Choosing the right vehicle for your investment portfolio can feel like a pivotal decision for seasoned investors and busy professionals alike. With both mutual funds and ETFs offering professionally managed, diversified pools of assets regulated by the SEC, understanding how these options differ becomes crucial for optimizing returns and managing risk. This article breaks down the core distinctions in trading flexibility, pricing, and transparency, giving you the clarity and confidence to align your strategy with your goals.

Table of Contents

- Core Concepts: ETFs And Mutual Funds Defined

- Types And Management Styles Compared

- Trading, Liquidity, And Transparency Features

- Cost Structures And Tax Implications

- Risks, Limitations, And Mistakes To Avoid

- Choosing The Right Option For Your Portfolio

Key Takeaways

| Point | Details |

|---|---|

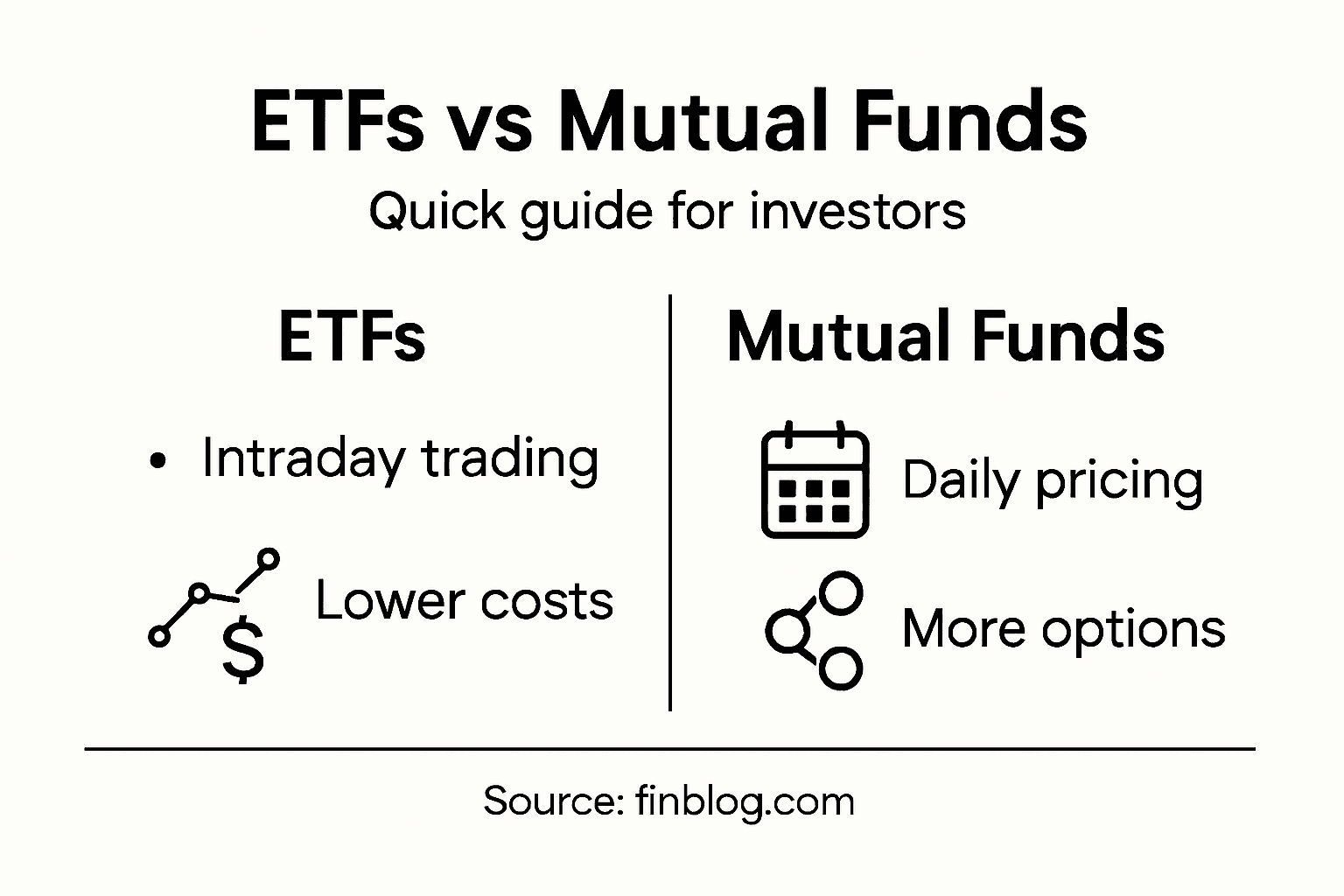

| ETFs provide intraday trading flexibility | Unlike mutual funds, ETFs can be bought and sold throughout the trading day, offering real-time price access. |

| Cost efficiency is crucial | Typically, ETFs have lower expense ratios than mutual funds, benefiting long-term investors by reducing costs over time. |

| Tax efficiency of ETFs is advantageous | ETFs use an in-kind redemption process that minimizes taxable gains, especially valuable for taxable investment accounts. |

| Choose based on your trading style | Determine if you need quick access to funds or if you’re comfortable with end-of-day pricing to decide between ETFs and mutual funds. |

Core concepts: ETFs and mutual funds defined

Both exchange-traded funds (ETFs) and mutual funds are investment companies registered with the SEC that allow you to pool money with other investors to purchase a diversified portfolio of stocks, bonds, or other assets. Think of them as professional investment vehicles that eliminate the need for you to personally research and buy hundreds of individual securities. The core appeal is straightforward: diversification and professional management without the headache of doing it yourself.

The practical differences lie in how these investments operate. Mutual funds are priced once daily after the market closes based on their net asset value calculation. You buy and redeem shares directly from the fund company at that day’s NAV price, similar to how you’d request a specific purchase amount. ETFs, by contrast, trade like individual stocks on exchanges throughout the day. Their prices fluctuate continuously based on supply and demand in real-time. This means you can buy or sell ETF shares at any point during market hours, not just at the closing bell. If you need to access your money quickly or want to catch a specific price point, this intraday trading capability matters significantly.

Both investments come with built-in professional management and the same regulatory oversight. A professional adviser manages holdings, and both require funds to disclose their holdings and fees through a prospectus. The key advantage over individual stock picking is obvious: you’re buying exposure to dozens or even hundreds of securities in a single purchase, dramatically reducing your exposure to any single company’s failure. For working professionals juggling multiple responsibilities, this hands-off approach provides meaningful peace of mind.

Here’s a quick comparison of core practical differences between ETFs and mutual funds:

| Factor | ETFs | Mutual Funds |

|---|---|---|

| Purchase Timing | Throughout market hours | After market close |

| Price Fluctuation | Real-time, changes all day | Fixed once daily at NAV |

| Access to Cash | Immediate during market hours | Delayed until NAV is calculated |

| Minimum Investment | Typically price of 1 share | Often set minimum, e.g., $1,000 |

| Order Placement | Broker/trading platform | Fund company or brokerage |

Pro tip: Before choosing between the two, check whether you’re an active trader who needs intraday pricing flexibility or a buy-and-hold investor comfortable with daily pricing, as this single factor often determines which vehicle works better for your actual investing style.

Types and management styles compared

When you choose an ETF or mutual fund, you’re actually making two separate decisions: what type of fund it is and how it’s managed. These decisions shape your returns, costs, and how much active oversight you need. Active management means a professional fund manager actively selects holdings trying to beat the market benchmark. Passive management means the fund simply replicates an index like the S&P 500, buying whatever securities are in that index. Most mutual funds have traditionally leaned toward active management, with managers constantly researching and adjusting positions. ETFs emerged primarily as passive, index-tracking vehicles but the landscape has shifted significantly.

Today’s reality is more nuanced than the old stereotype suggests. Mutual funds still offer both active and passive options, though active remains dominant in the mutual fund space. ETFs, however, have expanded dramatically beyond their passive roots. You can now find actively managed ETFs competing directly with active mutual funds, plus passive ETFs tracking virtually every index imaginable. The practical difference comes down to fees and transparency. Active management typically costs more because you’re paying for research, analysis, and frequent trading. Passive funds charge lower fees since they simply mirror an index. ETFs generally offer better intraday transparency, showing you exactly what holdings are in the fund throughout the trading day, whereas mutual fund holdings are typically disclosed less frequently.

Your management style choice directly affects your investment strategy and risk exposure. An active mutual fund manager might take concentrated bets on specific sectors or companies, potentially delivering outsized returns or losses. A passive ETF tracking the total market will move in lockstep with that market, without surprise underperformance from poor stock picking but also without the chance of outperformance. For working professionals making periodic contributions and holding long-term, passive index-tracking ETFs often deliver better risk-adjusted returns when you factor in fees. The math is compelling: after fees, most active fund managers fail to consistently beat their benchmarks over extended periods.

Pro tip: Compare the fee structure first, then assess whether you believe the fund manager’s track record justifies paying extra for active management; if returns don’t clearly exceed the fee difference over the past five years, passive options are likely the smarter choice.

Trading, liquidity, and transparency features

This is where ETFs and mutual funds diverge most noticeably in practical, day-to-day investing. The differences affect when you can buy or sell, what prices you pay, and how much you actually know about what you own. ETFs trade like stocks on public exchanges throughout the day. You can buy or sell shares during market hours at real-time prices determined by supply and demand. If the market drops sharply mid-morning and you want out immediately, you can execute that trade within seconds. Mutual funds work completely differently. When you place a buy or sell order, it gets processed at the next calculated net asset value after the market closes. You submit your request at 2 p.m., but you won’t know your execution price until 4 p.m., after the market has closed. This creates a significant lag if market conditions shift suddenly between your order and the closing bell.

Liquidity tells you how easily you can convert your investment into cash without losing value. ETFs have a structural advantage here because they combine features of both mutual funds and stocks. ETF shares trade intraday on exchanges with continuous pricing and high liquidity, whereas mutual funds only transact at end-of-day NAV. Behind the scenes, authorized participants create and redeem ETF shares in large blocks, which keeps prices efficient and spreads tight. For most investors, ETF trading spreads are remarkably small, often just a few cents per share. Mutual fund trading is essentially free since there’s no spread, but that only matters if you’re comfortable waiting until market close. If you need rapid access to your money during market hours, ETFs provide measurable advantages.

Transparency means visibility into what the fund actually holds. ETFs typically disclose their complete holdings daily, sometimes even in real-time. You can check exactly what stocks or bonds are in your fund at any moment during the trading day. Mutual funds typically disclose holdings quarterly, sometimes with a lag. This matters more if you’re concerned about portfolio liquidity and tracking performance, or if you want to avoid overlap with other investments you own. For active traders managing complex portfolios, this daily transparency prevents surprises. For buy-and-hold investors with simple portfolios, quarterly disclosures are often sufficient.

Pro tip: If you trade frequently or need to access funds quickly, prioritize ETFs for their intraday trading and real-time transparency; if you make occasional contributions and hold long-term, mutual fund timing lags matter less.

Cost structures and tax implications

Costs matter because they directly reduce your returns year after year. Both ETFs and mutual funds charge annual expense ratios, which are management and operational fees expressed as a percentage of your investment. A 0.5% expense ratio on a $100,000 portfolio costs you $500 annually. Over 30 years, that seemingly small difference compounds dramatically. But ETFs and mutual funds add costs in different ways beyond the base expense ratio. Mutual funds often charge sales loads, which are commissions paid when you buy or sell shares, ranging from 1% to 6% of your investment. Some mutual funds also impose redemption fees or account minimums. ETFs generally avoid these load charges entirely. Instead, you pay brokerage commissions when trading ETF shares, similar to buying individual stocks. Most brokers now offer commission-free ETF trading, effectively eliminating this cost for small trades.

Tax efficiency creates an even larger gap for long-term investors. This is where ETF structure becomes genuinely clever. When investors redeem ETF shares, the fund manager can exchange securities directly without triggering capital gains. This in-kind redemption mechanism keeps capital gains inside the fund rather than distributing them to remaining shareholders. Mutual funds work differently. When a manager sells securities to raise cash for redemptions, that sale often realizes capital gains that must be distributed to all shareholders, even those who didn’t sell. You end up paying taxes on gains you didn’t realize. Across bull markets, this compounds into meaningful differences. A study comparing identical mutual fund and ETF portfolios over extended periods typically showed ETFs distributed 20-30% less in taxable gains annually.

Understanding tax implications of your investment choices helps you plan strategically. Active mutual fund managers also tend to generate more capital gains through frequent trading, creating additional tax drag. Passive ETFs, by their nature, trade infrequently, minimizing these distributions. For taxable investment accounts (not retirement accounts), this difference can be substantial over decades. A $500,000 investment growing at 8% annually will generate significant taxable distributions, and a 30% reduction in that tax burden is real money staying in your pocket.

Pro tip: In taxable accounts, prioritize ETFs for their tax efficiency, especially if you hold positions for multiple years; in retirement accounts where taxes don’t apply, both vehicles work equally well, so focus on expense ratios and investment quality instead.

This table summarizes how costs and taxes differ between ETFs and mutual funds:

| Aspect | ETFs | Mutual Funds |

|---|---|---|

| Expense Ratios | Typically lower | Can be higher, especially active |

| Sales Loads | Usually none | Frequently 1-6% |

| Brokerage Fees | Often commission-free now | Rarely applies |

| Tax Efficiency | High, due to in-kind process | Lower, gains often distributed |

| Capital Gains Drag | Minimized | Common, especially with turnover |

Risks, limitations, and mistakes to avoid

Both ETFs and mutual funds carry market risk, the fundamental reality that your investment value can decline and you can lose money. Market downturns affect both vehicles equally. A stock market correction hits your ETF and mutual fund holdings the same way. The differences emerge in how risks are distributed and what additional risks specific structures create. ETFs introduce liquidity risk in certain situations. While most broad ETFs trade with tight spreads, specialty ETFs focused on niche sectors, emerging markets, or bonds can have wider spreads and lower trading volume. If you own 10,000 shares of an obscure commodity ETF and need to exit quickly, you might face slippage, meaning your actual execution price is worse than the quoted price. Mutual funds avoid this problem entirely since you redeem directly from the fund at NAV. But mutual funds carry timing risk. If you submit a sell order at 3 p.m. and markets drop 5% overnight, you’re stuck with whatever NAV calculates at the next close.

Leveraged and inverse ETFs represent a common mistake that deserves special attention. These funds use borrowed money or derivatives to amplify returns or bet against market declines. They’re marketed as tactical trading tools, but they’re genuinely dangerous for regular investors. Leveraged ETFs compound returns daily, which means they drift from their intended target over time. A 3x leveraged tech ETF isn’t simply triple tech exposure over years. Compounding effects distort returns dramatically, especially during volatile periods. Inverse ETFs that profit when markets fall sound attractive during bear markets, but holding them during recovery phases creates severe losses. These products belong in short-term tactical trading portfolios, not long-term retirement accounts.

The biggest mistake is treating all ETFs and mutual funds as identical vehicles. Investors often assume all investment products carry similar risk profiles, but a leveraged ETF and a conservative bond index fund exist in completely different risk universes. Many investors also misunderstand tracking error, which measures how closely an ETF follows its target index. A fund tracking the S&P 500 might deviate by 0.15% annually due to fees and operational costs. This seems trivial until you realize it compounds to thousands of dollars over decades. Before investing, read the prospectus, understand the fund’s objective, check the expense ratio, and honestly assess whether the fund’s strategy aligns with your goals and risk tolerance. Don’t buy something because it’s trendy or because a coworker mentioned it.

Pro tip: Avoid leveraged and inverse ETFs entirely unless you’re actively managing trades daily; instead, focus on broad, low-cost index funds or ETFs that match your time horizon, and rebalance your overall portfolio annually rather than trying to time short-term price movements.

Choosing the right option for your portfolio

The choice between ETFs and mutual funds isn’t about finding a universally superior option. It’s about matching the vehicle to your specific situation, goals, and investing style. Start by asking yourself three fundamental questions: How often do you plan to trade? Do you need access to your money quickly? Are you investing in a taxable account or a retirement account? Your answers reshape the calculus entirely. If you’re a working professional making monthly contributions to a long-term retirement portfolio and rarely touching the money, the differences between ETFs and mutual funds matter less. You’ll benefit from either option if you choose low-cost, diversified funds. If you’re actively rebalancing quarterly, trading based on market conditions, or managing a complex taxable portfolio with multiple positions, ETFs become more attractive. Their intraday trading flexibility and tax efficiency provide measurable advantages.

Consider your account structure carefully. In a 401k or traditional IRA, both ETFs and mutual funds work identically because taxes don’t apply inside these accounts. Your only decision becomes expense ratios and investment quality. A 0.03% expense ratio ETF and a 0.04% mutual fund are virtually interchangeable in retirement accounts. In taxable brokerage accounts, the calculus shifts. ETFs’ tax efficiency becomes genuinely valuable. Over 30 years, avoiding unnecessary capital gains distributions can preserve tens of thousands of dollars. Your ability to implement effective portfolio diversification strategies depends partly on having the right tools. ETFs’ granular transparency and low costs make it easier to build precisely targeted allocations without overlap or excessive fees dragging on returns.

Time horizon matters significantly. If you’re investing for retirement 20 or 30 years away, choose low-cost index funds or ETFs and ignore short-term volatility. Active management rarely justifies its costs over extended periods. If you’re saving for a home purchase in 3 years, prioritize stability over growth and avoid both complex specialty funds and leveraged products. Your risk tolerance determines fund selection more than the ETF versus mutual fund decision. A conservative investor should choose bond-heavy or balanced funds regardless of vehicle type. An aggressive investor can hold 90% equities through either ETFs or mutual funds. The vehicle is secondary to the asset allocation strategy.

One practical advantage of ETFs deserves emphasis for busy professionals: simplicity. You can build a complete portfolio with just three or four ETFs covering U.S. stocks, international stocks, bonds, and real estate. Add one commission-free trading broker, set up automatic monthly investments, and you’ve solved your portfolio construction problem for decades. Mutual funds require more research to find low-cost options without sales loads. You’ll find excellent mutual fund options, but you’ll work harder to identify them. Conversely, if you love the structure of a particular mutual fund family or if your employer’s 401k limits you to specific mutual fund options, that constraint simplifies your decision entirely.

Pro tip: Start with a simple three-fund or four-fund portfolio using low-cost index vehicles, whether ETFs or mutual funds, and focus 80% of your mental energy on consistent contributions and staying invested through market downturns; the 20% difference in fees and tax efficiency matters far less than discipline and time in the market.

Make Smarter Investment Choices With Expert Guidance

Understanding the difference between ETFs and mutual funds involves more than just picking one over the other. The challenge many investors face is navigating complex concepts like active versus passive management, tax efficiency, trading liquidity, and cost structures. If you are a working professional seeking to build a diversified portfolio while minimizing risks such as tax drag or timing issues, you need clear answers tailored to your goals and investing style.

At finblog.com, we specialize in helping investors like you cut through the noise. Whether you want to explore the benefits of intraday ETF trading or the simplicity of mutual funds for long-term wealth building, our expert resources and personalized consultations empower you to make confident decisions. Start now to align your portfolio strategy with your financial future by visiting finblog.com and discover actionable insights designed for serious investors who want to avoid common pitfalls. Take the step toward smarter investing today.

Frequently Asked Questions

What are the main differences between ETFs and mutual funds?

ETFs trade throughout the day like individual stocks and offer real-time pricing, while mutual funds are priced once daily after the market closes based on their net asset value (NAV).

How do the costs of ETFs compare to mutual funds?

ETFs generally have lower expense ratios and no sales loads, while mutual funds may come with higher fees, including sales loads and higher expense ratios, especially for actively managed funds.

What is the tax efficiency of ETFs compared to mutual funds?

ETFs tend to be more tax-efficient due to their in-kind redemption mechanism, which minimizes capital gains distributions. In contrast, mutual funds often distribute capital gains, which can result in tax liabilities for investors.

Which investment vehicle is better for long-term investors, ETFs or mutual funds?

For long-term investors, passive index-tracking ETFs often deliver better risk-adjusted returns due to lower fees and tax efficiency. However, individual circumstances and investment goals should guide the final decision.