TL;DR:

- Many financial professionals do not operate under a fiduciary standard, risking investors’ money.

- Verifying a fiduciary’s status requires direct written questions, reviewing disclosures, and confirming registration details.

Most people assume any financial advisor they hire is legally required to act in their best interest. That assumption is wrong, and it costs investors real money. Understanding what is a fiduciary, and how fiduciary duty differs from a simple suitability standard, is one of the most practical things you can do before handing anyone control over your financial future. This article breaks down the fiduciary duty definition, explains who qualifies, how the rules have shifted in 2026, and exactly how to verify whether the person managing your money is actually working for you.

Table of Contents

- Key takeaways

- What is a fiduciary and what do they owe you

- Types of fiduciaries and how they show up in finance

- The regulatory context in 2026: what changed and why it matters

- How to verify fiduciary status before you hire anyone

- Fiduciary oversight goes deeper than picking investments

- My honest take on fiduciary trust

- Explore fiduciary standards and planning tools at Finblog

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Fiduciary defined | A fiduciary is legally required to act in your best interest, not their own. |

| Not all advisors qualify | Many financial professionals operate under a weaker suitability standard, not a fiduciary one. |

| Verify before you trust | Always ask directly about fiduciary status and review Form ADV disclosures before hiring. |

| Regulation changed in 2026 | The DOL reverted to the five-part ERISA test after the 2024 Retirement Security Rule was vacated. |

| Process matters too | Fiduciary duties cover documentation, conflict management, and oversight, not just investment picks. |

What is a fiduciary and what do they owe you

A fiduciary is a person or entity that acts on behalf of another and is legally obligated to prioritize that person’s interests above their own. The term comes from the Latin word “fiducia,” meaning trust. In practice, it describes any professional relationship where one party holds authority over another’s money, property, or legal rights.

The fiduciary duty definition covers four core obligations. When you understand them, the label stops being abstract and starts being a real standard you can hold someone to.

- Duty of loyalty. The fiduciary must act solely in your best interest. Personal gain or third-party incentives cannot drive their decisions.

- Duty of care. They must act with diligence, skill, and prudence. Sloppy or uninformed advice is not acceptable under this standard.

- Duty of confidentiality. Information you share stays protected. A fiduciary cannot use your financial details for personal advantage.

- Duty to avoid conflicts of interest. When a conflict exists, it must be disclosed or resolved in your favor. Hiding it is a breach of duty.

Breaching fiduciary duty carries serious legal consequences. A fiduciary who violates their obligations can face civil liability, financial penalties, and in some cases criminal prosecution. That legal accountability is precisely what separates a fiduciary relationship from a casual professional one.

Types of fiduciaries and how they show up in finance

Fiduciary roles appear across law, finance, medicine, and government. In the context of investment management, the ones you are most likely to encounter fall into a few distinct categories.

Understanding fiduciary roles starts with recognizing that not everyone with “advisor” in their title holds this obligation. A Registered Investment Advisor (RIA) registered with the SEC or a state regulator is held to a fiduciary standard. A broker-dealer, by contrast, typically operates under a suitability standard, meaning they only need to recommend products that are “suitable” for you, not necessarily the best option available.

Here is how the most common roles compare:

| Role | Standard | Key obligation |

|---|---|---|

| Registered Investment Advisor (RIA) | Fiduciary | Must act in client’s best interest at all times |

| CFP® professional | Fiduciary | Prioritize client needs and disclose all conflicts |

| Broker-dealer | Suitability (Reg BI) | Recommend suitable products, avoid certain conflicts |

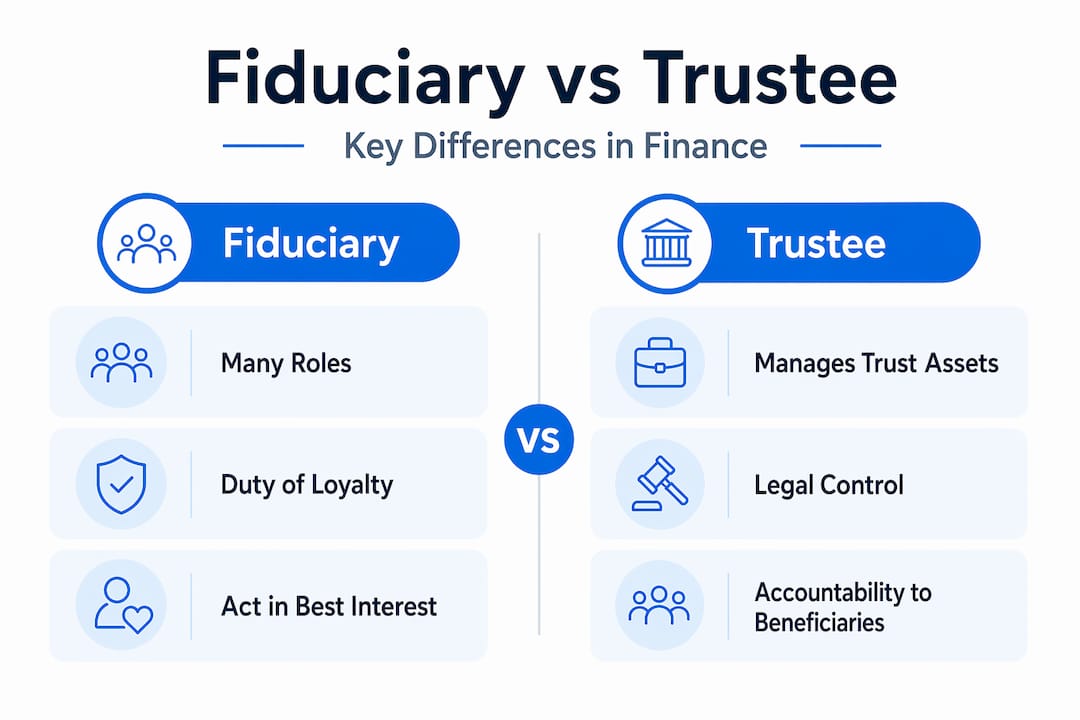

| Trustee | Fiduciary | Manage trust assets solely for beneficiaries |

| Estate executor | Fiduciary | Administer estate in the interest of heirs |

| Power of attorney agent | Fiduciary | Act within stated authority for the principal’s benefit |

The fiduciary vs trustee distinction is worth a closer look. Both are fiduciaries, but a trustee manages assets held in a formal trust structure for named beneficiaries. A financial advisor acting as a fiduciary manages your investment portfolio under an advisory relationship. The legal vehicle differs. The core obligation, putting your interests first, does not.

Pro Tip: When evaluating a financial advisor, ask whether they are registered as an RIA. SEC registration typically carries a stronger fiduciary obligation than registration as a broker-dealer alone.

The regulatory context in 2026: what changed and why it matters

Fiduciary standards in investment management are not static. The rules defining who qualifies as a fiduciary under federal retirement law shifted significantly in 2026, and the change directly affects how retirement investors should think about their advisors.

The Department of Labor’s 2024 Retirement Security Rule had expanded the definition of who counted as an investment advice fiduciary under ERISA, covering more one-time rollover recommendations and other advice scenarios. That rule was struck down by federal courts. As a result, the ERISA five-part test was restored as the standard for determining fiduciary status in retirement advice. Under that older test, a one-time rollover recommendation may not trigger fiduciary status at all, even if it involves a significant transfer of your retirement savings.

What does this mean for you practically? It means fewer retirement advisors are automatically held to a fiduciary standard when giving rollover advice. That gap matters because rollovers are exactly the moment when conflicted advice can cost you the most, when you are moving a large sum and the advisor stands to earn a commission on where it lands.

That said, best interest expectations remain even outside formal fiduciary classifications. The SEC’s Regulation Best Interest (Reg BI) still requires broker-dealers to act in clients’ best interest at the point of a recommendation. Several states have also passed their own fiduciary-level rules for investment advice. And the expectation that advisors document their reasoning and disclose conflicts has not disappeared. Regulation shapes the floor. Your own vigilance determines the ceiling.

Pro Tip: After any rollover recommendation, ask your advisor to put in writing why the recommendation is in your best interest and what fees or compensation they receive as a result. A genuine fiduciary will not hesitate.

How to verify fiduciary status before you hire anyone

Many consumers wrongly assume advisors automatically put clients first. Verification is not a formality. It is the single most important step before entering any financial advisory relationship. Here is a practical process:

- Ask directly, in writing. Request a simple written confirmation of whether they serve as your fiduciary at all times, not just sometimes. Some advisors switch hats depending on the type of product they are selling.

- Request and read Form ADV. Every RIA must file Form ADV with the SEC or state regulators. This document discloses their business practices, compensation structure, and any disciplinary history. It is public. Use it.

- Understand how they get paid. Fee-only fiduciaries charge you directly and do not receive commissions. Fee-based advisors do both. Commission-based advisors earn money when you buy products. Each model creates different incentive structures, and knowing which applies to your advisor tells you a lot about where their loyalty may actually sit.

- Check registrations independently. Use FINRA’s BrokerCheck or the SEC’s Investment Adviser Public Disclosure database to verify registration status and any complaints or enforcement actions.

- Watch for red flags. Be skeptical of advisors who push proprietary products, who are vague about compensation, or who resist putting disclosures in writing.

Compensation structure is a useful signal, but not a guarantee. Proper disclosure and registration must align with any fiduciary claim. An advisor calling themselves a fiduciary while collecting undisclosed commissions is not acting like one, regardless of what they say.

You can also explore the role of financial advisors in building wealth to understand how different advisor types impact your outcomes over time.

Fiduciary oversight goes deeper than picking investments

Here is something most articles miss. Fiduciary responsibilities explained properly are not limited to the moment an investment is selected. They cover the entire ongoing relationship.

Real fiduciary oversight includes:

- Documented rationale. A fiduciary should be able to show you, in writing, why a specific recommendation was made and how it aligned with your goals and risk tolerance.

- Conflict management. Identifying potential conflicts before they affect advice, and disclosing them proactively, is part of the duty of loyalty.

- Ongoing monitoring. Selecting a fund is not a one-time act. A fiduciary is responsible for reviewing whether that recommendation still makes sense as your circumstances and markets change.

- Retirement rollover scrutiny. Rollover decisions require documented fiduciary care that goes well beyond what is typical for standard investment selection, given the scale and irreversibility of these decisions.

Performance reporting is another area where fiduciary oversight reveals its depth. Fiduciary manager portfolios can differ significantly from model returns due to implementation costs, liquidity constraints, and legacy assets. A fiduciary’s job includes monitoring how returns are actually achieved, not just what the headline number says. Comparing returns alone without understanding the process behind them can be actively misleading.

That accountability over time is what makes a fiduciary relationship different from a transactional one. It is not just one good recommendation. It is a sustained commitment to your interests.

My honest take on fiduciary trust

I’ve spent years watching investors get burned not by outright fraud, but by the quiet damage of misaligned incentives. Someone recommends a product, it is technically “suitable,” and nothing illegal happened. But the investor paid higher fees, earned lower returns, and never knew a better option existed.

What I’ve learned is this: the word “fiduciary” is not magic. I’ve seen advisors wear the title and still find ways to serve themselves first through selective disclosure, vague fee structures, and strategically incomplete advice. Conversely, I’ve seen non-fiduciary advisors behave with genuine integrity. The label matters, but fiduciary behavior hinges on relationship transparency, not just legal classification.

My practical advice: treat fiduciary status as a starting filter, not a final answer. Verify it. Document it. Then pay attention to how your advisor communicates over time. Do they explain their reasoning? Do they proactively flag when something changes? Do they bring up conflicts before you ask? Those behaviors reveal more than any title ever will.

Regulatory frameworks will keep shifting, as they already have in 2026. Your best protection is knowing what to ask and refusing to accept vague answers.

— Povilas

Explore fiduciary standards and planning tools at Finblog

Understanding the importance of fiduciaries is only the first step. The decisions that follow, choosing retirement accounts, evaluating advisor relationships, and building a long-term financial plan, require the same level of clarity applied to real numbers and real options.

Finblog covers all of it. You can compare your retirement account choices to see how fiduciary standards apply across different account structures. If you want a step-by-step framework, the retirement planning checklist walks you through every decision point, including how to evaluate the advisor relationships you rely on. For a deeper look at advisor value and how to distinguish genuine fiduciaries from professionals who simply use the term, start with Finblog’s guide to the benefits of financial advisors. The goal is not just to understand fiduciary duty in the abstract. It is to use that understanding to make better decisions about your financial future.

FAQ

What does fiduciary mean in simple terms?

A fiduciary is someone legally required to act in your best interest rather than their own. The obligation covers loyalty, care, confidentiality, and conflict disclosure.

How is a fiduciary different from a regular financial advisor?

A fiduciary must prioritize your interests at all times, while a non-fiduciary broker-dealer only needs to recommend suitable products. The fiduciary standard is stricter and carries legal accountability.

Are all CFP® professionals fiduciaries?

Yes. CFP® professionals are held to a fiduciary standard and must prioritize client needs while disclosing all conflicts of interest.

What changed with fiduciary rules in 2026?

The DOL’s 2024 Retirement Security Rule was vacated by federal courts, restoring the older ERISA five-part test for fiduciary classification in retirement advice. This narrowed which retirement advisors are automatically held to a fiduciary standard.

How do I verify if my advisor is a fiduciary?

Ask them directly for written confirmation, review their Form ADV disclosure, and check their registration through SEC or FINRA public databases.