Financial coaching isn’t just for the wealthy. That’s a myth worth dismantling right now. Most people assume they need a six-figure portfolio before a coach becomes useful, but research shows coaching measurably increases savings, improves credit scores, and reduces debt for everyday individuals. Whether you’re living paycheck to paycheck or just starting to invest, the principles behind coaching can reshape how you relate to money. In this article, you’ll discover what financial coaching actually is, how it differs from education and advising, and how to apply its core methods to your own financial life starting today.

Table of Contents

- The basics: What is financial coaching?

- How financial coaching drives real change

- Coaching versus education: What’s the difference?

- Applying coaching principles to your financial life

- Why most people underestimate coaching’s impact

- Connect with expert guidance for lasting change

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Coaching drives real change | Financial coaching has proven effects on increasing savings, credit scores, and lowering debt for everyday people. |

| Coaching and education differ | Coaching offers personalized, action-oriented support while financial education provides foundational knowledge. |

| Principles are actionable | You can apply core coaching strategies to your own finances to improve habits and results. |

| Progress is measurable | Research shows quantifiable benefits, such as up to a 26-point credit score improvement with coaching. |

The basics: What is financial coaching?

A financial coach is a trained professional who works with you one-on-one to identify your money habits, set clear goals, and build a realistic plan to reach them. Think of it less like a classroom and more like a personal trainer for your finances. The coach doesn’t manage your money or sell you products. Instead, they help you understand your own behavior and make better decisions over time.

Coaches typically focus on several core areas:

- Budgeting: Building a spending plan that actually fits your life

- Debt management: Creating a strategy to pay down what you owe

- Saving habits: Developing consistent routines around setting money aside

- Basic investing: Understanding how to start growing wealth

- Financial mindset: Addressing the emotional and psychological side of money

So how does this differ from other types of financial help? The distinction matters. A financial advisor, for example, is licensed to manage investments and recommend specific products. You can read more about the benefits of financial advisors to understand where their role begins. A financial coach, by contrast, focuses on behavior and habit change rather than portfolio management.

Financial education, meanwhile, typically involves workshops, online courses, or reading materials. It’s valuable, but it’s usually one-size-fits-all. Coaching is personalized and ongoing. That distinction is exactly why coaching improves financial behaviors beyond what traditional education alone can achieve.

| Feature | Financial coaching | Financial advising | Financial education |

|---|---|---|---|

| Personalized | Yes | Yes | Rarely |

| Ongoing support | Yes | Sometimes | No |

| Product recommendations | No | Yes | No |

| Behavior-focused | Yes | Partially | Partially |

| Cost | Moderate | Higher | Low to free |

If you’re just starting out, exploring financial planning for beginners can help you figure out which type of support fits your current situation best. The short answer: almost anyone who wants to improve their money habits can benefit from coaching, regardless of income level.

How financial coaching drives real change

With a clearer understanding of what financial coaching is, we can dig into how it makes a quantifiable impact in people’s lives.

The connection between coaching and real financial improvement isn’t just anecdotal. Randomized controlled trials, which are studies that randomly assign participants to groups to test cause and effect, consistently show that coaching increases savings rates, improves credit scores, and leads to lower debt utilization compared to control groups.

Here’s a snapshot of what the research shows:

| Outcome | Coaching group result | Control group result |

|---|---|---|

| Credit score change | +26 points average | Minimal change |

| Savings rate | Significantly higher | Baseline |

| Debt utilization | Lower | Unchanged |

| Financial confidence | Increased | Marginal change |

“Participants who received financial coaching showed statistically significant improvements in savings behavior and credit outcomes compared to those who received no coaching.”

Let’s make this concrete. Imagine a 34-year-old with $8,000 in credit card debt and a credit score of 610. After six months of working with a coach, she has a structured repayment plan, has reduced her utilization ratio, and her score climbs to 636. That’s not magic. That’s accountability, goal-setting, and consistent action.

For anyone looking to build on that momentum, reviewing credit score improvement tips gives you a practical framework alongside coaching. And if debt is your primary concern, learning about mastering credit card debt can complement what a coach helps you build.

The improvements coaching drives come from a few key mechanisms:

- Accountability: Regular check-ins create pressure to follow through

- Personalization: Advice fits your actual income, goals, and habits

- Behavioral focus: Coaches target the root causes of financial struggles, not just the symptoms

- Momentum: Small wins build confidence that compounds over time

This is why coaching works where a single workshop or article often doesn’t. It stays with you.

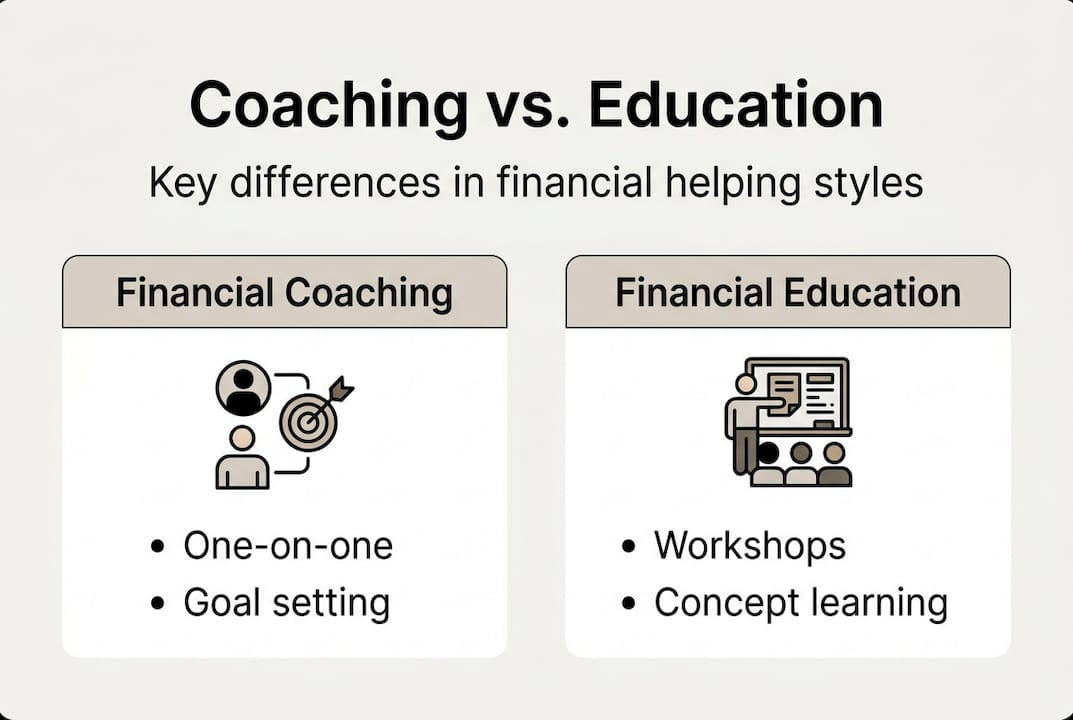

Coaching versus education: What’s the difference?

While research supports that coaching can shift financial behaviors, it’s important to also understand how it compares with traditional education.

Both coaching and education improve financial outcomes, but they get there through very different paths. Coaching and education differ in delivery, pacing, and the type of change they produce. Understanding those differences helps you choose the right tool for where you are right now.

| Factor | Financial coaching | Financial education |

|---|---|---|

| Format | One-on-one sessions | Courses, workshops, articles |

| Duration | Ongoing over weeks or months | Often a single event or course |

| Customization | Tailored to your situation | General audience |

| Primary goal | Behavior change | Knowledge transfer |

| Accountability | Built in | Self-directed |

Financial education is a great starting point. It builds the vocabulary and conceptual foundation you need to make sense of your options. You can explore the importance of financial education to understand how foundational knowledge sets the stage for smarter decisions.

But knowledge alone rarely changes behavior. You might finish a budgeting course and still overspend the following month. That’s not a failure of intelligence. It’s a failure of application, and that’s exactly the gap coaching fills.

Here’s a simple way to decide which you need right now:

- If you feel lost about basic concepts: Start with financial education to build your foundation.

- If you understand the concepts but can’t stick to a plan: Coaching is likely your missing piece.

- If you’re dealing with a specific crisis (debt, job loss): Coaching provides the personalized, urgent support education can’t.

- If you want to level up your investing knowledge: Education plus a coach who specializes in investing is a powerful combination.

- If you’ve tried budgeting apps without success: A coach can identify why the tools aren’t working for your specific habits.

The smartest approach often combines both. Learn the concepts, then work with a coach to apply them in your real life.

Applying coaching principles to your financial life

Understanding where coaching and education fit is useful, but you might be wondering how you can benefit directly. Here’s how to apply coaching methods to your own finances, even before you hire anyone.

The core of coaching is structured action. It’s not about knowing more. It’s about doing differently, consistently. Goal-setting and accountability directly improve saving and debt reduction success rates, which means you can borrow these tools right now.

Here’s a four-step framework to start self-coaching your finances:

- Set one clear, specific goal. Not “save more money” but “save $200 per month by cutting dining out to twice a week.” Specificity is what makes goals actionable.

- Track your progress weekly. Use a simple spreadsheet, a notebook, or a budgeting app. The act of tracking makes invisible habits visible. You can’t fix what you can’t see.

- Review and adjust monthly. At the end of each month, ask: What worked? What didn’t? What needs to change? This is where real learning happens.

- Build in support. This could be a professional coach, a trusted friend, or an online community. Accountability dramatically increases follow-through.

If debt is your biggest challenge, pairing this framework with proven debt repayment strategies gives you both the mindset and the mechanics to move forward.

Pro Tip: Find an accountability buddy, someone with similar financial goals, and check in with each other weekly. Research consistently shows that social accountability is one of the strongest predictors of follow-through on financial commitments. You don’t need a paid coach to benefit from this principle.

Start small. Pick one habit to change this week, not five. Coaching works because it’s focused and sustainable, not because it’s overwhelming.

Why most people underestimate coaching’s impact

Seeing how coaching can be applied firsthand, it’s worth considering why so many still overlook or underestimate its power.

Conventional wisdom says that reading a few good books or taking a free online course is enough to fix your finances. The evidence says otherwise. The problem isn’t access to information. In 2026, financial content is everywhere. The real barrier is behavior, and behavior doesn’t change through information alone.

Coaching’s impact is also easy to dismiss because progress feels slow at first. A 26-point credit score increase over six months doesn’t feel dramatic in the moment. But compounded over years, that shift changes what loans you qualify for, what interest rates you pay, and ultimately how much wealth you build.

There’s also a cultural hesitation around asking for help with money. Many people feel shame about their financial situation, which keeps them from seeking support. But a good coach creates a judgment-free space where you can be honest about where you actually are. That honesty is the starting point for real change.

Understanding the financial advisor roles that exist in the market helps clarify that coaching isn’t a luxury. It’s a practical tool, and its behavioral focus is precisely what makes it so effective compared to generic advice.

Connect with expert guidance for lasting change

If you’re ready to turn knowledge into action, partnering with expert coaches might be your next step. The principles covered here, goal-setting, accountability, behavior change, are far more powerful when guided by someone who can tailor them to your specific situation. At finblog.com, you’ll find resources designed to help you move from financial confusion to confident decision-making. Whether you’re just starting out or looking to accelerate progress you’ve already made, exploring financial coaching resources connects you with the kind of personalized guidance that generic content simply can’t provide. Your financial future is worth investing in.

Frequently asked questions

What does a financial coach do for me?

A financial coach helps you set realistic goals, build action plans, and supports you in making lasting changes to reach your money objectives. Research confirms that coaching increases savings and reduces debt over time.

How is financial coaching different from hiring a financial advisor?

Coaching focuses on building behaviors and everyday financial habits, while advisors manage investments and offer specific product recommendations. The two roles complement each other but serve different needs.

Can coaching really improve my credit score?

Coaching clients in studies increased their credit scores by an average of 26 points, alongside reduced debt utilization. Consistent accountability and targeted action plans drive those results.

What should I look for in a financial coach?

Look for certified professionals with strong communication skills and experience helping clients like you achieve specific financial goals. A good coach listens first and customizes their approach to your actual situation.