MicroStrategy (NASDAQ: MSTR) reports Q1 2025 earnings on Thursday, May 2, after market close — and it’s one of the most high-stakes events in the crypto-linked stock universe. As the largest corporate holder of Bitcoin and a business intelligence software company, MicroStrategy straddles two volatile sectors — software and crypto, making its earnings one of the most closely watched by both Wall Street and Main Street.

Here’s a deep dive into what to expect, what’s driving results, where the risks lie, and how analysts are positioned.

Expected Q1 2025 Results

What’s at stake:

MicroStrategy is expected to report:

- EPS estimate: -$0.02 (Yahoo Finance, MarketBeat, TradingEconomics)

- Revenue estimate: ~$134M (Yahoo Finance, MarketBeat, Nasdaq)

- Previous Year Revenue: $121M

- Previous Year EPS: -$0.83

Why it matters: A smaller-than-expected loss or a surprise profit could ignite the stock, but as always with MSTR, Bitcoin direction will matter even more.

Key Focus Areas

Let’s break down the real drivers that will shape investor reaction.

✅ Bitcoin Holdings and Market Impact

- MicroStrategy holds over 214,000 Bitcoin, valued at ~$13B at recent prices (TheStreet, TradingView, CNBC).

- Bitcoin soared ~50% in Q1, hitting above $70,000 before retreating slightly.

Accounting wrinkle: Because of GAAP rules, only unrealized Bitcoin losses (not gains) are reported on the P&L. Still, analysts and investors will be adjusting reported numbers to reflect the true underlying crypto position.

Why it matters: MSTR’s stock behaves like a leveraged Bitcoin ETF, and its Bitcoin commentary and accumulation strategy often overshadow software results.

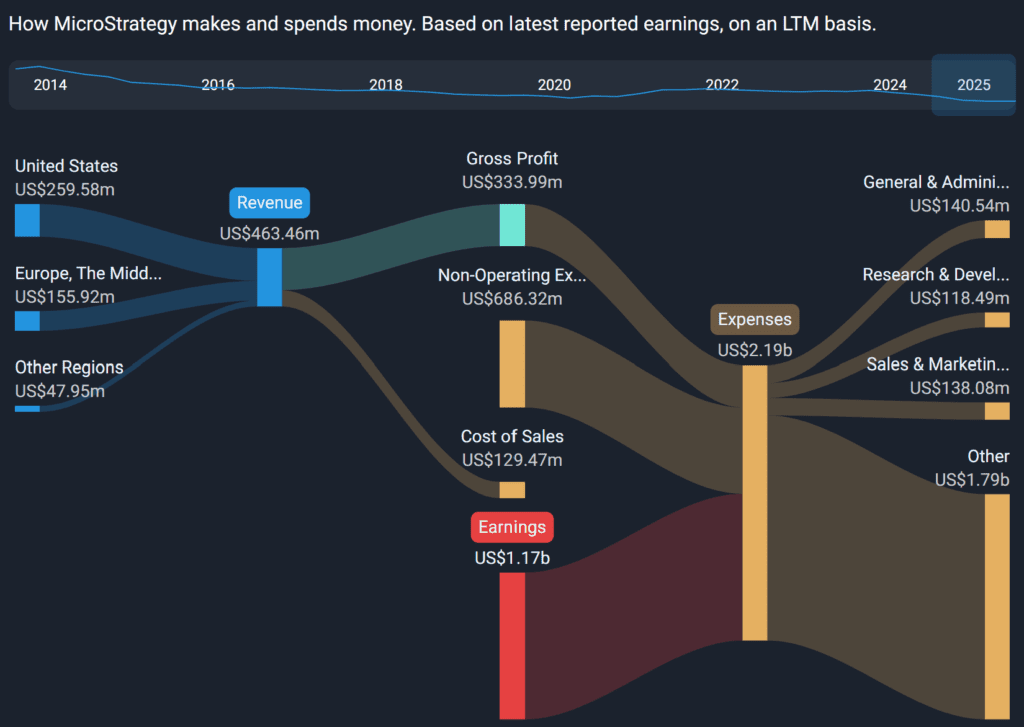

✅ Software Business Performance

- Expected flat to +5% YoY revenue growth from enterprise analytics software.

- Focus on cloud subscriptions, new customer wins, and AI-powered analytics solutions.

Why it matters: While overshadowed by Bitcoin, MicroStrategy’s software business provides operational stability and cash flow.

✅ Capital Strategy and Leverage

- ~$2.5B in long-term debt, much of it used to buy Bitcoin at lower prices.

- Debt-to-equity ratio: 0.4 (lower than peers, conservative on paper, but leverage is hidden via BTC exposure).

Why it matters: The market will be watching whether the company refinances debt, issues new convertibles, or sells shares to fund more BTC purchases.

✅ Bitcoin Accumulation Strategy

CEO Michael Saylor has been unapologetic:

“We’re buying more Bitcoin — period.”

Any update on additional BTC buys will be the most market-moving part of the call.

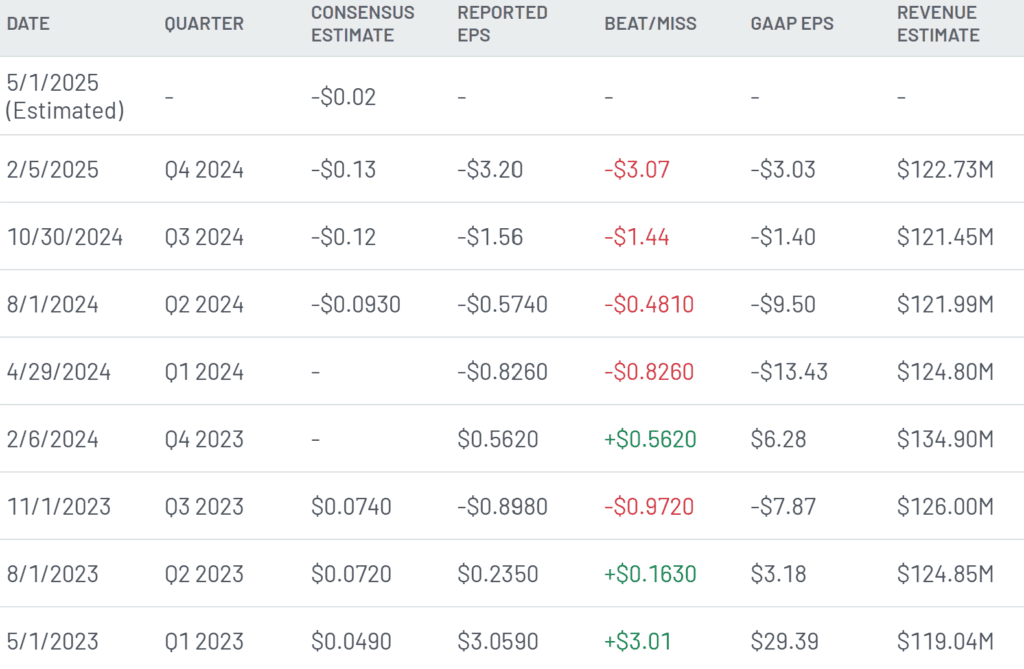

Past Earnings Performance

Recent history shows why this stock is so volatile:

| Quarter | EPS Estimate | EPS Actual | Price Change % Next Day |

|---|---|---|---|

| Q4 2024 | $0.06 | -$3.20 | -3.0% |

| Q3 2024 | -$0.14 | -$1.56 | -1.0% |

| Q2 2024 | -$0.11 | -$0.76 | -4.0% |

| Q1 2024 | $0.03 | -$0.83 | -18.0% |

Key takeaway: Even big misses don’t always crush the stock — it’s all about BTC momentum and forward guidance.

Performance and Sentiment Snapshot

- Current price (Apr 29): $381.45

- 52-week return: +225% (!!)

- Market cap: ~$22B

- P/E ratio: Not meaningful due to crypto-related accounting swings

Why it matters: Long-term shareholders are highly bullish, but they need confirmation that BTC exposure is still paying off.

Analyst Ratings and Sentiment

- 6 analyst ratings → Consensus: Buy

- Average 1-year price target: $498.17 (~30.6% upside)

- Latest updates:

- HC Wainwright → Initiated at Buy (Apr 2025)

- Barclays → Maintained Overweight (Feb 2025)

- Keefe, Bruyette & Woods → Initiated at Outperform (Feb 2025)

Peer Comparison Snapshot

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

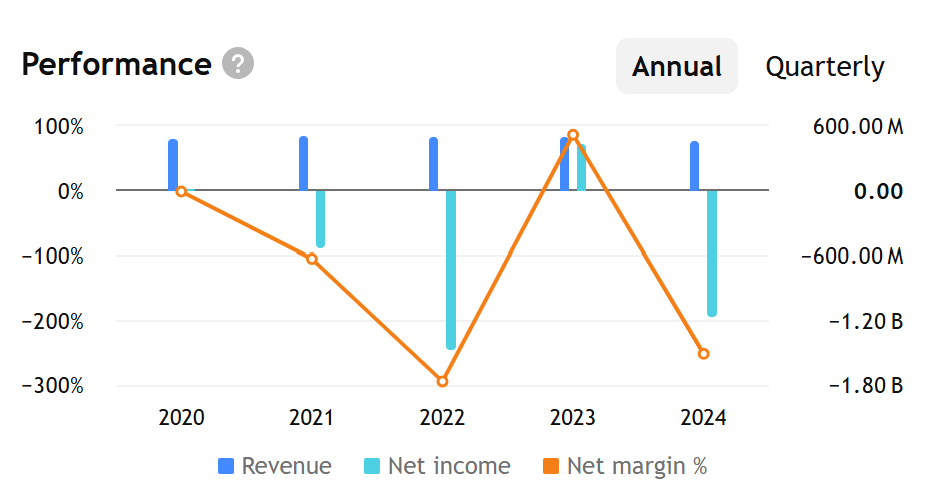

| MicroStrategy | Buy | -3.04% | $86.5M | -6.1% |

| AppLovin | Buy | +44.0% | $1.05B | +59.0% |

| Cadence Design | Outperform | -8.4% | $1.14B | +5.8% |

| Synopsys | Outperform | -3.7% | $1.19B | +3.2% |

Key insight: MSTR leads on gross profit but trails badly on growth and profitability metrics.

Challenges and Headwinds

- BTC volatility: A ~12% correction from March highs into April

- Accounting limitations: Only BTC losses show on P&L; upside is hidden

- Debt load: ~$2.5B in long-term debt

- Software competition: Tableau, Microsoft Power BI, Google Analytics

- Regulatory overhang: Crypto regulation risk is growing

Bullish Drivers

- Massive BTC exposure, amplified by leverage

- Potential BTC rally tailwind after spot ETF approvals

- Saylor’s unshakable “buy more BTC” philosophy

- Improving software subscriptions and enterprise cloud adoption

- High retail and institutional attention

Bearish Risks

- Extreme dependence on Bitcoin

- Negative revenue growth and EPS track record

- Balance sheet risk if BTC corrects sharply

- Software business trailing competitors

- High valuation tied to crypto cycles

Earnings Surprise History

- Mixed beats/misses; stock swings 10–20% post-report (MarketBeat, Nasdaq)

- Last quarter miss: EPS -$3.20 vs. est. +$0.06 → only -3% stock drop

Why it matters:

Expect big moves regardless of results — this is a sentiment and Bitcoin-driven stock.

Conclusion

MicroStrategy’s Q1 2025 earnings will be a referendum on Bitcoin, leverage, and conviction.

For bulls, it’s a hyper-levered BTC play; for bears, it’s a software company that’s become a crypto casino chip. The key questions on the call will be:

- Is Saylor buying more BTC?

- How’s the software transition to cloud + AI progressing?

- Can they manage debt if BTC cools off?

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related:

What Analysts Think of BigBear.ai Stock Ahead of Earnings?

What Analysts Think of Amazon Stock Ahead of Earnings?

Apple Q2 2025 Earnings Preview and Prediction: What to Expect

Eli Lilly Q1 2025 Earnings Preview and Prediction: What to Expect

UK-US trade talks ‘moving in a very positive way’, says White House

Trump Eases Auto Tariffs to Avoid Industry Meltdown

Trump Administration Lays Out Roadmap to Streamline Tariff Talks

Trump Pushes Plan to Replace Income Taxes with Tariffs: “A Bonanza for America!”

California Overtakes Japan to Become Fourth Largest Economy in World

“Made in USA”? It’s More Complicated Than You Think

Conflicting US-China talks statements add to global trade confusion