TL;DR:

- REITs allow investors to gain exposure to large-scale income-producing real estate without property management or large capital requirements. They generate returns primarily through dividends and property value appreciation, offering higher yields than many stock investments. Proper understanding of tax treatment, diversification, and real estate fundamentals is essential for using REITs effectively in a balanced portfolio.

Thousands of everyday investors own a piece of commercial skyscrapers, shopping centers, and medical office buildings without ever signing a mortgage or calling a property manager. They do it through REITs, and most working professionals have no idea how powerful this tool can be. A real estate investment trust (REIT) lets you participate in large-scale real estate markets the same way you buy a stock, with none of the landlord headaches. This guide breaks down how REITs work, what they pay you, how they’re taxed, and how to use them wisely in your portfolio.

Table of Contents

- What is a REIT? Understanding the basics

- How REITs generate returns for investors

- Comparing REITs and direct property investments

- Tax considerations and common pitfalls with REIT investing

- How REITs fit into a diversified investment portfolio

- Our perspective: Why REITs are often underestimated — and how to use them wisely

- Explore more with Finblog

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| REITs simplify real estate | REITs let investors profit from real estate markets without owning physical property. |

| Income and growth potential | REITs pay regular dividends and offer possible price appreciation for investors. |

| Easy portfolio diversification | Including REITs in your portfolio can lower risk and broaden investment exposure. |

| Tax rules matter | REIT dividends are taxed as ordinary income, so smart tax strategies can increase returns. |

| Accessible to most investors | You can invest in REITs with minimal capital through brokerages and retirement accounts. |

What is a REIT? Understanding the basics

A real estate investment trust (REIT) is a company that owns, operates, or finances income-producing real estate. Congress created the REIT structure in 1960 to give ordinary investors access to large commercial properties that were previously available only to wealthy institutions. Think of it like a mutual fund, but instead of stocks or bonds, the fund holds real estate assets.

REITs are legally required to meet strict criteria to qualify for their special tax status. The most important rule: REITs must distribute at least 90% of their taxable income to shareholders as dividends each year. That single requirement is what makes REITs one of the most consistent income-generating investments available.

The types of real estate held inside REITs vary widely. You can invest in:

- Equity REITs, which own and manage physical properties like office towers, apartment complexes, hotels, data centers, and retail malls

- Mortgage REITs (mREITs), which finance real estate by lending money or buying mortgage-backed securities

- Hybrid REITs, which combine both equity and mortgage strategies

- Specialized REITs, which focus on niche sectors like cell towers, self-storage facilities, senior housing, or timberland

The biggest difference between a REIT and direct property ownership is control versus simplicity. When you buy a rental property, you control everything from the tenant selection to the repair bills. With a REIT, a professional management team handles all of that. You just own shares.

Pro Tip: If you’re new to real estate investing, equity REITs are generally the easiest starting point because their income is more predictable and their business model is simpler to understand than mortgage REITs.

How REITs generate returns for investors

REITs make money in two main ways: rental income from tenants occupying their properties, and capital appreciation when property values rise over time. Because REITs must pay out the majority of their income, investors receive most of those gains directly as dividends rather than waiting for a share price increase.

Here’s a clear breakdown of how REIT returns actually reach you:

- Dividend income. REITs collect rent from tenants and distribute that income to shareholders, often on a quarterly basis. Some REITs pay monthly dividends, which is attractive for investors who rely on passive income to supplement their salary.

- Share price appreciation. As the underlying property values increase and the REIT grows its portfolio, the market price of REIT shares tends to rise. This creates capital gains for long-term investors.

- Dividend reinvestment. Many brokerages allow you to automatically reinvest REIT dividends to purchase more shares, compounding your returns over time without any extra effort.

- Return of capital distributions. Some REIT dividends include a “return of capital” component, which is not taxable immediately but reduces your cost basis for future tax purposes.

“Real estate cannot be lost or stolen, nor can it be carried away. Purchased with common sense, paid for in full, and managed with reasonable care, it is about the safest investment in the world.” — Franklin D. Roosevelt

The dividend yields on REITs tend to be higher than those on typical S&P 500 companies. Many established REITs yield between 3% and 6% annually, and some specialty REITs yield even more. That gap matters enormously when you’re building a portfolio that needs to generate regular cash flow.

Pro Tip: Compare a REIT’s funds from operations (FFO) rather than just its earnings per share. FFO is the industry standard metric that strips out depreciation and gives you a truer picture of a REIT’s cash-generating ability.

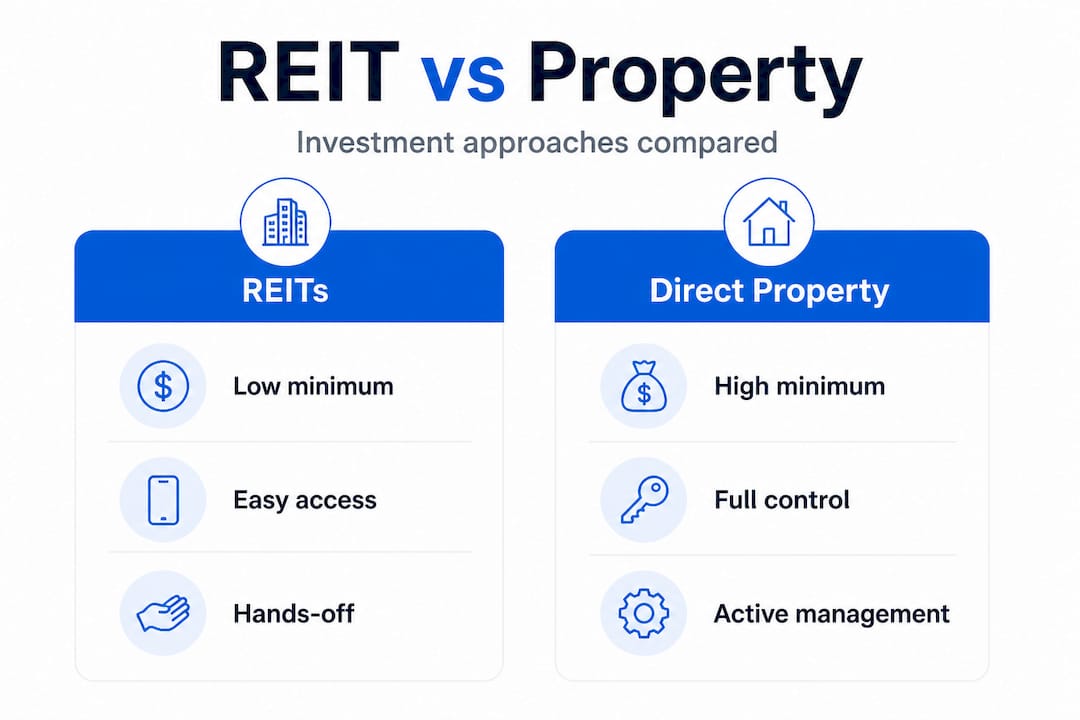

Comparing REITs and direct property investments

After seeing how REITs work for investors, it’s useful to compare them to buying property yourself. Both approaches give you real estate exposure, but they serve very different investor profiles and life situations.

| Factor | REITs | Direct property |

|---|---|---|

| Minimum investment | As low as one share (often under $100) | Typically $20,000+ for a down payment |

| Liquidity | Highly liquid, sold on stock exchanges | Illiquid, months to sell |

| Management burden | Zero, professionally managed | High, you handle tenants and repairs |

| Diversification | Built-in across many properties | Usually one or two properties |

| Control | None over specific decisions | Full control over your assets |

| Tax benefits | Section 199A deduction may apply | Depreciation, mortgage interest deduction |

| Leverage | Managed by the REIT | You control your own financing |

When you look at this side by side, neither option is universally better. Direct property investment rewards hands-on investors who understand local markets and are comfortable managing assets over decades. For most working professionals with limited time and capital, REITs offer a much more practical entry point.

Real estate vs REIT investing comes down to a few honest questions: How much time can you dedicate? How much capital can you lock up? And how comfortable are you with illiquid assets during a market downturn?

Here’s what REITs do better than direct property in most cases:

- They let you invest in geographies and property types you couldn’t access locally

- They provide instant diversification across dozens or hundreds of properties

- They allow you to rebalance or exit a position in minutes, not months

- They require no property management knowledge or experience

Direct property still wins on leverage potential and tax deductions for active real estate investors. But for the majority of professionals who want real estate exposure without becoming landlords, REITs are the smarter, simpler path.

Tax considerations and common pitfalls with REIT investing

Comparing REITs and property investing naturally leads to the next key issue: taxes and the common mistakes investors make. REITs have a few tax quirks that every investor must understand before putting money to work.

How REIT dividends are taxed

Unlike qualified stock dividends, most REIT dividends are taxed as ordinary income at your regular federal tax rate. That means if you’re in the 32% tax bracket, your REIT dividends could be taxed at 32% rather than the 15% or 20% rate that applies to qualified dividends from most stocks.

The good news is that tax-efficient REIT investing is absolutely achievable with the right account strategy.

| REIT account type | Tax treatment | Best for |

|---|---|---|

| Taxable brokerage account | Dividends taxed as ordinary income | Investors in lower tax brackets |

| Traditional IRA or 401(k) | Tax deferred until withdrawal | High earners wanting to defer taxes |

| Roth IRA | Tax-free growth and withdrawals | Long-term investors expecting growth |

The Section 199A deduction

Under current U.S. tax law, investors may qualify for a 20% deduction on qualified REIT dividends through the Section 199A deduction. This deduction effectively reduces your taxable REIT income, making REITs more competitive on an after-tax basis than many investors realize. Check with a tax advisor to confirm your eligibility.

Common mistakes REIT investors make

- Holding high-yield REITs in a taxable account when a tax-advantaged account is available

- Ignoring the difference between ordinary dividends, qualified dividends, and return of capital

- Buying a REIT purely for yield without checking its FFO growth rate or debt levels

- Overloading a portfolio with a single REIT sector (for example, holding only retail REITs)

- Failing to review REIT tax planning strategies before tax season

Pro Tip: The simplest tax move you can make is to hold your highest-yielding REITs inside a Roth IRA. Over a 20-year period, tax-free compounding on a 5% dividend yield can add a remarkable amount to your final balance compared to paying ordinary income tax on those dividends annually.

How REITs fit into a diversified investment portfolio

With tax and investment strategy in mind, let’s look at how REITs can improve your overall portfolio balance. Real estate as an asset class historically has a low correlation with stocks and bonds. That means when your equity holdings drop sharply in a market selloff, your REIT positions don’t necessarily fall by the same amount or at the same time.

That low correlation is the core reason financial advisors often recommend a REIT allocation as part of a diversified investment strategy. It doesn’t eliminate risk, but it smooths out the ride.

How much should you allocate? Common guidance from institutional portfolio managers suggests a 5% to 15% allocation to real estate, including REITs, depending on your age, income needs, and risk tolerance. A younger investor building wealth might lean toward growth-oriented REITs in industrial and data center sectors. An investor nearing retirement might favor residential or healthcare REITs that generate predictable income.

Here are the core benefits of including REITs in a diversified portfolio:

- Income generation. Regular dividends from REITs can supplement salary income or replace it in retirement

- Inflation protection. Many REIT leases include rent escalation clauses that grow with inflation, protecting purchasing power

- Sector variety. Different REIT types respond to different economic forces, giving you meaningful diversification

- Accessibility. You can build a real estate allocation with as little as a few hundred dollars spread across multiple REIT shares

One important caution: don’t fall into the trap of over-concentrating in a single REIT type. Many investors load up on retail or office REITs because of high yields, only to be hit hard when those sectors face structural pressure. The value of diversification applies just as strongly within the REIT category as it does across your broader portfolio.

A practical approach is to use a REIT index fund or exchange-traded fund (ETF) to gain diversified real estate exposure in a single transaction. This gives you a slice of dozens of REITs simultaneously, reducing concentration risk without requiring you to research individual companies. For more data-backed insights on diversification, it’s worth studying how different asset mixes have performed across market cycles.

Our perspective: Why REITs are often underestimated — and how to use them wisely

Most investors who ignore REITs do so because they look boring. No flashy earnings surprises. No viral product launches. Just properties collecting rent and paying dividends. That perception is costing people real money.

Here’s the insight most investment content skips over: REITs don’t just offer income. They offer institutional-grade real estate that individual investors could never access otherwise. A share of a major data center REIT, for example, gives you a stake in the infrastructure powering cloud computing. A healthcare REIT gives you exposure to senior housing demand driven by an aging population. These are macro trends with decades of runway, and REITs let you invest in them directly.

The biggest mistake we see investors make is treating REITs exactly like high-yield stocks and chasing the highest dividend yield without understanding the underlying business. A 9% yield sounds exciting until the REIT cuts its dividend because it over-leveraged its balance sheet. A 4% yield from a well-managed industrial REIT with low debt and strong FFO growth will outperform that flashy 9% yield over a decade almost every time.

The second mistake is failing to understand that REITs require a real estate mindset, not just a stock market mindset. You need to think about lease expiration schedules, tenant credit quality, occupancy rates, and capital expenditure requirements. These are not complicated once you learn them, but they are different from how you evaluate a technology stock.

Our honest recommendation: build a purposeful REIT allocation using strategic diversification principles and hold it through market cycles. Don’t trade REITs like stocks. Let the income compound. Use tax-advantaged accounts wherever possible. And spend more time understanding what’s inside your REIT than worrying about what the share price did last week. The investors who treat REITs with patience and discipline consistently outperform those who treat them as trading vehicles.

Explore more with Finblog

If you’re ready to go beyond the basics and build a smarter, more resilient investment portfolio, Finblog is built for exactly that. From in-depth guides on dividend investing and tax-efficient strategies to plain-language breakdowns of portfolio diversification and passive income, we cover the topics that serious investors actually need. Whether you’re evaluating your first REIT or restructuring a portfolio you’ve held for years, our resources are designed to help you make confident, informed decisions. Explore our full library and take the next step toward building wealth that works harder for you.

Frequently asked questions

How do I invest in a REIT?

Most investors can purchase REIT shares through a standard brokerage or retirement account the same way they’d buy any publicly traded stock, with no special application required.

Are REIT dividends taxed differently than stock dividends?

Yes. Most REIT dividends are taxed as ordinary income at your regular tax rate, whereas qualified stock dividends often benefit from lower long-term capital gains rates of 15% or 20%.

What’s the minimum investment for a REIT?

You can start investing in a publicly traded REIT for as little as the cost of a single share, which can range from under $20 to several hundred dollars depending on the company.

Can REITs help with portfolio diversification?

Absolutely. REITs have historically shown a lower correlation with stocks and bonds, which means they can reduce overall portfolio volatility while adding a consistent income stream.

What are the biggest risks of REIT investing?

The primary risks include property market downturns, rising interest rates (which increase REIT borrowing costs and compete with dividend yields), and sector concentration if your holdings are too narrowly focused in one property type.

Recommended

- Understanding Real Estate vs Stocks: Comprehensive Insights – Finblog

- Understanding Dividend Investing Guide for Beginners – Finblog

- 7 Best Passive Income Ideas for Smart Investors Explained – Finblog

- Understanding Tax Efficient Investing: How It Works – Finblog

- Step-by-step real estate investing in Europe: a clear guide – Article | Crowdinform Investment Guides Real estate crowdfunding