US equities opened lower on Friday after July’s inflation report landed largely as forecast, keeping hopes alive for a September rate cut while highlighting the drag from tariffs. At the bell, the Dow fell about 46 points, the S&P 500 slipped ~0.2%, and the Nasdaq dropped ~0.34%.

The data: inflation and spending

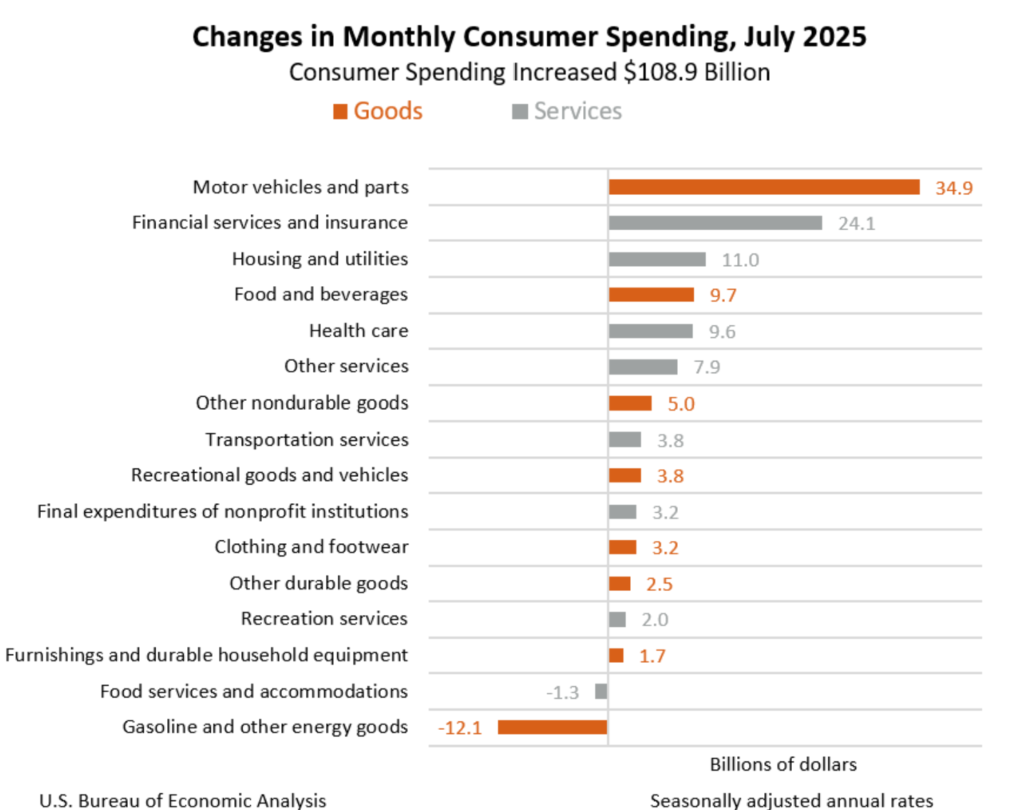

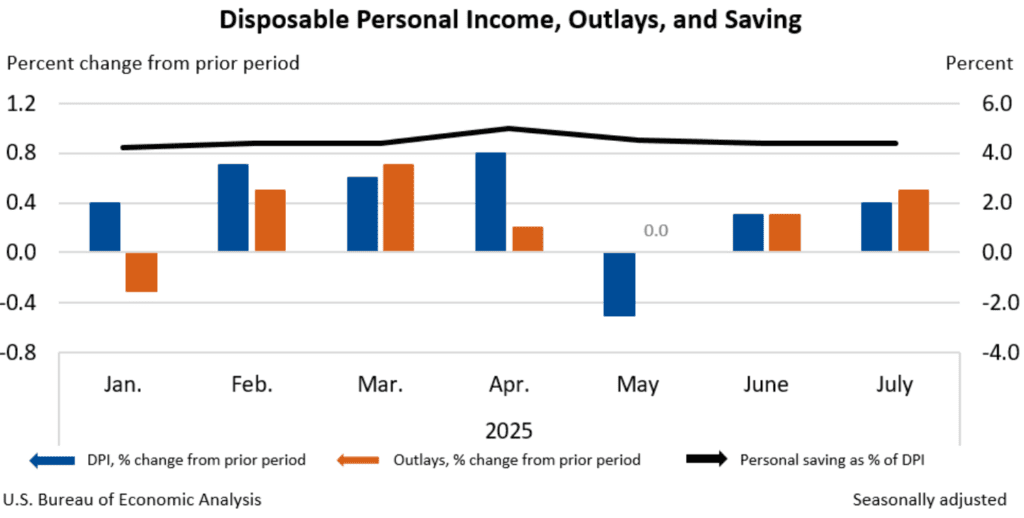

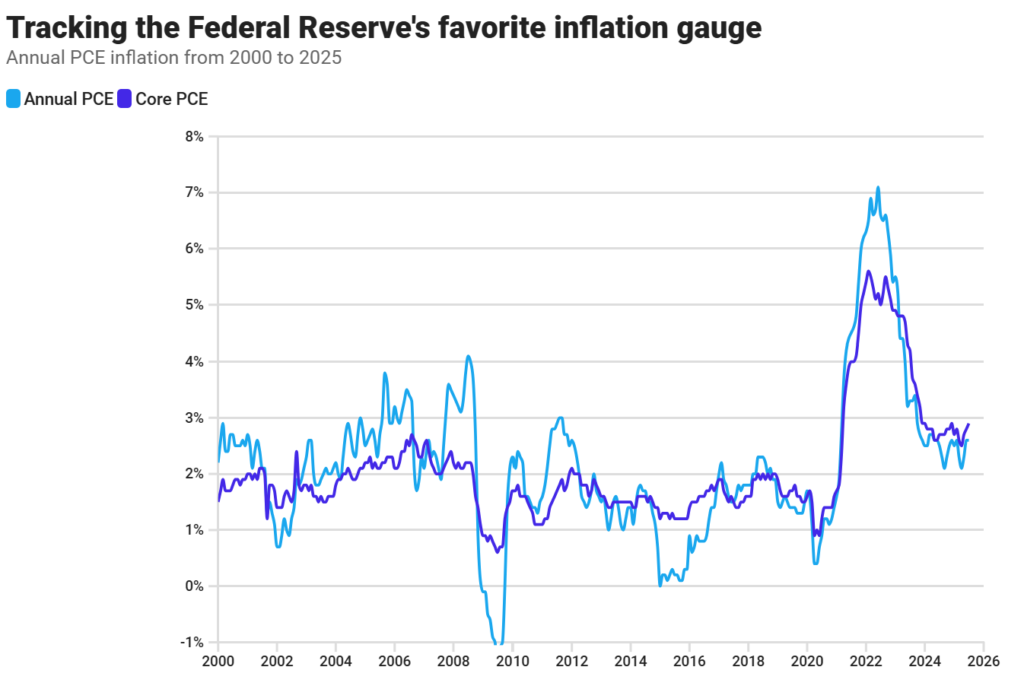

The PCE price index—the Fed’s preferred gauge—rose 0.2% month over month and 2.6% year over year in July, unchanged from June. Core PCE (excluding food and energy) increased 0.3% m/m and 2.9% y/y, the highest since February. Meanwhile, consumer spending rose 0.5% with auto purchases contributing more than one-third of the gain as buyers moved ahead of tariff-related price increases. Personal income rose 0.4%; the saving rate held at 4.4%.

Headline PCE: +0.2% m/m; +2.6% y/y (unchanged from June)

Core PCE: +0.3% m/m; +2.9% y/y (highest since February)

Consumer spending: +0.5% m/m, with autos a big driver

Personal income: +0.4% m/m

Why markets eased

Even with headline inflation steady, the uptick in core PCE to 2.9% reinforces the “sticky” component of price pressures. At the same time, tariff effects are now more visible in goods prices, a backdrop that tempered the otherwise supportive narrative for a September cut and weighed on early trading.

What’s happening under the hood

Tariffs & prices. Multiple reports note tariffs are showing up in the data. Import prices for consumer goods rebounded in July, consistent with inflation pressure from tariffs, while today’s PCE shows services prices still running hot.

Consumers still spending — especially on cars. July outlays rose 0.5% and auto buying was a big chunk as households tried to get ahead of tariff-related price increases.

Trade turns into a growth headwind. The goods trade deficit widened sharply in July to $103.6B as imports jumped, a setup that could drag Q3 GDP after trade boosted Q2 growth.

What Does It All Mean for the Fed?

The latest inflation data is welcome news for the Fed, whose top officials have begun to lay the groundwork for lower borrowing costs as early as their next gathering in roughly three weeks’ time.

Last week, Jerome H. Powell, the chair of the central bank, sent his strongest signal yet that the Fed is preparing to cut interest rates again after a long pause.

Two members of the Fed’s Board of Governors, both of whom were nominated by Mr. Trump, were ready to restart interest rate cuts at the July meeting, citing less concern about inflation and greater worries about the labor market.

“The Fed opened the door to rate cuts, but the size of that opening is going to depend on whether labor-market weakness continues to look like a bigger risk than rising inflation,” said Ellen Zentner, chief economic strategist at Morgan Stanley Wealth Management. “Today’s in-line PCE Price Index will keep the focus on the jobs market. For now, the odds still favor a September cut.”

Waller’s message (key because he could chair Fed next)

Fed Governor Christopher Waller doubled down on a September cut and said he’d back more easing over the next 3–6 months — and could consider a bigger move if the labor market weakens further:

- “Let’s get on with it.” — Waller, in a Miami speech urging the Fed to start cutting in September.

- He supports 25 bps in September and sees additional cuts in coming months, but left the door open to a larger move if jobs data deteriorate.

Translation: The Fed is leaning toward easing to cushion a softer job market, but a sticky 2.9% core PCE and tariff-related price pressure could limit the pace of cuts.

What’s next

- August employment report (next week): A softer print or sizeable downward revisions could shift the debate from 25 bps to the possibility of 50 bps in September.

- Tariff pass-through: Watch the goods-price components in coming PCE/CPI releases for sustained pressure beyond the initial “front-run” surge in autos.

- Growth mix: July’s wider goods gap suggests trade may subtract from Q3 GDP, reversing Q2’s boost.

In conclusion, the Fed is poised to start easing, but not to floor it. Tariffs are quietly hardening the inflation floor just as growth shows soft spots, leaving policymakers to cut while guarding against rekindled price pressure. For markets, that means a data-dependent drift rather than a decisive pivot: the next jobs report will decide whether September is a plain quarter-point trim or the opening move in something bigger. Until then, expect choppy trading as investors weigh a gentler policy path against the risk that tariffs keep core inflation sticky.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related: Nvidia Q2 2026 Earnings Preview and Prediction: What to expect

Why Warren Buffett and Hedge Funds Are Betting on UnitedHealth Stock (UNH)