TL;DR:

- ETFs are investment funds that trade on exchanges like stocks, offering instant diversification across various asset classes. They differ from mutual funds by trading intraday at market prices and generally provide tax efficiency, low costs, and flexibility, but require understanding risks such as bid-ask spreads and leverage resets. Proper use of ETFs involves aligning them with specific goals, avoiding overconfidence, and understanding their structural advantages and limitations for effective wealth building.

Exchange-traded funds are everywhere in financial headlines, brokerage ads, and retirement plan menus. Yet most working professionals still confuse them with mutual funds, treat them like individual stocks, or worse, buy a leveraged ETF thinking it works just like a plain index fund. ETFs are genuinely different from both, and that difference shapes how you build wealth, manage taxes, and respond to market swings. This guide cuts through the noise and gives you a clear, practical picture of what ETFs are, how they actually work, and how to use them wisely.

Table of Contents

- What is an ETF? The basics explained

- How ETFs trade: Pricing, spreads, and the creation/redemption process

- ETFs vs mutual funds: Key differences for investors

- Understanding ETF structure, types, and regulatory safeguards

- Using ETFs in your investment strategy: Benefits, risks, and pro tips

- The uncomfortable truth most ETF guides ignore

- Ready to start or level up your ETF investing?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| ETF basics | An ETF is a basket of assets you can buy and sell on an exchange throughout the trading day. |

| How ETFs trade | ETFs offer intraday pricing and liquidity, but market price can differ from net asset value. |

| ETF vs mutual fund | ETFs trade like stocks while mutual funds only trade once daily, making ETFs more flexible for investors. |

| Regulation matters | Not all products called ‘ETFs’ are regulated the same—always check for SEC registration. |

| Consider the risks | Some ETFs, especially leveraged and inverse types, carry complex risks that long-term investors should understand. |

What is an ETF? The basics explained

An ETF (exchange-traded fund) is an investment fund that holds a basket of underlying assets and whose shares trade on an exchange like a stock. That single sentence is doing a lot of work, so let’s unpack it.

When you buy one share of an ETF, you are not buying a single company’s stock. You are buying a proportional slice of a fund that may hold dozens, hundreds, or even thousands of securities. Think of it like buying a single box of a mixed assortment rather than choosing individual pieces. One transaction gets you immediate exposure to a whole collection of assets.

ETFs can hold a wide variety of asset types, including:

- Stocks from a specific index (like the S&P 500), a sector (like technology), or a region (like emerging markets)

- Bonds, both government and corporate, across different maturities and credit qualities

- Commodities such as gold, silver, or oil through futures contracts or physical holdings

- A mix of asset classes for balanced or multi-asset strategies

One of the most powerful features for individual investors is the ability to get this diversification in a single trade. For someone just building a portfolio, an ETFs for beginners guide can help you understand which fund types match your goals right from the start. Rather than researching and buying 50 separate stocks, you buy one ETF and own all of them at once.

ETFs trade at market prices that change throughout the day. The price you pay at 10 a.m. may be different from the price at 3 p.m., which is a key distinction from how traditional mutual funds work.

The simplicity of this structure is genuinely attractive. You open a standard brokerage account, search for an ETF ticker symbol, and buy shares just as you would a share of Apple or Microsoft. No minimum investment hurdles, no complex paperwork, and no waiting until the market closes to know your purchase price.

How ETFs trade: Pricing, spreads, and the creation/redemption process

Understanding how ETF prices work will save you money and prevent frustrating surprises. ETFs typically have two key prices: a continuously traded market price (bid/ask) and a daily calculated net asset value (NAV) after the market closes. These two numbers are usually very close together, but not always identical.

Here is a quick breakdown of the terms you need to know:

| Term | What it means | Why it matters |

|---|---|---|

| Market price | The price buyers and sellers agree on during trading hours | This is what you actually pay |

| NAV | The total value of fund assets divided by shares outstanding | Benchmark for fair value |

| Bid price | The highest price a buyer is currently offering | You sell at or near this |

| Ask price | The lowest price a seller is currently accepting | You buy at or near this |

| Bid/ask spread | The gap between bid and ask prices | Represents a trading cost |

The bid/ask spread is a cost that many new investors overlook. On highly liquid ETFs tracking major indexes, this spread may be just a penny or two per share. On smaller, niche ETFs with lower trading volume, it can be significantly wider. Always check the spread before trading, especially in volatile markets.

The mechanism that keeps ETF market prices close to NAV is called the creation and redemption process. The ETF creation and redemption mechanism in the primary market helps keep ETF share prices close to the value of their underlying holdings, using authorized participants (APs). APs are large financial institutions, usually major banks or broker-dealers, that can create new ETF shares by delivering the underlying basket of securities to the fund, or redeem existing shares in exchange for the underlying assets. When ETF shares trade at a premium to NAV, APs create new shares and sell them, pushing the price down. When shares trade at a discount, APs buy shares and redeem them, pushing the price back up.

As a retail investor, you never interact with this creation/redemption process directly. But you benefit from it every single time you trade, because it keeps the market price honest. The ETF market growth projections underscore how this structure has attracted enormous investor confidence over the past decade.

Pro Tip: For frequently traded, large ETFs on major indexes, the bid/ask spread is rarely a meaningful cost. For sector-specific or thinly traded ETFs, compare the spread as a percentage of the share price before placing your order. You may be paying more than you realize just to get in.

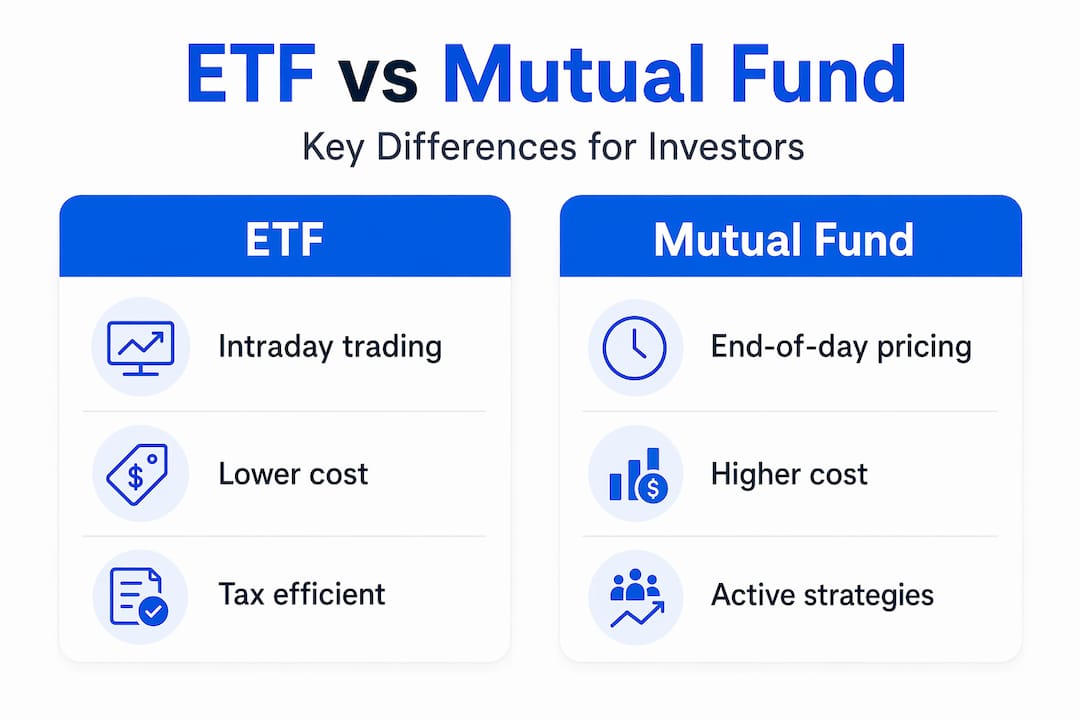

ETFs vs mutual funds: Key differences for investors

This comparison trips up many investors, including experienced ones. Both products hold diversified baskets of securities and both are regulated investment funds. But the practical differences matter enormously for how you invest.

A central practical distinction is that ETFs trade intraday on an exchange, while mutual funds transact at the end-of-day NAV. Here is why that distinction has real consequences:

- Pricing timing: ETFs let you see and act on the current price at any moment during market hours. Mutual fund orders are processed after the market closes, at a price you do not know when you place the order.

- Minimum investments: Many mutual funds require $1,000 to $3,000 to get started. Most ETFs require only the cost of one share, which can be as low as $10 to $50 for some funds.

- Load fees: Some mutual funds still charge sales loads (front-end or back-end commissions). ETFs do not have loads, though you may pay a brokerage commission or bid/ask spread.

- Tax efficiency: ETFs tend to generate fewer taxable capital gains distributions compared to mutual funds, largely because of the creation/redemption mechanism.

- Flexibility: You can place limit orders, stop-loss orders, and even short-sell ETFs. You cannot do any of that with mutual funds.

For a side-by-side breakdown, a detailed ETF vs. mutual fund comparison can help you evaluate which structure fits your specific financial situation. You can also review a broader ETF and mutual fund guide for updated perspectives heading into 2026.

That said, mutual funds are not bad products. Many excellent actively managed strategies are only available as mutual funds. The point is to understand what you are buying and how it behaves, especially when markets move quickly.

Understanding ETF structure, types, and regulatory safeguards

Here is something most ETF guides skip over: not everything labeled “ETF” is necessarily the SEC-registered ETF structure investors commonly mean. Regulators distinguish ETFs from other exchange-traded products (ETPs), and this distinction has real investor protection implications.

An SEC-registered ETF is subject to the Investment Company Act of 1940, which provides significant investor protections including independent board oversight, regular disclosure requirements, and strict rules around leverage and concentration. Other ETPs, such as exchange-traded notes (ETNs) or some commodity products, may be structured as debt obligations or limited partnerships, carrying very different risk profiles.

Common ETF types you will encounter:

- Equity ETFs: Track stock indexes or sectors. The most widely used category.

- Bond ETFs: Hold government, corporate, or municipal bonds. Useful for income and diversification.

- Commodity ETFs: Provide exposure to gold, oil, agricultural products, or broad commodity indexes.

- Leveraged ETFs: Aim to deliver 2x or 3x the daily return of an index. Complex and risky.

- Inverse ETFs: Designed to move opposite to an index. Used mainly for hedging or speculation.

- Thematic ETFs: Focus on specific trends like clean energy, artificial intelligence, or genomics.

- ESG ETFs: Screen holdings based on environmental, social, and governance criteria.

- Actively managed ETFs: A fund manager makes security selection decisions rather than following a fixed index.

The FINRA ETF types resource provides a useful breakdown of these product categories and their associated risks. One striking data point: actively managed ETFs have grown from a niche category to representing more than 7% of total U.S. ETF assets as of recent industry data, reflecting strong investor demand for professional stock-picking within the ETF wrapper.

Always read the prospectus before buying any ETF. The prospectus tells you the fund’s objective, what it holds, how it is structured, what it costs, and whether it is SEC-registered. For insights on new ETF innovations, including prediction market ETFs currently under regulatory review, the landscape is moving fast.

Using ETFs in your investment strategy: Benefits, risks, and pro tips

Let’s get practical. ETFs offer genuine advantages, but they also come with risks that are easy to miss when you are focused on the convenience and low cost.

Key benefits:

- Diversification at low cost: A single S&P 500 ETF gives you exposure to 500 companies with one trade and an annual fee as low as 0.03%.

- Flexibility: Buy or sell any time the market is open. Set limit orders to control your entry price.

- Tax efficiency: The creation/redemption mechanism typically avoids triggering capital gains distributions, making ETFs especially useful in taxable accounts.

- Transparency: Most ETFs disclose their full holdings daily, unlike many mutual funds that report quarterly.

- Broad market access: Want exposure to Japanese small-cap stocks, investment-grade corporate bonds, or healthcare companies? There is likely an ETF for each.

Key risks to watch:

- Market risk: ETFs do not eliminate the risk that markets fall. A diversified ETF still drops in a downturn.

- Bid/ask spread costs: As discussed, these can be meaningful for illiquid funds, especially if you trade frequently.

- Complexity in non-standard ETFs: Leveraged, inverse, and some thematic ETFs behave in ways that surprise investors who do not read the fine print.

- Tracking error: Some ETFs do not perfectly replicate their target index, resulting in returns that drift slightly from what you expected.

On leveraged and inverse ETFs specifically, the risk is real and underappreciated. Leveraged and inverse ETFs can behave very differently from what many investors expect over longer holding periods because they reset leverage on a frequent (typically daily) basis and therefore are mainly designed for short-term use. A 2x leveraged ETF does not simply double your annual return. It doubles the daily return and resets. In volatile markets, this daily compounding can lead to substantial losses even when the underlying index finishes roughly flat over the period.

Pro Tip: For long-term goals like retirement or education savings, stick to plain equity or bond ETFs with low expense ratios. Reserve leveraged or inverse ETFs for sophisticated, short-term tactical plays only if you fully understand how daily resets affect compounding. The step-by-step ETF guide on this site walks through building a starter portfolio with the right fund types for each goal.

The uncomfortable truth most ETF guides ignore

Here is the reality: ETFs are a vehicle, not a strategy. Treating them as a strategy is the single most common mistake we see investors make.

The marketing around ETFs has been almost universally positive for the past decade, and for good reason. They are genuinely efficient, transparent, and cost-effective. But that positivity has a side effect. It creates overconfidence. Investors who feel they have “solved” investing by buying ETFs sometimes skip the harder work of understanding their own risk tolerance, time horizon, and actual portfolio construction.

Easy diversification sounds great. But easy diversification can also mean buying five ETFs that all hold the same 50 large-cap tech stocks with significant overlap, without realizing you are not actually diversified at all. Or buying a thematic ETF on a trend you read about after the major gains have already been captured.

There is also the question of ETF tax nuances that most guides mention briefly but do not explain fully. The creation/redemption tax advantage is real, but it is not unlimited. Investors in high-turnover active ETFs or certain commodity ETFs may face unexpected tax bills. The wrapper does not automatically equal tax efficiency.

The real work is not finding the “best ETF.” It is knowing why you are buying it, how it fits your broader financial picture, and what you will do when it drops 30%. The investors who struggle most are not the ones who picked the wrong fund. They are the ones who had no plan when volatility hit. The ETF did exactly what it was designed to do. The investor was simply unprepared for what that meant in practice.

Ready to start or level up your ETF investing?

Whether you are just getting started or looking to sharpen a strategy you have already built, having the right resources makes a significant difference. At finblog.com, we have built a library of practical, no-nonsense guides designed for working professionals who want to invest intelligently without spending hours parsing financial jargon. From our ETF investing basics walkthrough to deeper dives into fund selection, tax strategy, and portfolio construction, you will find content that meets you where you are. Explore the site, use the guides, and if you want personalized guidance, our consultation resources are there to help you take the next concrete step toward your financial goals.

Frequently asked questions

What does an ETF actually invest in?

An ETF holds multiple asset types such as stocks, bonds, or commodity exposures depending on its stated objective, giving investors diversified exposure through a single fund share.

How does ETF pricing work compared to stocks or mutual funds?

ETFs are bought and sold on an exchange during market hours at live prices, while mutual funds are priced at NAV after the trading day ends, meaning you always know your ETF cost at execution.

Are all products labeled “ETF” the same under the law?

No. Regulators distinguish ETFs from other exchange-traded products (ETPs), and some products use the term without being SEC-registered investment funds, so always verify registration in the prospectus.

Can I buy and sell an ETF at any time during market hours?

Yes. ETFs trade at market prices that change throughout the day, so you can buy or sell shares any time the stock exchange is open, just like individual stocks.

What are the risks of leveraged or inverse ETFs?

Leveraged and inverse ETFs reset their leverage daily, which means long-term returns can diverge sharply from simple expectations, making these products unsuitable for most buy-and-hold investors.