Debt has always been a key driver of economic growth, but when it grows too large, it can create major problems for financial markets. The long-term debt cycle theory, popularized by Ray Dalio, explains how economies move through phases of borrowing, deleveraging, and recovery.

Understanding where we stand in this cycle today can give us insight into what comes next.

Let’s explore the dynamics of debt cycles, the current state of sovereign and corporate debt, and what potential deleveraging could mean for global markets.

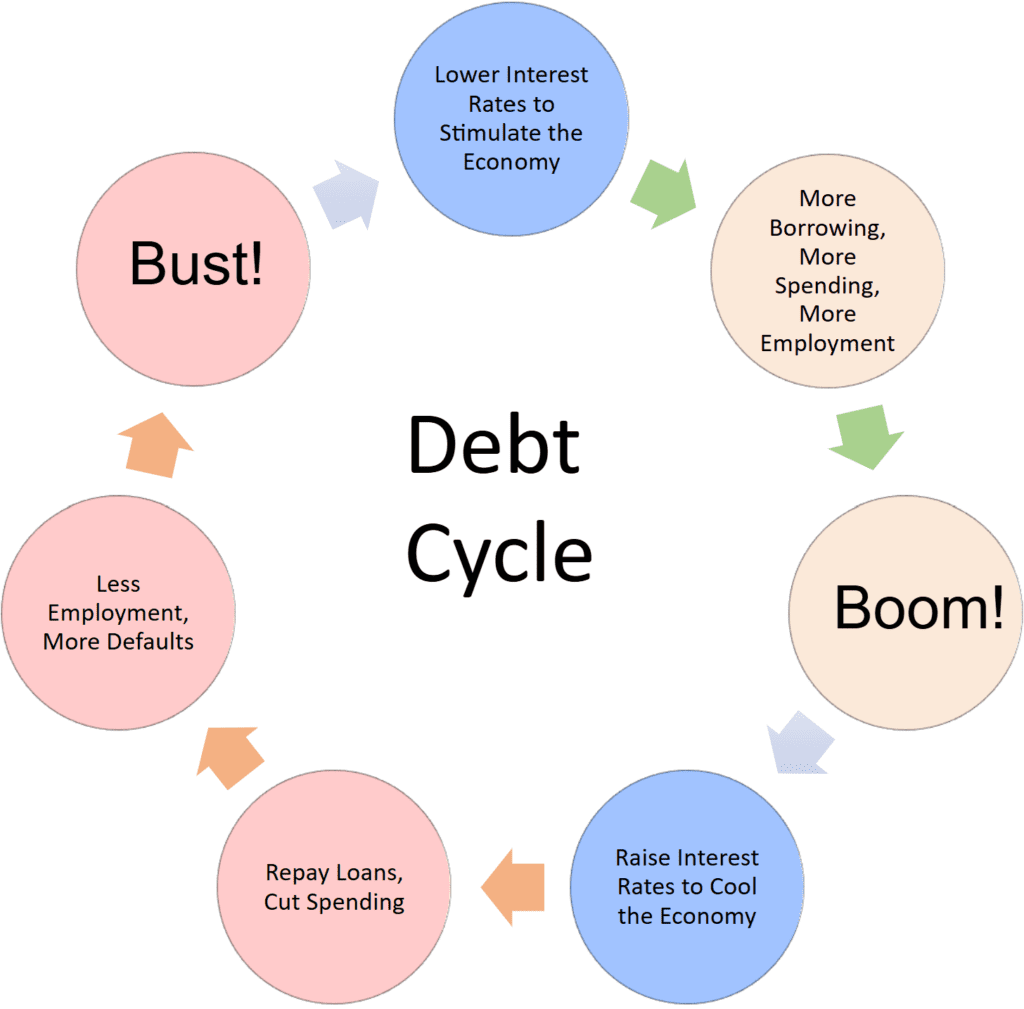

What Are Debt Cycles?

Debt cycles occur in two forms. Short-term debt cycles (5-10 years) are tied to the normal business cycle, where economies expand, credit rises, interest rates increase, and corrections reset the system.

Long-term debt cycles (50-75 years) are more significant.

Over decades, debt builds to unsustainable levels, eventually leading to deleveraging, defaults, and economic restructuring. The last major deleveraging happened during the 1930s Great Depression and, more recently, the 2008 Global Financial Crisis.

Today, many experts argue that we are approaching the late stage of the current long-term debt cycle.

Sovereign Debt: The Rising Burden

Governments worldwide have accumulated record levels of debt.

In the United States, national debt has surpassed $34 trillion, equal to over 120% of GDP. Similarly, in the Eurozone, countries like Italy and Greece carry debt-to-GDP ratios exceeding 140% and 170%, respectively.

Emerging markets are particularly vulnerable, as rising borrowing costs and a strong U.S. dollar have increased the pressure on external debt. High levels of sovereign debt can be sustainable while interest rates remain low and growth continues.

However, if inflation persists and central banks keep rates elevated, governments may face higher debt servicing costs.

This scenario could force policymakers to choose between austerity, restructuring, or inflationary measures to reduce real debt burdens. For investors, this environment raises risks for government bonds and currencies while increasing opportunities in inflation-hedging assets like gold and commodities.

Corporate Debt: A Ticking Clock?

Corporate borrowing has surged over the past decade due to low interest rates and easy credit conditions. Global corporate debt exceeded $90 trillion in 2023.

However, rising interest rates are now creating challenges for businesses, particularly those with weak balance sheets.

The share of “zombie companies”-businesses unable to cover their interest payments-is rising, especially in sectors like real estate and retail. If rates stay elevated, defaults could increase, particularly in leveraged industries. Investors should focus on companies with strong cash flows and avoid those overly reliant on cheap financing. The high-yield bond market, in particular, could experience increasing volatility as risks grow.

Deleveraging: How It Could Play Out

When debt becomes unsustainable, economies enter a period of deleveraging, where debt is reduced through defaults, inflation, or productivity growth. Deleveraging occurs in four key ways:

- Defaults and restructuring force borrowers to renegotiate or fail to repay debts.

- Austerity measures reduce spending but slow economic growth.

- Inflation erodes the real value of debt but risks runaway price increases.

- Productivity growth allows economies to outgrow their debt burdens, though this is the hardest to achieve.

It is expected a combination of these outcomes over the next decade.

Central banks may tolerate higher inflation to ease debt burdens, while defaults could rise in sectors with excessive leverage. For investors, this environment reinforces the importance of quality equities, inflation-resistant assets like commodities, and short-duration bonds.

Where Do We Stand Today?

At this point in the long-term debt cycle, several themes stand out.

Sovereign debt levels are rising, particularly in developed economies. Corporate vulnerabilities are increasing, with rising defaults a likely scenario in highly indebted sectors.

Central banks face a delicate balancing act between controlling inflation and maintaining financial stability. For investors, this late-stage environment demands caution.

Defensive strategies, diversification, and focus on quality assets can help navigate potential volatility.

Visions of Tomorrow

A few scenarios stand out as the debt cycle progresses:

- Central banks may tolerate higher inflation to reduce real debt levels.

- Debt restructuring could occur in economies and companies with unsustainable burdens.

- Global growth may slow as high debt levels weigh on economic expansion.

- Emerging markets with external debt may face heightened risks due to rising global borrowing costs.

Bonus Lesson to Remember

Debt is a double-edged sword. It fuels economic growth, but when it becomes excessive, it creates systemic risks.

At this stage in the long-term debt cycle, understanding risks and opportunities is critical. By focusing on quality assets, staying diversified, and preparing for volatility, investors can position themselves to weather the challenges ahead.

History shows that those who adapt during uncertain times emerge stronger in the end.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Source: Macro Strategist

Related:

Institutional Investors Bet $1B on These 4 Stocks—Should You?

Nasdaq 100 Crashes After Dimon & Buffett Sell-Off: What Did They Know?

CrowdStrike: Deep Dive into Company Fundamentals & Market Forecast

How Google tracks Android device users before they’ve even opened an app

Crypto Capital Of The World? Trump’s Bitcoin Reserve Plan Sparks Debate

Next S&P 500 Inclusion Coming: Here are Potential Stock Additions

Congress Trading: A Spotlight on Ecolab (ECL)

Trump’s Bitcoin Reserve: A Game-Changer or a Market Shock?

TSMC and Intel Investments at Risk as Trump Targets $52B CHIPS Act

What Analysts Think of Broadcom Stock Ahead of Q1 Earnings?

What Analysts Think of BigBear.ai Stock Ahead of Earnings?

The 10 Stocks Hedge Funds Love—and Hate—the Most

Why Is the Stock Market Still Panicking after Nvidia Strong Earnings…?