Understanding income phaseouts is crucial for maximizing tax savings. These mechanisms gradually reduce or eliminate tax benefits as your annual income increases, creating a sliding scale of deduction availability that targets middle-income taxpayers.

Key Eligibility Factors for Deduction Phaseouts:

- Filing status (single, married, head of household)

- Adjusted gross income (AGI)

- Sources of income

- Participation in retirement plans

- Age and employment status

- Specific expense categories

Common Phaseout Scenarios:

-

Retirement Account Contributions

- Traditional IRA deductions phase out at higher income levels

- Roth IRA contribution limits decrease with increased income

-

Education-Related Deductions

- Student loan interest deductions reduce as income rises

- Education credits have strict income-based limitations

-

Charitable Contribution Limits

- Percentage-based deduction restrictions

- Income-related caps on total charitable donation claims

Tax benefit limitations are designed to ensure that higher-income taxpayers do not disproportionately benefit from tax reduction strategies. These rules create a more balanced approach to taxation.

Income phaseouts are not penalties, but strategic mechanisms to distribute tax benefits equitably across different income brackets.

Pro tip: Track your income throughout the year and consult a tax professional to understand how approaching specific income thresholds might impact your available deductions.

Avoiding Costly Deduction Mistakes

Tax deduction errors can be financially devastating, potentially triggering expensive audits or reducing your potential savings. Common deduction mistakes often stem from misunderstanding complex tax regulations and inadequate documentation.

The most prevalent tax deduction mistakes typically fall into several critical categories that can compromise your financial strategy. Recognizing these pitfalls is the first step toward protecting your hard-earned money and maintaining compliance with Internal Revenue Service guidelines.

Major Deduction Mistake Categories:

- Failing to keep comprehensive documentation

- Misunderstanding eligibility requirements

- Incorrectly calculating deduction amounts

- Overlooking potential deductions

- Mixing personal and business expenses

- Filing without professional guidance

Specific Error Scenarios to Avoid:

-

Documentation Disasters

- Discarding receipts before recommended retention period

- Incomplete record-keeping

- Not tracking mileage and business expenses systematically

-

Calculation Catastrophes

- Incorrectly computing deduction limits

- Misapplying phaseout rules

- Double-counting deductions

Tax compliance strategies require meticulous attention to detail and a thorough understanding of current tax regulations.

Small mistakes can lead to significant financial consequences, making precision crucial in tax preparation.

Pro tip: Invest in professional tax preparation software or consult a certified tax professional to minimize the risk of costly deduction errors.

Unlock Maximum Tax Savings for 2026 with Expert Guidance

Navigating common tax deductions can be overwhelming, especially when deciding between standard and itemized deductions or understanding income phaseouts. If you want to avoid costly deduction mistakes and fully leverage above-the-line and itemized deductions discussed in this article, you need tailored financial insight. Many taxpayers struggle keeping track of eligibility rules, documentation, and complex calculation methods that directly impact their tax savings.

Take control of your finances today by discovering strategies that fit your unique situation. Visit finblog.com to access expert advice and educational resources. Learn how to optimize your tax benefits and ensure you are not leaving money on the table by reviewing our comprehensive tax deduction insights. Don’t let confusing rules and phaseouts reduce what you can save. Act now and secure your financial future by getting personalized guidance at finblog.com.

Start maximizing your 2026 tax deductions before filing season hits. Your next step is one click away.

Frequently Asked Questions

What are the most common tax deductions for 2026?

Some common tax deductions for 2026 include mortgage interest payments, state and local tax contributions, charitable donations, student loan interest, retirement account contributions, and healthcare expenses exceeding a certain percentage of income.

How do I choose between standard and itemized deductions?

Choose the standard deduction for simplicity; however, if your total itemized deductions exceed the standard amount, itemizing could provide greater tax savings. Calculate both to determine your best option.

What are above-the-line deductions, and why are they beneficial?

Above-the-line deductions reduce your adjusted gross income (AGI) before calculating other tax obligations, offering a significant benefit. Examples include HSA contributions, retirement account contributions, and educator expense deductions.

How can I avoid common mistakes when claiming tax deductions?

To avoid mistakes, keep comprehensive documentation, understand eligibility requirements, carefully calculate deduction amounts, and consider consulting a certified tax professional for guidance.