TL;DR:

- Most retirees face their first significant tax bill in retirement due to unplanned withdrawals from traditional IRAs or 401(k)s. Effective withdrawal strategies involve understanding RMD rules, planning in low-income years for Roth conversions, and sequencing distributions to minimize taxes and preserve wealth. Regular verification and strategic use of tools like QCDs and specific share sales can significantly optimize long-term tax savings.

Most retirees are blindsided by their first big tax bill in retirement. You’ve spent decades saving, and then the IRS shows up demanding a cut of every dollar you pull from your traditional IRA or 401(k). The mechanics of tax-efficient withdrawals are not complicated, but they require a deliberate plan most people never build. This guide walks you through exactly what you need to know: how required minimum distributions work, how to prepare your finances before withdrawals begin, and how to execute a withdrawal sequence that keeps more of your money in your pocket.

Table of Contents

- Understanding required minimum distributions (RMDs) and their tax impact

- Preparing for tax-efficient withdrawals: assessment and planning steps

- Executing withdrawals strategically: tactical steps for tax savings

- Verifying your withdrawal strategy: avoiding common mistakes and ensuring compliance

- Why early Roth conversions and charitable giving are game-changers for retirees

- Explore tailored retirement tax strategies with our expert resources

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Start RMDs at 73 | You must begin required minimum distributions by age 73 to avoid steep IRS penalties. |

| Plan Roth conversions early | Converting to Roth IRAs before RMDs start lowers future taxable withdrawals and Medicare surcharges. |

| Use QCDs to reduce taxes | Qualified charitable distributions let you donate directly from IRAs, lowering taxable income without itemizing deductions. |

| Manage brokerage gains | Keep taxable income low to utilize the 0% capital gains bracket by timing sales and specific share identification. |

| Automate and verify withdrawals | Set up systematic withdrawals and confirm custodian calculations annually to avoid costly errors and penalties. |

Understanding required minimum distributions (RMDs) and their tax impact

To build real retirement withdrawal strategies, you first need to understand the rules you’re working around. RMDs are mandatory annual withdrawals the IRS requires from traditional IRAs and 401(k)s once you reach a certain age. Ignore them, and the penalties are steep.

IRS rules for 2026 require RMDs from traditional IRAs and 401(k)s starting at age 73, with significant penalties for missed amounts. Your RMD amount is calculated by dividing your prior year-end account balance by an IRS life expectancy factor from their Uniform Lifetime Table. If your IRA balance was $500,000 at the end of 2025 and your factor is 26.5, your 2026 RMD is roughly $18,868.

Here is what trips people up most:

- First RMD deadline: You have until April 1 of the year after you turn 73. Sounds generous. But delaying to April 1 means you also take a second RMD by December 31 of that same year, stacking two distributions into one tax year and potentially pushing you into a higher bracket.

- Missed RMD penalty: A 25% penalty applies to any amount you should have withdrawn but did not. That can be reduced to 10% if corrected promptly.

- Multiple accounts: You can aggregate RMDs across traditional IRAs and withdraw from any single account, but 401(k)s require separate calculations and withdrawals.

| Account type | RMD required? | Starting age | Can aggregate? |

|---|---|---|---|

| Traditional IRA | Yes | 73 | Yes (across IRAs) |

| 401(k) | Yes | 73 | No (per account) |

| Roth IRA | No | N/A | N/A |

| Roth 401(k) | No (as of 2024) | N/A | N/A |

Pro Tip: Set up automatic systematic withdrawals through your custodian. Automation removes the risk of forgetting a deadline and creates a predictable income stream you can plan around. Most major custodians offer this at no extra cost.

The moment you treat RMDs as a passive obligation rather than an active tax event, you start losing money you didn’t have to. Consider optimizing retirement savings as an ongoing process, not a one-time setup.

Preparing for tax-efficient withdrawals: assessment and planning steps

Having grasped RMD essentials, you can now prepare your finances to minimize taxes when withdrawing funds. The retirees who pay the least in taxes are not the ones with the smallest accounts. They’re the ones who mapped out their income sources years before their first RMD.

Start with a full picture of every income source you’ll have in retirement:

- Social Security benefits (partially taxable depending on combined income)

- Pension payments (usually fully taxable)

- Traditional IRA and 401(k) distributions (fully taxable as ordinary income)

- Roth IRA distributions (tax-free if account is over 5 years old)

- Taxable brokerage account gains (taxed at capital gains rates)

- Part-time work or rental income

Once you see everything together, you can identify your effective tax bracket and find gaps worth filling. The strategy is to manage retirement tax brackets by maximizing lower brackets early through IRA withdrawals or Roth conversions before higher future brackets are forced by RMDs.

The “low-income gap” is your most valuable window. For many retirees, the years between actual retirement and age 73 are a golden period of lower taxable income. This is exactly when Roth conversions make the most sense.

Here is how to use that window effectively:

- Calculate your current bracket ceiling. Find out how much room you have before hitting the next bracket. For 2026, the 12% bracket for married filing jointly ends at $94,300 in taxable income.

- Convert traditional IRA funds to Roth up to that ceiling. You pay tax now at 12% instead of potentially 22% or higher once RMDs and Social Security stack on top.

- Model your future RMD size. Use your projected account balance at age 73 and the IRS life expectancy factor to estimate what mandatory withdrawals will look like. If they push you into a higher bracket, convert more now.

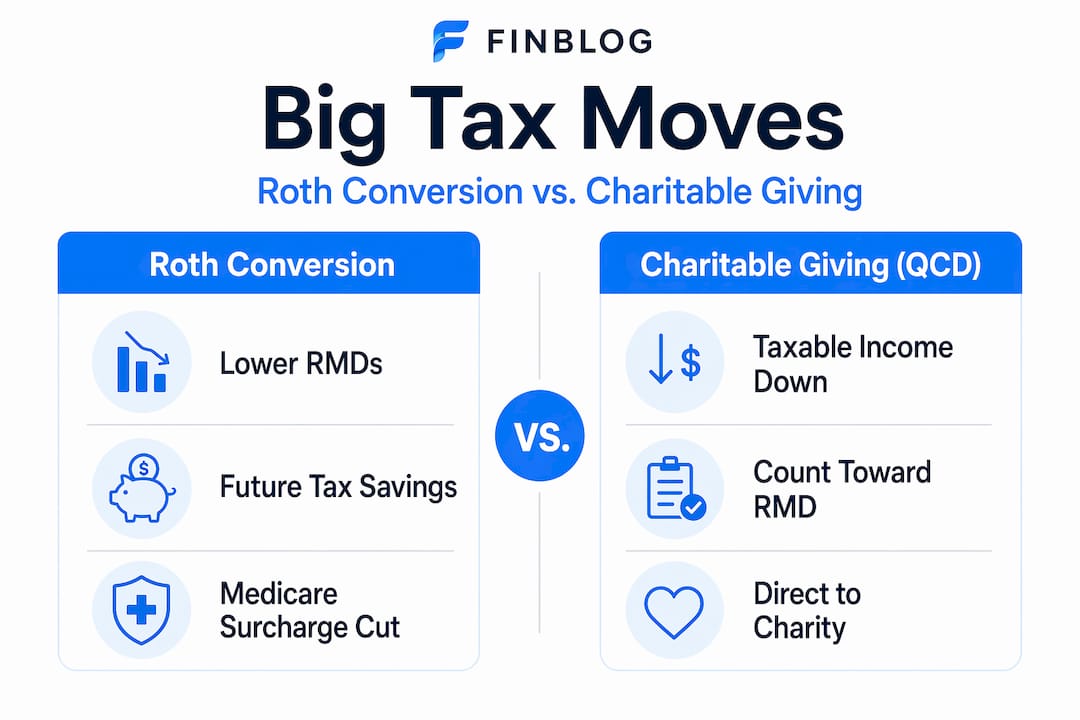

- Add qualified charitable distributions to the plan. If you are charitably inclined and over 70½, Roth IRA conversions paired with QCDs create a remarkably efficient combination.

- Model Social Security timing last. Delaying benefits to age 70 increases your monthly check but also adds taxable income. Run the numbers against your RMD projections before committing.

Pro Tip: Use a free online RMD calculator to project your age-73 distribution amounts based on current account balances and assumed growth rates. Seeing the number concretely often motivates action during the conversion window that vague awareness never does.

The tax planning steps you take before your first RMD matter more than almost anything you do after. This is where the real leverage is.

Executing withdrawals strategically: tactical steps for tax savings

With plans ready, now execute withdrawals tactically to preserve wealth through every distribution decision you make.

The most proven approach is withdrawal sequencing: pulling from accounts in an order that keeps your total tax bill as low as possible across your lifetime, not just the current year.

The withdrawal order that works:

- Satisfy all RMDs first. This is not optional, and meeting it clears the mandatory obligation.

- Draw from taxable brokerage accounts next, focusing on shares with the highest cost basis to minimize realized gains.

- Pull from traditional IRAs to fill your current tax bracket, especially during pre-Social Security years.

- Leave Roth IRAs alone as long as possible. Tax-free growth is compounding in your favor.

Managing brokerage account withdrawals is where real precision pays off. Tax-free capital gains harvesting is possible when married couples filing jointly keep taxable income below $98,900, preserving the 0% long-term capital gains rate. In practical terms, this means you could sell appreciated shares and owe nothing in federal tax on those gains, as long as you manage total income carefully.

Qualified charitable distributions deserve their own spotlight. QCDs satisfy RMDs without adding to your taxable income, which also lowers Medicare premium surcharges (called IRMAA) and reduces the portion of Social Security subject to tax. You can give up to $111,000 per year directly from your IRA to charity through a QCD. Unlike writing a check and taking a deduction, QCDs work even if you take the standard deduction.

| Withdrawal source | Tax treatment | Best used when |

|---|---|---|

| RMD from traditional IRA | Ordinary income | Mandatory; satisfy first |

| Taxable brokerage gains | 0% to 20% capital gains | Income below $98,900 (MFJ) |

| Traditional IRA (beyond RMD) | Ordinary income | Filling lower brackets |

| Roth IRA | Tax-free | Last resort; let it grow |

| QCD from IRA | Excluded from income | Charitably inclined, 70½+ |

A concrete example: A married couple retired at 65, not yet receiving Social Security or RMDs, could withdraw $30,000 from a traditional IRA, direct $20,000 as a QCD to their favorite charity, and sell $50,000 in appreciated brokerage shares, all while staying within the 0% capital gains zone and the 12% income bracket. That is a withdrawal sequencing strategy that funds lifestyle needs while leaving minimal tax.

Pro Tip: When selling shares in a brokerage account, use specific identification, not FIFO (first in, first out), to choose which shares to sell. Selling your highest-cost-basis lots first keeps realized gains small and your tax bill lower. Most custodians allow this method with a simple instruction at the time of sale.

One more consideration: capital gains tax management becomes especially important in years when RMDs or conversions push income higher. Timing brokerage sales in lower-income years and deferring them in higher-income years is a move that takes minutes to plan and can save thousands.

Verifying your withdrawal strategy: avoiding common mistakes and ensuring compliance

After executing withdrawals, the work is not done. Regular verification keeps you compliant and catches errors before they become expensive.

The most overlooked mistake retirees make is trusting their custodian’s RMD calculation without checking it. Custodians do make errors, and you, not them, are responsible for the penalty if the amount is wrong. Pull your prior year-end balance, look up your IRS life expectancy factor, and verify the number yourself every January.

Common compliance mistakes to watch for:

- Forgetting an inherited IRA. Inherited accounts have their own RMD rules and schedules entirely separate from your own accounts.

- Ignoring IRMAA thresholds. A single income spike from a large Roth conversion or RMD can trigger Medicare Part B and D surcharges for two years running. The IRMAA surcharge kicks in when your modified adjusted gross income exceeds $106,000 (individual) or $212,000 (married) in 2026.

- Treating RMDs as a ceiling. You can always take more than your RMD. In low-income years, withdrawing extra from your traditional IRA fills lower brackets and reduces future RMD size.

If you miss an RMD, file IRS Form 5329 immediately. The penalty drops from 25% to 10% if corrected within two years. Prompt action matters more than the mistake itself.

The best habit is a quarterly review: check distributions taken, compare against your bracket plan, and assess whether any Roth conversions or brokerage sales should be pulled forward or pushed to the following year. These tax saving strategies are most effective when treated as a living plan, not a one-time decision.

Pro Tip: Set a calendar reminder for October 1 each year to review your year-to-date income and projected distributions. This gives you three months to make adjustments, convert additional IRA funds, or complete charitable giving before December 31.

Why early Roth conversions and charitable giving are game-changers for retirees

Most retirement tax articles focus on sequencing withdrawals correctly and hitting RMD deadlines. That is necessary. But it is not where the real money is saved.

The biggest lifetime tax wins for retirees come from decisions made before age 73, not from optimizing what you withdraw after mandatory distributions begin. And yet most people wait.

Roth conversions before age 73 directly reduce the size of future RMDs and can lower Medicare surcharges, saving tens of thousands over a lifetime. Here is the counterintuitive part: paying tax now, voluntarily, on a Roth conversion at 12% saves you from paying it involuntarily at 22% or 24% once Social Security, RMDs, and other income stack up after 73. The math is not close. A retiree who converts $100,000 over five years between ages 65 and 70 at a 12% marginal rate pays $12,000 in tax. The same $100,000 withdrawn at 22% later costs $22,000. That is $10,000 in savings from one decision made early.

QCDs are equally underused and can lower taxable income meaningfully even when taking the standard deduction, a fact many retirees miss entirely. A traditional charitable deduction only helps if your itemized deductions exceed the standard deduction, which for married couples over 65 sits above $31,000 in 2026. A QCD bypasses this entirely because the income never enters your return in the first place.

The strategy that consistently produces the best outcomes combines these two moves: convert aggressively in the low-income gap years, and use QCDs to handle charitable giving goals without inflating taxable income. Pair both with delayed Social Security to age 70, and you have a system where Roth IRA basics and charitable planning reduce your lifetime tax bill by six figures in many cases. Not theoretical. Documented, calculable, and available to most retirees who plan a few years early.

Explore tailored retirement tax strategies with our expert resources

Tax-efficient retirement withdrawals require more than understanding the rules. They require a plan built around your specific accounts, income sources, and timeline. At finblog.com, you will find detailed guidance on everything from RMD calculations and retirement tax strategy resources to Roth conversion timing, capital gains harvesting, and Social Security optimization. Whether you are five years from retirement or already navigating mandatory distributions, our articles, tools, and calculators give you the frameworks to act with confidence. Explore our full library to build a withdrawal plan that keeps more of what you have worked a lifetime to save.

Frequently asked questions

When do I need to start taking required minimum distributions (RMDs)?

You must begin RMDs from traditional IRAs or 401(k)s at age 73, with your first distribution due by April 1 of the following year; delaying to that deadline means taking two distributions in one calendar year, which can push your tax bracket higher. IRS rules for 2026 confirm these starting requirements and penalties.

How can qualified charitable distributions (QCDs) reduce my taxable income?

QCDs let you donate up to $111,000 per year directly from your IRA to an eligible charity, counting toward your RMD but excluded entirely from your taxable income, which also lowers Medicare surcharges and reduces Social Security taxation. QCDs lower taxable income even when you take the standard deduction, unlike regular charitable contributions.

Can I sell investment shares from my brokerage account tax free?

Yes, if your taxable income stays below $98,900 as a married couple filing jointly, you pay 0% on long-term gains from shares held over one year. Careful timing of brokerage sales relative to other income is the key.

What happens if I miss my RMD deadline?

Missing an RMD triggers a 25% penalty on the amount not withdrawn, but filing Form 5329 promptly and correcting the shortfall within two years can reduce that penalty to 10%.

How do Roth conversions help with tax-efficient withdrawal planning?

Converting traditional IRA funds to a Roth IRA before age 73 shrinks the balance subject to future mandatory distributions, reducing both your RMD amounts and potential Medicare surcharges; early Roth conversions done during low-income years lock in lower tax rates before Social Security and RMDs stack together.