Nvidia posted huge Q2 numbers, guided Q3 to $54B ±2%, and said the AI build-out is still just starting. China/H20 revenue was zero in Q2 and not in Q3 guidance. The company is licensed to ship to China, but policy remains the swing factor. Below is a clean, well-structured article with paragraphs first and lists after each headline, plus direct quotes.

Results snapshot (so the quotes have context)

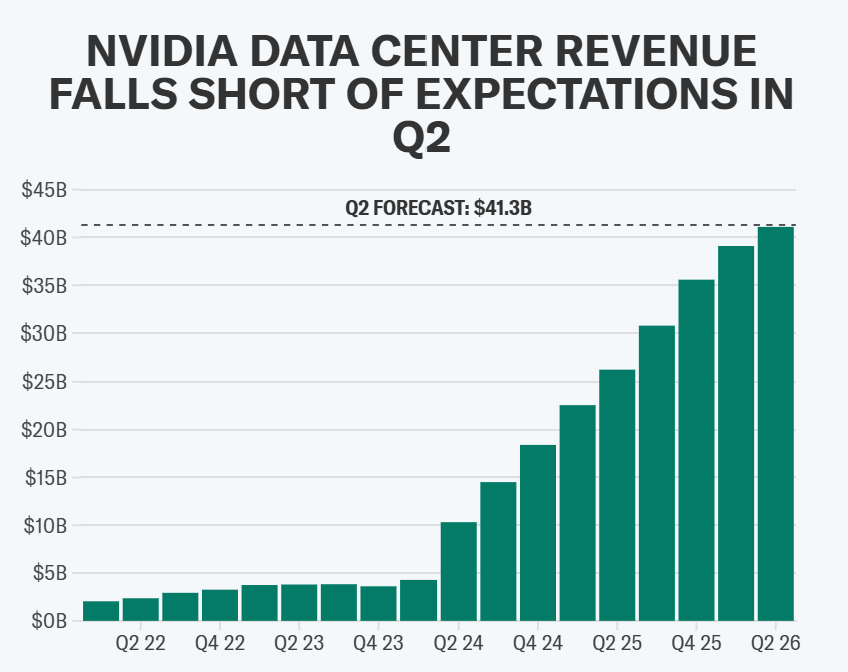

The quarter was dominated by Data Center strength and a networking surge. Management also called out mix details (cloud ≈ half of DC), customer concentration, and geography billing optics (Singapore billing for U.S. customers). China/H20 stayed at zero in Q2 and is excluded from Q3. (More about: Nvidia Beats, But Here is Why Shares Slip)

Jensen Huang : Vision, demand, China — in his own words

After earnings, Nvidia CEO Jensen Huang spoke, and Jensen’s core message was that the AI cycle is in its early stages, compute needs are surging (especially for reasoning/agentic AI), and Nvidia wants the American tech stack to be the global standard, including China, if approvals allow. He also emphasised that supply remains tight and system scale is crucial.

- “A new industrial revolution has started. The AI race is on.”

- “We see $3–$4 trillion in AI infrastructure spend by the end of the decade.”

- “There’s about $600 billion in data-center capex… we’re at the beginning of this build-out.”

- “Because of agentic AI, the amount of hallucination has dropped… you can now use tools and perform tasks. Enterprises have been opened up.”

- “The compute necessary for one-shot vs. reasoning/agentic AI could be 100×, 1000×, potentially more.”

- “We’ve been approved and licensed to ship to China, and now we’re looking for orders.”

- “Bringing Blackwell to the China market is a real possibility… we’ll keep advocating that the American tech stack becomes the global standard.”

Why it matters:

- Multi-year runway: bigger models + tools/agents = more compute, bigger clusters, faster refresh.

- Policy is gating China: licenses in hand; orders depend on formal approvals.

- Platform, not just chips: Nvidia pushes a full rack-scale system (GPU + CPU + NVLink + SuperNIC + software).

Colette Kress (CFO): What’s actually in the numbers and the guide

Colette set clear guardrails: Q3 guidance excludes China/H20; $2–$5B of H20 could ship in Q3 if geopolitics ease. She highlighted networking’s boom, sovereign AI momentum, the 15% discussion (not codified), and transparency around billing geography.

- “We have not included H20 in our Q3 outlook as we continue to work through geopolitical issues.”

- “If geopolitical issues subside, we should ship $2–$5B in H20 revenue in Q3; and if we had more orders, we can bill more.”

- “U.S. officials have expressed an expectation that the U.S. will receive 15% of revenue from licensed H20 sales, but no regulation codifies this.”

- “Over 99% of Data Center compute revenue billed to Singapore was for U.S.-based customers.”

- Networking momentum: roughly $7.2B, ~+98% YoY (reflects larger fabrics: NVLink/InfiniBand/Ethernet for AI)

- Sovereign AI: “on track to > $20B this year” as governments fund national AI factories

- Compute mix: H20 decline (~$4B) explains the QoQ dip in compute despite overall DC strength

China & policy: What changed, what didn’t

Nvidia sold no H20 to China in Q2, released $180M of reserved H20 inventory, and moved ~$650M of H20 to a non-China customer. Management excluded China H20 from Q3. U.S. officials have talked about a 15% revenue share on licensed China sales, but there is no published regulation. The company’s filing warns that any request for a percentage of revenue may subject Nvidia to litigation.

Q2 China H20: $0

Inventory release: $180M (linked to ~$650M H20 outside China)

Q3 guide: excludes China H20; $2–$5B potential only if approvals/conditions improve

15% discussion: not codified; flagged as potential litigation risk in the 10-Q

Management stance: actively advocating for approvals to sell Blackwell in China

Where Nvidia stands now

Nvidia looks less like a chip vendor and more like an AI-factory supplier: GPUs, NVLink fabrics, Ethernet/InfiniBand, software, and full rack-scale systems. Demand remains broader than one buyer group: CSPs ≈ 50% of DC, but sovereign/enterprise channels are now meaningful. Two mega-customers are a big piece of quarterly revenue — a strength and a risk.

Platform moat: chips + networking + systems + software (one programming model from cloud to edge)

Networking boom: ~$7.2B, ~+98% YoY — evidence of larger clusters (not just more GPUs)

Buyer mix: CSPs ≈ 50% of DC; sovereign AI now a $20B+ 2025 revenue engine

Concentration: two customers = ~39% of Q2 revenue (23% & 16%)

Geography optics: Singapore billing mostly reflects invoicing hubs, not end demand

Key takeaways from earnings

The engine is strong without China; China is upside, not base case. Policy, not demand, is the near-term swing factor. Nvidia’s edge is the full stack and an annual product cadence (Blackwell now, Rubin queued).

- Beat + raise with conservatism: Q3 $54B ±2% excludes China H20; upside exists but isn’t assumed.

- Demand ≠ peaked: Agentic/reasoning AI drives orders-of-magnitude more compute; hence bigger clusters, faster refresh.

- Networking matters: ~+98% YoY shows the fabric is now a revenue pillar, not a sidecar.

- Policy watch: 15% concept is not law; company flags litigation risk if enforced by request.

- China is a call option: $2–$5B H20 could drop into Q3 if conditions ease; Blackwell for China is “a real possibility.”

- Platform vs. ASICs: System complexity + unified programming model raises the bar for custom chips.

- Concentration cuts both ways: A few mega-buyers amplify both upside and risk.

What to watch next

The next catalysts are policy headlines, confirmed purchase orders, and execution on the product roadmap and fabrics. These decide whether upside shows up now or later.

- Formal US guidance on licensed China sales (any rule on 15%)

- Actual POs for H20 (and Blackwell) into China

- Blackwell ramp vs. Hopper run-rate (lead times, mix, margins)

- Networking run-rate (NVLink/Ethernet/InfiniBand scale-out)

- Sovereign AI wins (Europe’s AI factory plans; other national builds)

- Rubin milestones (annual cadence, taped-out parts at TSMC)

Nvidia’s Q2 shows a company selling AI factories, not just chips: Data Centre at $41.1B, networking up ~98% YoY, and Q3 guided to $54B ±2% without counting China. Jensen calls this a “new industrial revolution” with $3–$4T of AI infrastructure ahead and says Nvidia is licensed and “looking for orders” in China, while Colette keeps the outlook clean — no China H20 assumed, but $2–$5B could drop in if geopolitics allow. The much-discussed 15% U.S. take is not codified, and the 10-Q warns that any such request could lead to litigation.

Nvidia delivered another monster quarter, guided above Street, and kept the long-term story intact: more compute per model, bigger clusters, and a full-stack platform that’s spreading beyond hyperscalers to sovereigns and enterprises. The only real near-term swing factor is policy—how the U.S.–China rules land. If the door cracks open, China becomes upside; if not, the rest of the market (plus Rubin in 2026) is clearly big enough to keep the flywheel spinning.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related: Nvidia Q2 2026 Earnings Preview and Prediction: What to expect

Why Warren Buffett and Hedge Funds Are Betting on UnitedHealth Stock (UNH)