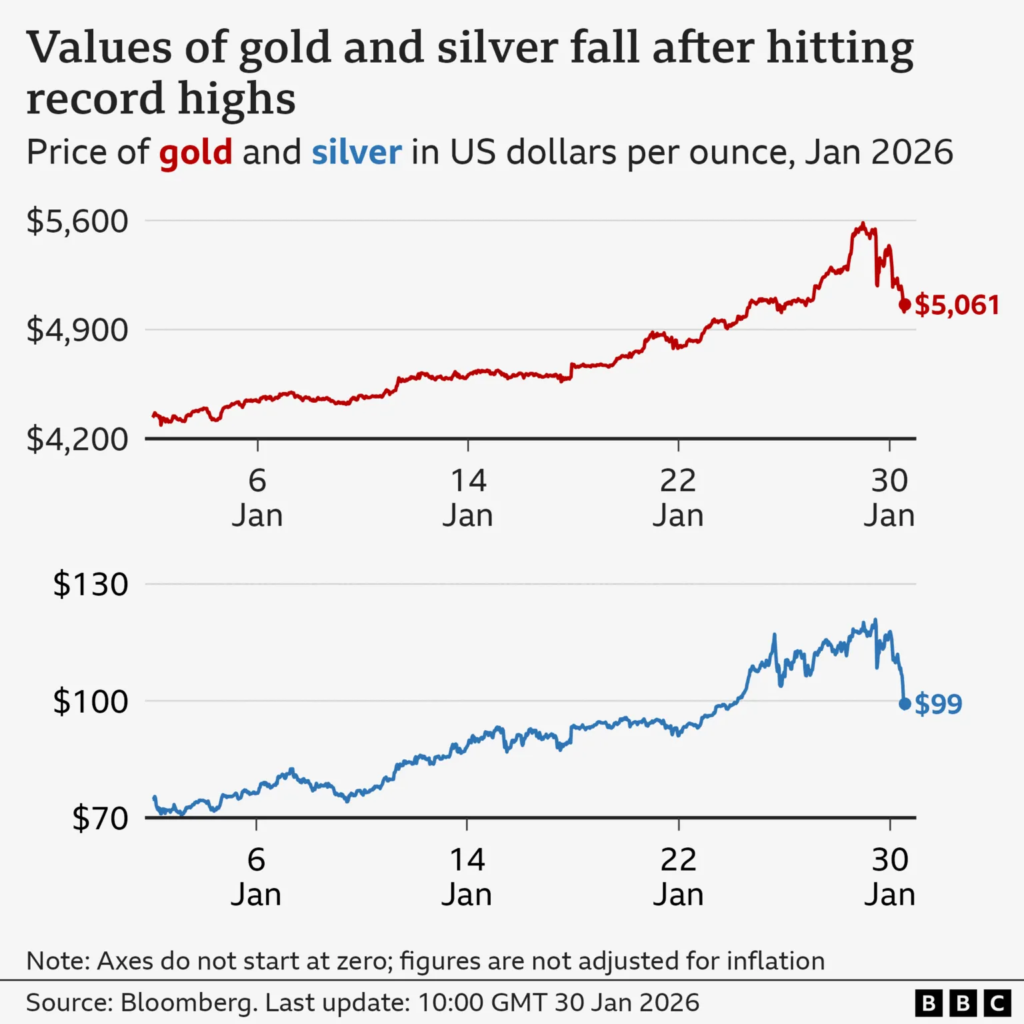

Gold and silver did not just fall last week. They collapsed in a way markets have not seen since 1980.

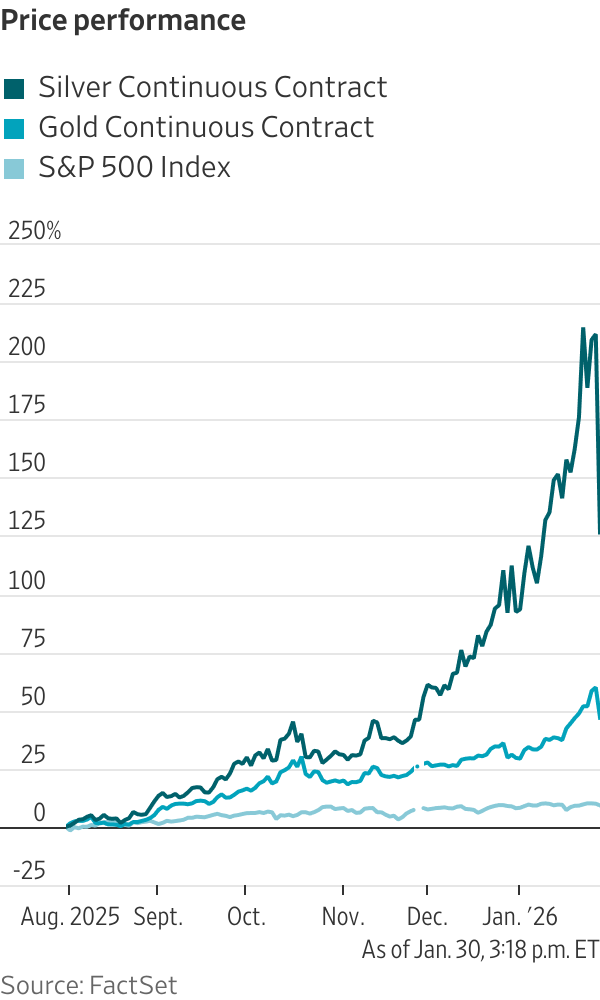

Silver plunged as much as 30% in a single day, its sharpest drop since the Hunt brothers’ collapse more than four decades ago. Gold futures fell roughly 11–12%, marking one of the largest one-day dollar losses on record. In total, more than $7 trillion was wiped off the combined value of precious metals markets.

For assets many investors treat as “safe,” the speed of the reversal was shocking. But the selloff did not come out of nowhere. It was the final act of a rally that had become overcrowded, leveraged, and emotionally charged.

To understand why gold, silver and platinum surged so violently, and why they crashed just as fast, you have to understand three powerful narratives that collided at once.

The scale of the selloff, by the numbers

The declines were historic:

- Gold futures fell 10–12% in one day, dropping from above $5,500 per ounce to around $4,700–4,900, the largest one day dollar decline on record and the steepest percentage fall since January 1980.

- Silver collapsed 27–32%, falling from more than $114 per ounce to near $78–83, its worst one-day crash since 1980, when the Hunt brothers’ silver squeeze unravelled.

- Platinum plunged alongside, caught in the same liquidation wave.

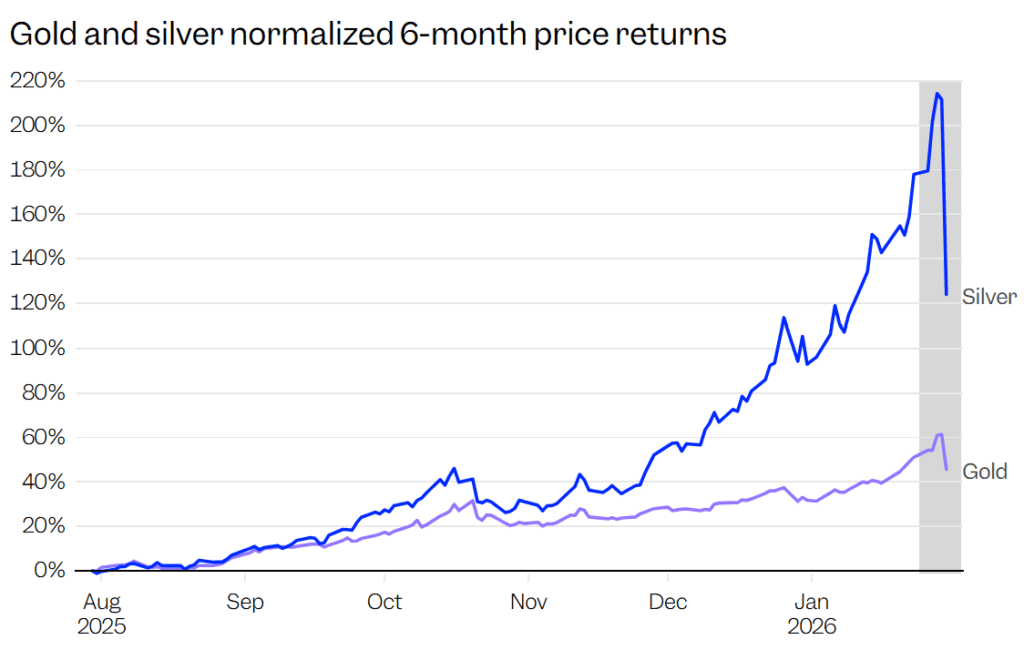

- Despite the crash, gold remains up roughly 60–80% year over year, while silver is still up around 20–25% for 2026, showing how extreme the prior rally had been.

Mining stocks were hit hard, helping drag the S&P 500 down about 0.4%, the Dow Jones down roughly 180 points, and the Nasdaq down close to 1%.

As several analysts noted, liquidity in metals markets is thin. When prices rise vertically, it does not take much selling to send them straight back down. This rally had all the hallmarks of a crowded trade: heavy ETF inflows, leveraged positioning, and fast money chasing momentum rather than fundamentals.

More about: Gold Crash! Down $3.4 Trillion as Silver Sinks 12% from New Record Highs

Why gold and silver surged in the first place

1. Gold as an alternative to the dollar

One explanation for the surge was fear about the future of the US dollar.

For years, countries worried about sanctions have shifted reserves away from dollars and toward gold. That trend helped support gold prices earlier on.

But here is the key detail many missed.

According to the World Gold Council, central banks actually slowed their gold buying in 2025 as prices climbed. The marginal buyer was no longer governments. It was private investors, largely through ETFs.

If gold were rising mainly as a dollar alternative, we would expect:

- A sharply falling dollar

- Rising US Treasury yields as capital exits America

- Strong demand for haven currencies

Instead, something odd happened.

The US dollar weakened, but US 10-year Treasury yields fell slightly, while yields in Japan, Germany, France and the UK rose. That is not a classic “capital flight” signal.

Gold was moving independently. That disconnect hinted that speculation had overtaken its original purpose.

2. Geopolitics and tariffs

Trump’s tariff threats, trade disputes with Europe and China, wars in Ukraine and Gaza, and even rhetoric around Greenland all contributed to a global risk off environment.

As Emma Wall of Hargreaves Lansdown put it, gold was “doing what it does best when the world feels messy.”

3. The debasement trade and inflation fear

The second and more emotional driver was inflation anxiety.

After the inflation shock of the early 2020s, many investors became convinced another wave was inevitable. Large deficits, trade tariffs, political pressure on central banks and a weaker dollar all fed the belief that money would be debased again.

Gold and silver became the center of what Wall Street calls the debasement trade.

Then came the trigger.

Reports emerged that President Donald Trump would nominate Kevin Warsh as the next Federal Reserve chair.

Warsh is widely seen as more hawkish than other candidates, particularly Kevin Hassett. Once the nomination was confirmed, markets reacted instantly:

- The US dollar posted its strongest day in months

- Gold and silver collapsed

- Long-term Treasury yields rose

At first glance, this made sense. A less dovish Fed chair reduces fears of aggressive rate cuts and runaway inflation.

But here is the problem with the debasement story. If investors truly feared inflation, that fear should show up clearly in bond markets. It did not.

Long-term inflation expectations actually fell this year. The five-year, five-year forward breakeven rate is lower than it was a year ago.

So why did inflation fear appear almost exclusively in precious metals, but not in bonds, currencies or equities? That inconsistency suggests gold and silver were amplifying fear rather than accurately pricing it.

4. Central banks and large buyers

Central banks continued buying gold as an alternative reserve asset, especially after seeing Russia’s dollar assets frozen.

Demand was also fueled by:

- China, both retail and institutional

- Western investors via ETFs

- New entrants such as Tether, which reportedly accumulated gold reserves rivaling those of small nations

BullionVault reported January 2026 as its largest month ever for new customers, even bigger than the pandemic or the Lehman collapse.

5. A global growth boom, not collapse

The third explanation flips everything on its head.

What if gold and silver were rising not because investors feared economic collapse, but because they expected strong global growth?

History supports this idea.

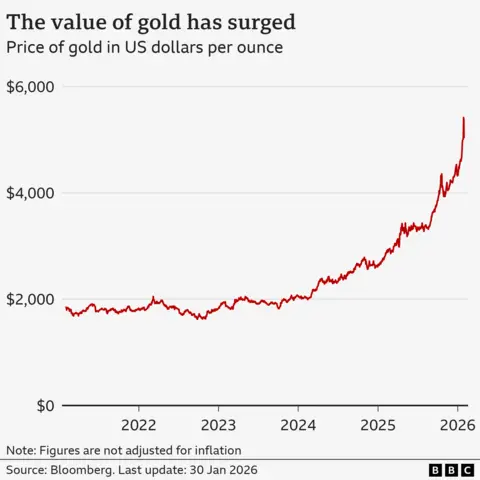

Between 2001 and 2007, before the financial crisis, commodities surged alongside global expansion. Copper soared. Silver climbed. Gold rose steadily from $273 to over $600 an ounce.

We saw echoes of that pattern recently:

- Small stocks outperforming big stocks

- Value stocks beating growth

- Copper jumping more than 20% since November on data-center demand

- Silver and gold riding the same momentum wave

There are reasons investors might believe in global growth. Japan has promised tax cuts. Germany is boosting defense spending. China stimulus hopes remain alive. Even geopolitical tensions briefly eased.

But again, the scale does not fit.

Global growth optimism does not justify silver tripling in a year. It does not explain why gold detached from bonds and currencies. And it certainly does not justify a one-day crash of this magnitude.

More about: Three Reasons Gold Hit Record Highs — and One Key Reason It’s Falling Now

Why crash was so violent

By late January, precious metals had become one of the most crowded trades in global markets.

Silver was especially vulnerable. Heavy leverage meant that once prices began to fall, margin calls forced selling, pushing prices lower and triggering a self-reinforcing liquidation cycle. Adrian Ash of BullionVault said he had “never seen anything quite like this” in two decades of trading.

Liquidity also disappeared at the top. Above roughly $5,500 for gold and $120 for silver, there were simply not enough buyers. When prices slipped, the absence of bid support turned an ordinary pullback into a free fall. Even copper fell more than 4%, signaling institutional risk reduction rather than retail panic.

Month-end profit taking added fuel. After gains ranging from 60% in gold to nearly 200% in silver over the past year, many funds locked in profits. Kevin Warsh’s nomination as Fed chair was the catalyst, but the unwind was already primed.

Why platinum and even copper fell too

This wasn’t about individual metals anymore. It was about risk reduction.

When markets flip from confidence to caution, investors sell entire asset groups, not just one contract or one commodity. Precious metals moved together. Base metals like copper fell as well, even though retail investors barely touch them.

That’s a sign this was not a small investor panic. It was institutional repositioning.

The key lesson investors learned

Gold did not fail. Silver did not “break.”

What failed was the assumption that safe assets cannot move violently.

The rally combined three partially true stories into one overcrowded trade. When the narrative cracked, prices collapsed under their own weight.

Even after the crash:

- Gold remains up more than 14% this year

- Silver is still up over 20% year to date

The lesson is not that gold is useless. The lesson is that timing and positioning matter, even in assets people believe are immune to chaos.

Gold still has a role in uncertain times. But Friday proved that arriving late to a rally that has already outrun reality can be just as dangerous as chasing meme stocks.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.