TL;DR:

- Behavioral economics studies how psychological and emotional factors influence economic decisions, deviating from rational behavior.

- Its core principles include loss aversion, framing effects, present bias, and overconfidence, which explain predictable decision-making patterns.

Behavioral economics is defined as the study of how psychological, cognitive, and emotional factors systematically influence economic decisions. Unlike classical economics, which assumes people act as perfectly rational agents, behavioral economics draws on psychology, neuroscience, and sociology to explain why real decisions often deviate from what theory predicts. Pioneers like Daniel Kahneman and Amos Tversky demonstrated through Prospect Theory that people do not weigh gains and losses symmetrically. Kahneman’s book Thinking, Fast and Slow brought these ideas to a mainstream audience. The field now shapes public policy, financial product design, and personal finance strategy in measurable ways.

What is behavioral economics and why does it matter?

Behavioral economics is the interdisciplinary science that integrates psychology, neuroscience, and sociology into economic models to explain deviations from rational actor assumptions. Classical economics assumes people have perfect information, stable preferences, and always maximize utility. Behavioral economics replaces those assumptions with evidence from real human behavior. The result is a more accurate picture of how decisions actually get made.

The importance of behavioral economics goes beyond academic theory. It improves traditional economic models by offering realistic frameworks for decision-making and aids policy and corporate design. Governments use it to design better retirement systems. Businesses use it to build products people actually choose. Investors use it to understand why markets behave irrationally during crises.

The field also reframes what “irrational” means. Human errors in judgment are not random noise. They are predictable and measurable, which means they can be modeled, anticipated, and addressed through smart design. That predictability is what makes behavioral economics so powerful.

What are the fundamental principles of behavioral economics?

Six core principles explain most of what behavioral economics covers. Each one describes a specific, repeatable pattern in how people make choices.

-

Bounded Rationality. People do not process all available information before deciding. They use mental shortcuts, called heuristics, to reach “good enough” conclusions quickly. This explains why complex financial decisions often get simplified into gut feelings. Bounded rationality implies predictable rather than random irrationality, which shifts how economists model behavior.

-

Loss Aversion. Losses feel roughly twice as painful as equivalent gains feel good. A $500 loss hurts more than a $500 gain pleases. This asymmetry, central to Prospect Theory, explains why investors hold losing stocks too long and sell winning ones too early.

-

Framing Effect. The way information is presented changes the choice people make, even when the underlying facts are identical. A medical treatment described as having a “90% survival rate” gets chosen more often than one described as having a “10% mortality rate.” Same data, different decision.

-

Present Bias. People consistently overvalue immediate rewards relative to future ones. This explains why saving for retirement feels abstract and spending today feels concrete. Present bias is a primary driver of undersaving across income levels.

-

Anchoring. The first number a person sees in a negotiation or purchase decision acts as a reference point that distorts all subsequent judgments. A $1,000 price tag makes a $700 alternative feel like a bargain, even if $700 is still overpriced.

-

Overconfidence Effect. People systematically overestimate the accuracy of their own predictions and abilities. In investing, overconfidence leads to excessive trading, concentrated portfolios, and underestimation of risk.

Pro Tip: When you notice yourself reacting strongly to a financial loss, pause before acting. Loss aversion is likely amplifying the emotional signal beyond what the facts warrant.

These core principles explain recurring decision patterns that standard economics consistently missed. They are not edge cases. They are the norm.

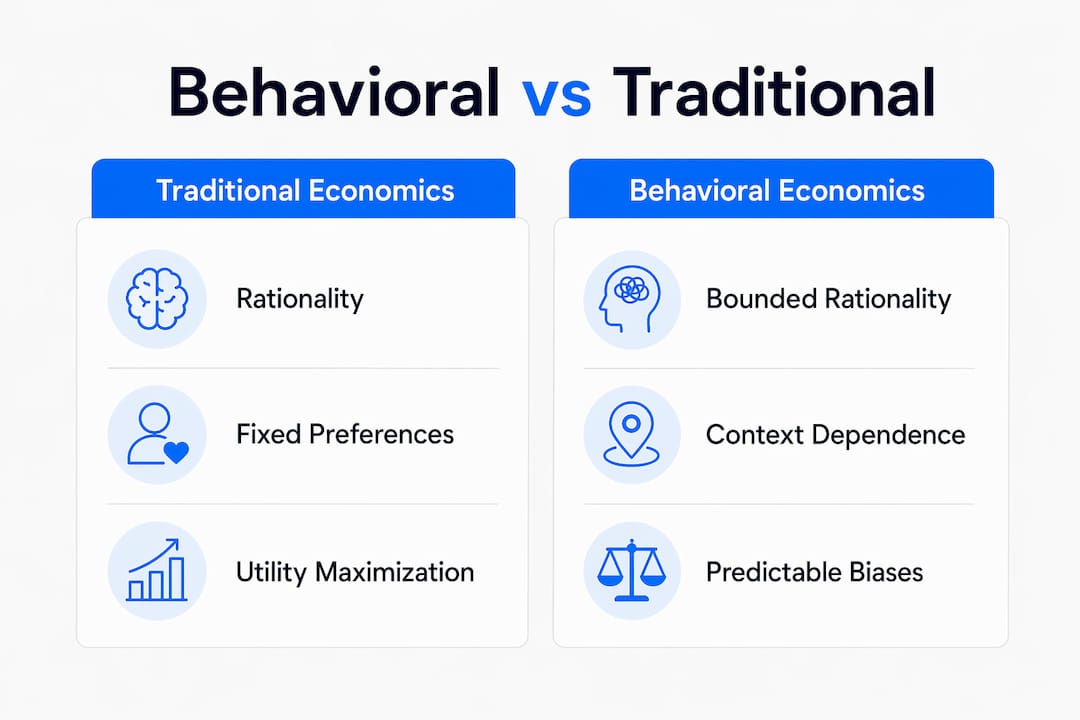

How does behavioral economics differ from traditional economics?

The contrast between behavioral economics and traditional economics comes down to one core disagreement: how rational are people, really?

| Dimension | Traditional Economics | Behavioral Economics |

|---|---|---|

| Human rationality | Assumes perfect rationality | Recognizes bounded rationality |

| Information | Assumes full information access | Accounts for cognitive limits |

| Decision errors | Treats errors as random | Views errors as systematic and predictable |

| Emotional influence | Excludes emotions from models | Incorporates emotions and biases |

| Predictive accuracy | Strong in idealized conditions | Stronger in real-world conditions |

| Policy application | Relies on incentives alone | Adds choice architecture and nudges |

Traditional economics built its models on the “rational actor,” a hypothetical person who always maximizes utility with complete information. That model works well in controlled conditions but breaks down when applied to real markets, real voters, or real savers. Behavioral economics refines, rather than replaces, classical economics by grounding its assumptions in empirical evidence.

The key insight is that human decision-making is context-dependent. Change the default option on a form, and enrollment rates shift dramatically. Change the order of items on a menu, and purchasing patterns change. These effects are invisible to classical models but entirely predictable through a behavioral lens. People exhibit predictable irrationality, using heuristics that systematically deviate from classical rationality. That predictability is what makes behavioral economics scientifically useful.

What are the practical applications of behavioral economics?

Behavioral economics moves from theory to practice across three major domains: public policy, financial markets, and product design.

Public policy and nudges

Governments worldwide use choice architecture to shift behavior without mandates or financial incentives. Choice architecture, including default settings and framing, powerfully influences decisions without changing underlying incentives. The United Kingdom’s Behavioural Insights Team applied these principles to tax compliance, organ donation, and energy conservation. Switching pension enrollment from opt-in to opt-out dramatically increased participation rates in the United States and United Kingdom. The change required no new law and no financial subsidy.

Financial markets and investment behavior

Behavioral economics explains phenomena that classical finance cannot, including market bubbles, panic selling, and the equity premium puzzle. Identifying where judgment deviates from standard economic predictions helps design better investment products and financial advice frameworks. Robo-advisors like Betterment and Wealthfront use behavioral design principles to reduce emotional trading and keep investors on track. Understanding bias in investing is now a core competency for serious financial professionals.

Product design and marketing

Consumer behavior research draws heavily on behavioral economics. Subscription services use free trials to exploit present bias. Retailers use anchor pricing to make discounts feel larger. Health apps use loss-framed notifications (“You lost your streak!”) to drive engagement. These are not accidents. They are deliberate applications of behavioral principles.

Pro Tip: Before finalizing any financial product or policy design, map the decision environment your audience faces. The default option you set will likely determine the outcome for the majority of people.

The common thread across all applications is that small design changes can shift outcomes across millions of people. That scale makes behavioral economics one of the highest-leverage tools available to policymakers and business leaders.

How do behavioral economics concepts affect personal financial decisions?

Behavioral economics is not just an academic framework. It explains the specific mistakes most people make with their own money.

-

Loss aversion distorts portfolio decisions. Investors feel the pain of a 10% portfolio drop far more intensely than the pleasure of a 10% gain. This asymmetry causes panic selling at market lows, which locks in losses and misses recoveries. Recognizing this bias is the first step toward avoiding common investment mistakes.

-

Present bias undermines saving. The future self feels abstract. The present self wants to spend. Present bias explains why people consistently undersave even when they intellectually understand the importance of retirement funding. Automatic savings programs exploit this by removing the active decision entirely.

-

Anchoring skews investment valuations. When an investor buys a stock at $100 and it drops to $60, the $100 price becomes a psychological anchor. The investor waits to “break even” rather than evaluating whether $60 is a fair price today. This anchoring effect leads to holding losing positions far longer than logic supports.

-

Overconfidence inflates risk-taking. Research consistently shows that individual investors overestimate their ability to pick winning stocks and time the market. Overconfidence leads to underdiversification and excessive trading, both of which reduce long-term returns. Understanding the psychology of investing helps counter this tendency.

-

Framing shapes saving versus investing choices. When saving is framed as “protecting your future,” people save more. When investing is framed as “risking your money,” people invest less. The underlying financial reality is the same. The framing changes the decision. Understanding the real differences between saving and investing cuts through this framing noise.

Behavioral finance, the subfield that applies behavioral economics specifically to financial markets and personal money decisions, has grown into a discipline of its own. It gives investors a vocabulary for recognizing their own biases before those biases cost them money.

Key takeaways

Behavioral economics explains that human decision-making follows predictable, measurable patterns driven by cognitive biases, not random errors, making it a practical tool for policy, finance, and product design.

| Point | Details |

|---|---|

| Core definition | Behavioral economics studies how psychology and cognition systematically shape economic choices. |

| Foundational principles | Loss aversion, bounded rationality, framing, present bias, and anchoring drive most decision errors. |

| Vs. traditional economics | Behavioral economics adds empirical realism to classical models without discarding them. |

| Real-world applications | Nudges, default options, and choice architecture shift behavior at scale across policy and markets. |

| Personal finance impact | Recognizing biases like overconfidence and loss aversion directly improves investment and saving decisions. |

Why behavioral economics is harder to apply than it looks

Most people who encounter behavioral economics for the first time make the same mistake: they treat it as a toolkit of tricks. Read about loss aversion, add a loss-framed message to your product, expect results. That approach consistently underdelivers.

The deeper issue is that behavioral economics and behavioral design are distinct. Behavioral economics explains why people behave as they do. Behavioral design applies those insights to influence behavior, often through nudging. Conflating the two leads to shallow interventions that fail when context changes. A nudge that works in one population may backfire in another because loss aversion varies by context and individual risk profile. Treating it as a fixed ratio is a mistake I see repeatedly in financial product design.

What actually works is building a genuine understanding of the underlying biases before designing any intervention. That means studying real decision environments, not just reading summaries of Kahneman. The field is maturing fast, and the practitioners who go beyond the basics are the ones producing results that hold up. For anyone serious about applying these ideas in finance or policy, the next step is not more theory. It is studying how real choice architectures succeed and fail in practice.

— Povilas

Behavioral economics resources at Finblog

Finblog covers the intersection of behavioral economics and personal finance across a growing library of practical guides. If you want to see these principles applied directly to money decisions, the financial mistakes to avoid guide breaks down how biases like anchoring and overconfidence show up in real portfolios. The personal finance myths guide addresses framing-driven misconceptions that cost readers money every year. For a broader starting point, Finblog’s main resource hub connects you to guides on investing psychology, risk management, and smarter saving strategies built around how people actually make decisions.

FAQ

What is the simplest behavioral economics definition?

Behavioral economics is the study of how psychological biases and cognitive limits cause people to make economic decisions that deviate from classical rational-actor predictions. It combines insights from psychology, neuroscience, and economics.

Who founded behavioral economics?

Daniel Kahneman and Amos Tversky are the field’s foundational figures. Their work on Prospect Theory, published in 1979, established the empirical basis for behavioral economics and earned Kahneman the Nobel Prize in Economics in 2002.

How does loss aversion affect financial decisions?

Loss aversion causes investors to feel the pain of losses roughly twice as intensely as the pleasure of equivalent gains. This leads to holding losing investments too long and selling winning ones too early.

What is choice architecture in behavioral economics?

Choice architecture refers to the design of the environment in which people make decisions. Default options, the order of choices, and framing all influence outcomes without changing the underlying incentives or available options.

Is behavioral economics the same as behavioral finance?

Behavioral economics is the broader field covering all economic decisions. Behavioral finance is a subfield that applies behavioral economics principles specifically to financial markets, investor psychology, and personal money management.