TL;DR:

- Relying on generic portfolio templates can lead to underperformance and higher taxes that do not suit individual circumstances.

- Effective customization begins with clear, specific financial goals, an honest assessment of risk tolerance, and understanding personal constraints before building a tailored investment plan.

You open your brokerage account, scan a generic “balanced portfolio” template someone shared online, and follow it to the letter. Six months later, your returns are underwhelming, your tax bill is higher than expected, and the allocation still ignores the fact that you’re sitting on company stock or planning to buy a house in three years. That’s the quiet cost of a one-size-fits-all investment model. The good news is that customizing your investment approach isn’t reserved for wealthy clients with private wealth managers. With the right preparation, tools, and ongoing discipline, you can build a strategy that genuinely reflects your goals, constraints, and life stage.

Table of Contents

- What you need before customizing your investment approach

- Step-by-step: How to design your customized investment strategy

- Tools and strategies for customizing investments

- Verifying, adjusting, and troubleshooting your customized approach

- What most get wrong about customizing investment strategies

- Get expert help tailoring your investment approach

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Personalized goals first | Start with your unique goals and circumstances for a tailored investment strategy. |

| Effective tools matter | Leverage strategies like direct indexing and tax-loss harvesting for better results. |

| Ongoing review is vital | Adjust your approach regularly to stay on track with your life and market changes. |

| Customization is more than tweaks | True personalization means deep alignment, not just minor adjustments to a template. |

What you need before customizing your investment approach

Now that you see why tailoring your strategy matters, let’s clarify what you need in place before you begin customizing.

Before you touch a single asset allocation, you need to do the less exciting work of self-assessment. That means writing down your specific financial goals in concrete terms. “Save for retirement” is not a goal. “Accumulate $1.8 million in a tax-advantaged account by age 62 to sustain $72,000 in annual withdrawals” is a goal. The specificity matters because every investment decision downstream flows from it. Goals might include retirement income, funding a child’s education, generating passive income, or saving for a home purchase. Each carries a different time horizon and a different tolerance for short-term volatility.

Understanding your risk tolerance goes beyond answering a five-question questionnaire from a brokerage app. Real risk tolerance includes both your financial capacity to absorb losses and your emotional ability to stay the course when markets drop 25%. A 35-year-old tech employee with high income and no dependents has a very different risk profile from a 50-year-old small business owner whose wealth is concentrated in illiquid business equity. Work through real scenarios: if your portfolio dropped 30% in a single year, would you hold, rebalance, or panic-sell? Your honest answer shapes everything.

Here are the key pieces of information to gather before you build your strategy:

- Current net worth and asset inventory: Real estate, retirement accounts, taxable brokerage accounts, stock options, and any debt obligations

- Income stability and liquidity needs: How much cash flow you need readily accessible and whether your income is variable or salaried

- Tax circumstances: Your marginal federal and state tax bracket, whether you have capital gains exposure, and whether tax-loss harvesting is relevant to your situation

- Ethical or ESG preferences: Some investors want to exclude specific industries or favor companies with strong environmental records

- Investment time horizon: Short-term (under 3 years), medium-term (3 to 10 years), or long-term (10-plus years) goals often require entirely different asset classes

Research confirms that portfolio customization involves real trade-offs, including estimation error in optimized approaches where out-of-sample performance gains can be offset by parameter uncertainty and turnover costs. In plain terms, over-engineering a portfolio without solid data inputs can actually hurt results rather than help them.

| Preparation element | Why it matters | Common mistake |

|---|---|---|

| Written financial goals | Anchors every allocation decision | Too vague or missing entirely |

| Risk tolerance assessment | Prevents panic-driven decisions | Overestimating risk appetite |

| Tax situation review | Unlocks tax-efficient structuring | Ignoring bracket and gain exposure |

| Liquidity requirements | Protects short-term cash needs | Locking up emergency funds |

| Ethical preferences | Aligns values with portfolio | Assumed, not explicitly stated |

Pro Tip: Before you schedule any advisory meetings, spend 30 minutes writing down your three most important financial milestones and the date by which you want to reach each one. That document becomes the north star for every customization decision you make.

A useful starting point for thinking through the mechanics of building an investment portfolio is to understand which asset classes serve which types of goals, then layer your personal constraints on top.

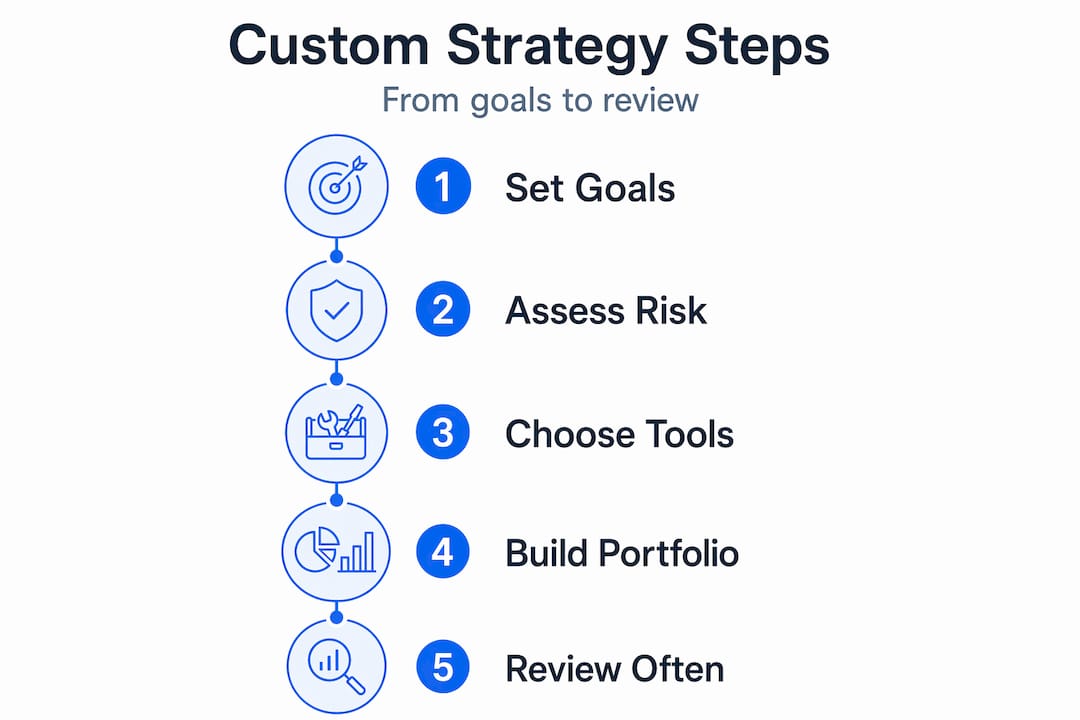

Step-by-step: How to design your customized investment strategy

With your information and requirements ready, you’re set to build your custom strategy.

The first question most investors face is whether to adapt an existing model portfolio or build from scratch. Model portfolios (say, a classic 60/40 stock and bond allocation) are a useful baseline. But they don’t account for concentrated stock positions, employer match mechanics, or the fact that you’re in a high tax bracket and in peak earning years. A truly customized solution treats the model as a starting point, not the answer.

Here is a sequenced process to design your strategy:

- Define your target allocation mix. Decide your broad split between equities, fixed income, real assets, and cash equivalents. Base this on your time horizon and risk profile, not market sentiment.

- Integrate constraints. Layer in your liquidity needs, tax situation, ESG filters, and any concentrated positions you need to manage or unwind gradually.

- Select specific assets. Within each allocation bucket, choose index funds, ETFs, individual securities, or alternative assets that serve each goal. Match the asset’s volatility profile to the goal’s time horizon.

- Choose your implementation method. Decide between a DIY approach through a self-directed brokerage, a fee-only financial advisor, or a robo-advisor that handles rebalancing automatically.

- Document your investment policy statement (IPS). Write down your target allocations, acceptable ranges (called drift bands), and the conditions under which you will rebalance. An IPS forces discipline when markets get emotional.

- Execute in phases if needed. If you’re deploying a large lump sum, consider dollar-cost averaging over several months to reduce the risk of poor timing. For long-term goals, staying invested almost always beats waiting for the “right” moment.

As portfolio customization research shows, even well-designed optimized approaches carry estimation error, which is why documenting your logic and keeping your inputs grounded in your actual situation matters more than chasing a theoretically perfect allocation. For a broader view of what’s working in current markets, reviewing investing strategies in 2025 offers useful context on how macro factors interact with individual portfolio decisions.

| Approach | How it works | Best for |

|---|---|---|

| Static customization | Set allocation once, rebalance on a schedule | Stable life circumstances, low complexity |

| Dynamic customization | Adjust allocation as goals, life events, or markets shift | Complex situations, high-net-worth investors |

| Robo-advisor guided | Algorithm manages allocation within set parameters | Cost-conscious investors who want automation |

| Advisor-led custom | Advisor builds and adjusts based on full financial picture | High complexity or significant tax optimization |

If you are developing an investment strategy for the first time, starting with a documented plan and a simple, low-cost implementation keeps you from over-complicating the early stages.

Pro Tip: Set a calendar reminder every six months to review your portfolio against your IPS. Life changes faster than most investors realize, and even a single major event like a new job, an inheritance, or a change in tax filing status can shift your optimal allocation significantly.

Tools and strategies for customizing investments

Once you have a blueprint, you need the right tools and methods to bring your personalized strategy to life.

The most powerful customization technique available to taxable investors today is direct indexing. Instead of buying a fund that tracks an index, direct indexing means purchasing the individual securities that make up the index directly in your account. This creates a critical advantage: you can harvest tax losses on individual positions that decline even when the broader index is up.

“Direct indexing is a well-known customization technique for taxable investors because it enables tax-loss harvesting at the individual security level, producing ‘tax alpha.’” — Key Private Bank introduction to direct indexing

Tax alpha from direct indexing can add meaningful compounding power over time. Some estimates suggest this approach can generate meaningful annual after-tax outperformance compared to holding a standard ETF. Direct indexing also makes it easier to exclude specific stocks for ethical reasons, manage existing concentrated positions without triggering a taxable event all at once, and align with ESG screens.

Here are the primary tools and techniques worth understanding:

- Direct indexing platforms: Several brokerage and wealth management platforms now offer direct indexing with minimums starting around $100,000. The technology has become more accessible as fractional shares and commission-free trading have lowered the barrier to entry.

- Tax-loss harvesting: This involves selling positions that have declined in value to realize a capital loss, then immediately reinvesting the proceeds in a similar (but not identical) asset to maintain market exposure. You can learn more about the mechanics through tax-loss harvesting explained, which covers wash-sale rules and when the strategy makes the most sense.

- ESG overlays: You can apply environmental, social, and governance screens to any portfolio, excluding sectors like fossil fuels, tobacco, or weapons manufacturing, or weighting toward companies with high sustainability scores.

- Factor-based investing: This approach tilts your portfolio toward historically rewarded risk factors like value (stocks trading below intrinsic value), quality (high profitability and low debt), or momentum (recent price strength). Factor exposure can be layered on top of a core allocation.

- Asset location optimization: Placing tax-inefficient assets (like bonds or REITs) in tax-advantaged accounts and tax-efficient assets (like index ETFs) in taxable accounts can quietly boost after-tax returns without changing your allocation at all. This is one of the simplest forms of tax-efficient investing available to any investor.

The combination of these tools is where real customization compounds. A portfolio that uses direct indexing, applies an ESG screen, locates assets intelligently across account types, and harvests losses systematically can significantly outperform a generic fund mix on an after-tax basis, even if pre-tax returns are similar.

Verifying, adjusting, and troubleshooting your customized approach

Customizing isn’t a one-and-done process. Here’s how you ensure your approach keeps working in your favor.

The most common failure mode for customized portfolios is what you might call “set-and-forget drift.” An investor builds a thoughtful strategy, implements it carefully, then does nothing for two years. By then, a bull run in equities has pushed the portfolio from 60% stocks to 78% stocks, the risk profile no longer matches the original intent, and the investor doesn’t realize it until a market correction hits harder than expected.

Here is a practical framework for ongoing portfolio maintenance:

- Quarterly performance review. Compare your actual returns against a relevant benchmark and check whether each goal’s specific account is on track. Don’t just look at total returns; evaluate whether your risk-adjusted progress matches your plan.

- Semi-annual allocation check. Review whether your actual allocation has drifted more than 5 percentage points from your target in any major bucket. If it has, execute a rebalance.

- Annual strategy review. Reassess your goals, income situation, time horizons, and tax circumstances. Ask whether the original strategy still fits, or whether a life event (marriage, new child, job change, approaching retirement) requires a meaningful shift.

- Event-driven adjustments. Some changes shouldn’t wait for a scheduled review. A large inheritance, a new mortgage, the exercise of stock options, or a significant income change all warrant an immediate reassessment of your allocation and tax planning.

- Troubleshoot underperformance carefully. If your portfolio is lagging, distinguish between strategy drift, market timing errors, excessive costs, and tax drag. Each has a different fix.

“Customization” that is only cosmetic may underperform approaches that continually re-align the plan to life events, risk tolerance shifts, and goal-specific cash-flow needs.

Pro Tip: Consider bringing in a fee-only financial planner for your annual review, even if you manage the portfolio yourself the rest of the year. An outside perspective catches blind spots, particularly around tax optimization and sequence-of-returns risk as you approach a major goal.

For ongoing portfolio construction decisions, tracking both financial and personal milestones in the same document keeps your strategy grounded in what actually matters to you.

What most get wrong about customizing investment strategies

Here’s a perspective most financial content skips: many investors believe they’ve customized their portfolio when they’ve actually just added a layer of cosmetic complexity. They tilted slightly toward tech stocks because they work in the industry. They excluded one controversial sector. They moved one fund from taxable to a retirement account. And then they called it done.

That’s not customization. That’s decoration.

Real customization means your portfolio is structurally different from a generic model in ways that directly serve your specific circumstances. It means the asset location reflects your tax situation. The allocation reflects your true liquidity needs and your realistic time horizon. The rebalancing schedule reflects how your income and risk tolerance shift over time. And the whole system gets revisited as your life changes, not just when markets make the news.

The research backs this up. Cosmetic customization consistently underperforms strategies that genuinely realign with life events and evolving risk tolerance. The gap between surface-level tweaks and authentic personalization can compound over years into a meaningful difference in outcomes.

The fix is to treat your investment strategy as a living document, not a configuration you set once. Track personal milestones the same way you track financial ones. Know when your risk tolerance changes, not just when your account balance does. Look at how investors adapt in challenging markets for practical examples of genuine strategic pivots versus reactive noise. The investors who come out ahead aren’t necessarily the ones with the most sophisticated allocation models. They’re the ones who stay honest about their situation and adjust with purpose.

Get expert help tailoring your investment approach

Navigating the overlap between tax strategy, allocation theory, goal-based planning, and life events is genuinely complex. You don’t have to figure it out alone. Finblog offers educational resources, tools, and expert content designed specifically for investors who want to move beyond generic templates and build strategies that match their real financial picture. Whether you’re exploring direct indexing for the first time, trying to understand how to structure a tax-efficient withdrawal plan, or simply want to pressure-test your current allocation, the right information makes the process faster and less costly in the long run. Explore the resources, ask better questions, and take deliberate next steps toward a portfolio that truly fits your life.

Frequently asked questions

What is the most effective way to start customizing my investment portfolio?

Begin by clearly defining your goals, risk tolerance, and key constraints before selecting tools and strategies. As research on portfolio construction trade-offs confirms, building your strategy on precise inputs reduces estimation error and improves real-world outcomes.

How does direct indexing benefit taxable investors?

Direct indexing enables tax-loss harvesting at the individual security level, which can generate meaningful annualized tax alpha compared to holding a standard fund. According to a direct indexing primer, this approach also allows investors to apply custom ESG screens and manage concentrated stock positions more efficiently.

Is it necessary to update my customized investment approach?

Yes. Cosmetic-only customization that doesn’t adapt to life events, goal shifts, or changes in risk tolerance consistently underperforms strategies that realign continuously with evolving circumstances.

How does a customized strategy compare to a model portfolio?

A customized strategy adjusts for your specific tax bracket, liquidity needs, and goal timeline, while a model portfolio is a standardized starting point. Research shows that optimized custom approaches outperform generic models when inputs are accurate, though they require greater discipline to maintain correctly.