Stocks pushed higher for a second day as investors reacted to signals that the US may soon step back from the Iran war, easing pressure on oil and inflation.

Wall Street ended Wednesday in positive territory after Donald Trump signalled a possible fast US exit from Iran, saying the country could be “out pretty quickly,” while still leaving room for targeted future strikes.

That single shift in tone was enough to move markets.

Investors, who had been pricing in prolonged geopolitical risk, quickly rotated back into equities, especially into growth and tech stocks.

The result was a broad rally. The S&P 500 rose 0.72%, the Nasdaq jumped 1.16%, and the Dow gained 0.48%. At the same time, the CBOE Volatility Index dropped to its lowest level in over a week, showing that market fear is already fading.

But the real story is not just the rally. It is what the market is pricing in next.

Investors are following a clear logic: Less war risk → Lower oil prices → Lower inflation → Better conditions for stocks

That expectation is already reshaping positioning.

This is why tech stocks led the move. When inflation pressure eases, interest rate fears also ease, and that directly benefits high-growth companies.

- Alphabet surged 3.4%

- Meta Platforms and Amazon gained over 1%

- Semiconductor stocks jumped for a second straight session

At the same time, sector rotation became very clear.

Energy stocks dropped sharply as oil prices fell, while airline stocks moved higher as cheaper fuel improves margins. This reflects how quickly markets adjust when macro expectations shift.

Several company-specific catalysts added to the momentum.

- Intel jumped 8.8% after announcing a $14.2 billion buyback deal

- Eli Lilly rose 3.8% following FDA approval of its new weight-loss drug

- Space stocks rallied after reports that SpaceX filed confidentially for an IPO

However, not everything followed the upward trend.

Nike collapsed 15.5%, hitting its lowest level in a decade after warning of a surprise drop in sales. It was the biggest negative outlier of the day.

Zooming out, the broader market still tells a more cautious story.

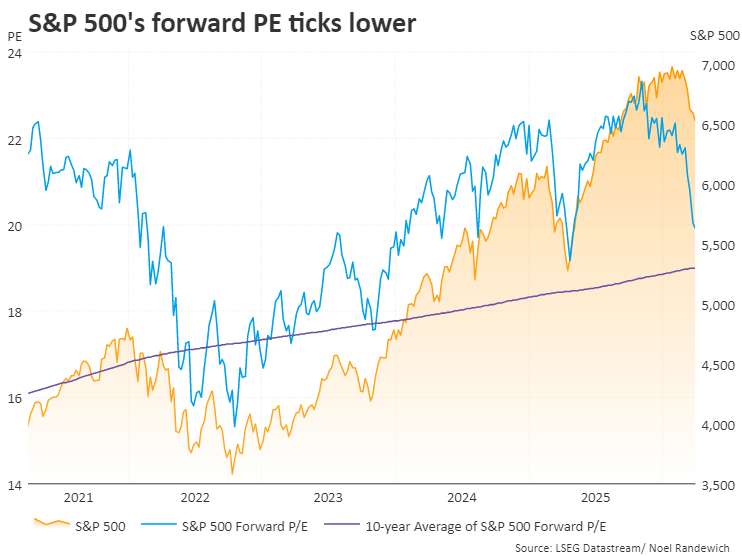

The S&P 500 remains down around 4% in 2026, and valuations have compressed, with the index now trading at its lowest forward P/E in 10 months.

So here is where things get interesting. Is this the beginning of a real recovery… or just a short-term relief rally?

Because one major risk has not gone away. Inflation is still elevated.

In fact, markets are increasingly pricing in a potential rate hike by the Federal Reserve by year-end, instead of the previously expected cuts. That puts investors in a two-sided market:

- Bull case: Geopolitical tensions ease, oil falls, markets recover

- Bear case: Inflation stays high, rates go up, pressure returns

So the next move depends on one key question: Which matters more right now, falling war risk or persistent inflation?

That is what the market is trying to figure out next.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related: Is the US headed for a recession? The Iran war could tip the balance