TL;DR:

- Proper planning, including legal documents and communication, is essential to preserve family wealth.

- Using a combination of wills, trusts, gifting, and insurance optimizes wealth transfer and tax efficiency.

- Regular reviews and family conversations prevent conflicts and ensure plans stay current across generations.

Most families believe their wealth will naturally pass to the next generation. The reality is far less comfortable. Without deliberate planning, a lifetime of accumulated assets can vanish within a generation or two, lost to taxes, legal disputes, or simple miscommunication between family members. The risks are not hypothetical. Poor documentation, outdated beneficiary designations, and avoided conversations about money are the real threats to your legacy. This article walks you through proven strategies for transferring generational wealth, common pitfalls to avoid, and the practical steps that separate families who preserve their legacy from those who watch it disappear.

Table of Contents

- What is generational wealth transfer?

- Core strategies for effective wealth transfer

- Comparing popular wealth transfer vehicles

- Common pitfalls and how to avoid them

- A fresh perspective: How real legacy is built

- Ready to secure your family’s legacy?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Plan proactively | Early and thorough planning prevents costly mistakes in wealth transfer. |

| Use the right tools | Trusts, wills, and strategic gifting are key to protecting generational assets. |

| Avoid common errors | Regular reviews and professional guidance help sidestep expensive pitfalls. |

| Communicate with heirs | Clear conversations with future generations preserve both assets and family harmony. |

What is generational wealth transfer?

Generational wealth transfer is the process of passing financial assets, property, investments, and other resources from one generation to the next in a deliberate and structured way. It sounds straightforward, but the execution is where most families stumble.

The concept goes beyond simply writing a will. True wealth transfer involves legal structures, tax planning, family communication, and ongoing management. It requires you to think about not just what you leave behind, but how and when it reaches your heirs.

Why do so many families fail at this? The reasons are surprisingly consistent. Family conflict over asset distribution is one of the most common causes of wealth erosion. Add to that a lack of proper legal documents, outdated estate plans, and the compounding effect of estate taxes, and you can see why generational wealth planning demands serious attention.

“Many families fail to preserve wealth beyond the second or third generation.” This pattern, sometimes called “shirtsleeves to shirtsleeves in three generations,” appears across cultures worldwide and underscores how universal the challenge truly is.

Several myths make this problem worse. Here are the most damaging misconceptions families carry into estate planning:

- A will is enough. Wills only cover probate assets and do not protect against taxes or family disputes.

- Wealth transfer is only for the ultra-rich. Any family with property, savings, or a business needs a plan.

- My family will figure it out. Without clear instructions, families often do not figure it out, and courts may decide for them.

- One plan lasts forever. Tax laws change, family circumstances shift, and plans that worked a decade ago may now be outdated.

- Talking about money is taboo. Avoiding these conversations is one of the fastest ways to guarantee conflict later.

Understanding these misconceptions is the first step toward building a plan that actually works.

Core strategies for effective wealth transfer

Once you understand the stakes, the next step is knowing which tools to use. Effective wealth transfer is not a single action. It is a layered strategy built from multiple complementary methods.

Here are the foundational steps every family should consider:

- Create or update your will. A will is the baseline document. It names your beneficiaries, designates an executor, and outlines your wishes. Without one, state law decides who gets what.

- Establish a trust. Trusts offer control that a will simply cannot match. You can set conditions on distributions, protect assets from creditors, and avoid the time-consuming probate process. Trust fund basics are worth understanding before deciding which type fits your situation.

- Use strategic gifting. In 2026, the annual gift tax exclusion allows individuals to give up to $18,000 per recipient without triggering gift taxes. This is a powerful, underused tool for gradually transferring wealth during your lifetime.

- Plan charitable contributions. Donor-advised funds and charitable remainder trusts can reduce your taxable estate while supporting causes that matter to your family.

- Review beneficiary designations. Retirement accounts and life insurance policies pass outside of your will. Keeping these designations current is critical.

The combination of these approaches is what wealth transfer strategies consistently recommend, because using trusts and gifting reduces estate taxes and helps preserve more of what you have built. Physical asset protection importance also plays a role, particularly for families with significant tangible property.

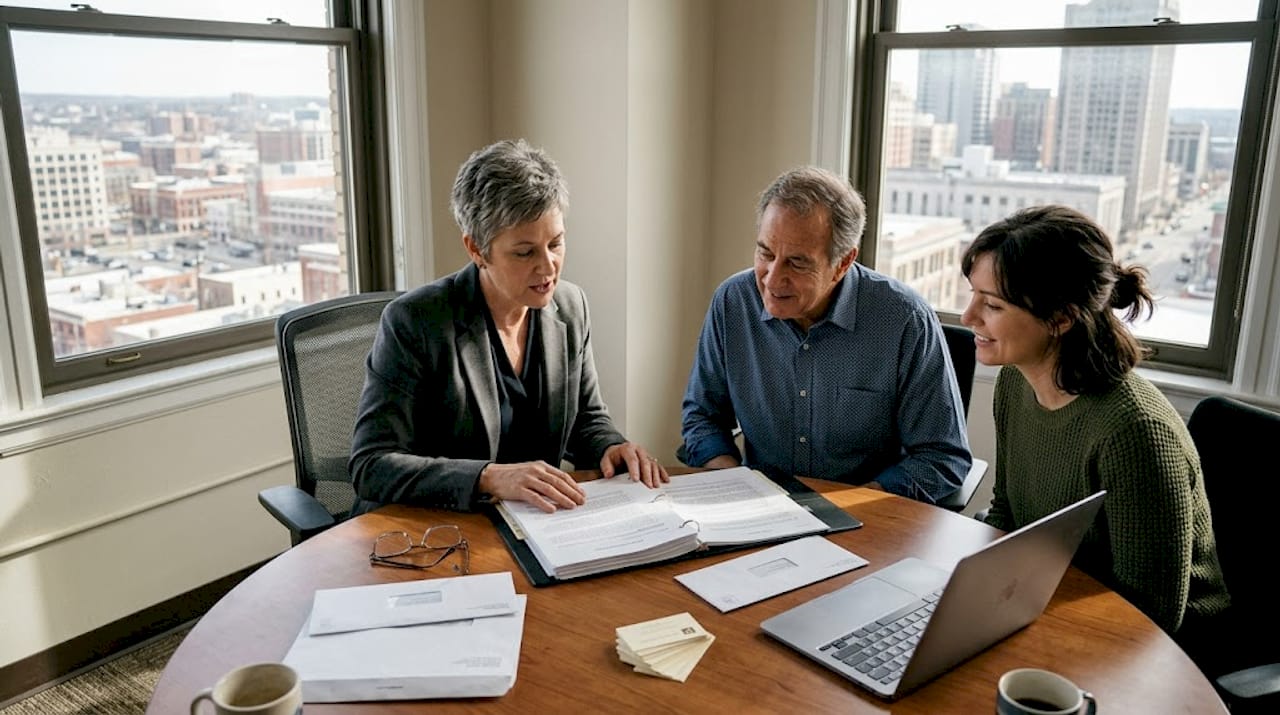

Pro Tip: Schedule a family meeting to discuss your intentions before finalizing any documents. Heirs who understand your wishes in advance are far less likely to contest decisions or create conflict after you are gone.

Comparing popular wealth transfer vehicles

Not all wealth transfer tools work the same way, and choosing the wrong one for your situation can cost your family significantly. Here is a clear comparison of the most widely used vehicles:

| Vehicle | Key benefit | Key limitation | Best for |

|---|---|---|---|

| Will | Simple and flexible | Subject to probate | Basic asset distribution |

| Revocable trust | Avoids probate, flexible | Does not reduce estate taxes | Privacy and control |

| Irrevocable trust | Tax advantages, asset protection | Loss of control over assets | Large estates, tax planning |

| Life insurance | Tax-free death benefit | Ongoing premium costs | Liquidity and estate equalization |

| Direct gifting | Immediate transfer, tax-efficient | Annual limits apply | Gradual wealth reduction |

| Family foundation | Charitable legacy, tax benefits | Administrative complexity | Philanthropic families |

As the table shows, each vehicle has a distinct role. Trusts offer more control than wills, but they require setup costs and ongoing administration. Life insurance is often overlooked as an estate planning tool, yet it provides immediate liquidity to cover taxes or equalize inheritances among heirs.

One critical statistic worth noting: roughly 60% of American estates go through probate, a process that can take months or years and reduce the value passed to heirs through legal fees and delays. Trusts sidestep probate entirely, which is a major advantage for larger or more complex estates.

The smartest approach for most families is to combine vehicles. A revocable trust handles the bulk of your assets, while direct gifting chips away at your taxable estate over time, and life insurance covers any liquidity gaps. Exploring wealth preservation strategies can help you identify the right combination for your specific situation. You can also review asset protection strategies to understand how physical and financial assets work together in a complete plan.

The trust vs will guide on Finblog breaks down these distinctions in practical terms if you want to go deeper on that comparison.

Common pitfalls and how to avoid them

Even families with solid plans can see their legacy unravel because of avoidable mistakes. Knowing what to watch for is half the battle.

Here are the most common pitfalls and how to address them:

- Not updating documents. Life changes fast. Marriages, divorces, births, and deaths all affect who should receive your assets. Failure to update beneficiary information can cost families millions, particularly when an ex-spouse remains listed on a retirement account.

- Skipping the conversation. Families that never discuss wealth transfer plans are far more likely to face disputes. Heirs who feel blindsided often challenge documents in court.

- Ignoring tax implications. Estate taxes, capital gains taxes, and income taxes on inherited retirement accounts can all reduce what heirs actually receive. Planning around these is not optional.

- Relying on a single advisor. Estate planning sits at the intersection of law, taxes, and financial planning. One professional rarely covers all three areas well.

- Assuming the plan is permanent. Tax laws change. The federal estate tax exemption, for example, has shifted dramatically over the past two decades. What works today may not work in five years.

Real-world scenarios make this concrete. Consider a family that set up a trust in 2010 but never updated it after a divorce. When the original grantor passed away, a former spouse was still named as a trustee, triggering a legal battle that consumed years and significant legal fees. Reviewing wealth protection tips regularly prevents exactly this kind of outcome.

Pro Tip: Build a recurring annual review into your calendar, ideally with your estate attorney and financial advisor together. Treat it like a financial physical exam. Also explore generational financial planning resources to stay current on best practices between formal reviews.

For physical assets, why asset protection matters is worth reading to understand how protecting tangible property fits into your broader estate plan.

A fresh perspective: How real legacy is built

Here is something most estate planning articles will not tell you: the families who successfully transfer wealth across multiple generations are not necessarily the ones with the most sophisticated legal structures. They are the ones who invest as much in relationships and shared values as they do in documents.

We have seen families with ironclad trusts and perfectly drafted wills still lose everything to internal conflict within a decade. And we have seen families with modest estates preserve their wealth for generations simply because they talked openly about money, taught their children how to manage it, and created a shared sense of purpose around what the wealth was for.

The role of financial advisors is important, but advisors cannot substitute for family alignment. A trust cannot make your heirs responsible stewards. Only intentional education and honest conversation can do that.

The real work of legacy building happens at the dinner table, not just in the attorney’s office.

Ready to secure your family’s legacy?

You now have a clear picture of what effective generational wealth transfer looks like and where most families go wrong. The next step is putting that knowledge into action. Finblog offers a library of wealth guides covering every aspect of estate planning, from foundational concepts to advanced tax strategies. Whether you are just starting to think about your legacy or need to update an existing plan, our resources are built to help you move forward with confidence. Revisit wealth transfer strategies for a deeper look at the tools covered here, and consider connecting with a financial advisor to build a plan tailored to your family’s specific goals.

Frequently asked questions

What is the biggest risk in generational wealth transfer?

The biggest risk is lack of planning, which often results in family disputes, lost assets, and heavy taxation. Most wealth is lost by the third generation due to poor planning and inadequate family communication.

How do trusts help with generational wealth?

Trusts let you set rules for how assets are managed and distributed, protecting your legacy from legal and tax issues. Trusts provide control that wills alone simply cannot offer, especially for complex or high-value estates.

How often should wealth transfer plans be reviewed?

Wealth transfer plans should be reviewed at least once a year, or after any major life event or law change. Regular reviews are necessary to adapt to changes and avoid costly errors that accumulate over time.

Can I transfer wealth without paying taxes?

Some strategies, like strategic gifting and charitable contributions, can reduce taxes, but complete avoidance is rare. Tax-efficient planning preserves more wealth by minimizing exposure rather than eliminating taxes entirely.

Why should I involve a financial advisor?

Financial advisors help spot potential pitfalls and ensure your legacy plan meets both legal and financial goals. Professional advice prevents major mistakes that self-directed planning often misses, particularly around tax law and beneficiary coordination.

Recommended

- Generational Wealth Planning: Securing Your Legacy – Finblog

- Wealth Transfer Strategies: Secure Your Financial Legacy – Finblog

- Master Generational Financial Planning for Lasting Wealth – Finblog

- How to Build Wealth: Proven Steps for Lasting Financial Success – Finblog

- Why invest in asset protection: cut risks by 40% in 2026 – Safes and Security Direct