Many investors believe complex hedging models deliver superior protection, but research reveals a counterintuitive truth: simpler strategies often outperform sophisticated alternatives. Naïve hedging outperforms complex risk models across multiple asset classes and timeframes. This guide explores proven hedging methods that reduce portfolio volatility without overwhelming complexity. You will discover actionable techniques to enhance your risk management skills, from diversification fundamentals to dynamic approaches used by professionals. Whether you are building your first hedged portfolio or refining existing strategies, these evidence-based insights help you protect capital while maintaining growth potential.

Table of Contents

- Key takeaways

- Why simple hedging strategies often outperform complex models

- Core hedging methods: diversification, static, and dynamic approaches

- Nuances of selective hedging and regime-based hedge allocations

- Applying hedge fund insights and professional hedging tactics

- Explore comprehensive resources on investment and risk management

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Naive hedging outperforms | Using a simple 1 to 1 futures hedge ratio reduces portfolio risk without forecasting or complex model inputs. |

| Diversification reduces volatility | Diversifying across uncorrelated assets lowers overall volatility and complements hedges. |

| Dynamic hedging advantages | Dynamic hedging adapts to shifting correlations and market conditions, often outperforming static approaches. |

| Minimum variance hedging works | Traditional minimum variance hedging remains effective even when analysts pursue selective hedging. |

| Equity long short leads | Recent results show equity long short hedge funds delivering stronger returns relative to other hedge strategies. |

Why simple hedging strategies often outperform complex models

The financial industry promotes sophisticated hedging models with advanced mathematics and proprietary algorithms. Yet decades of empirical evidence tells a different story. Naïve hedging outperforms complex risk models by using a straightforward 1:1 futures hedge ratio that consistently reduces portfolio risk measures like Value at Risk and Conditional Value at Risk.

Complex models introduce estimation errors that compound during volatile periods. When market conditions shift rapidly, intricate calculations based on historical correlations break down. The models that promised precision become liability generators. Statistical analysis across commodities, currencies, and equity indexes spanning multiple decades confirms this pattern repeatedly.

“Simplicity in hedging provides robustness when markets behave unpredictably, while complexity adds layers of potential failure points.”

Naïve hedging works because it avoids the estimation risk inherent in calculating optimal hedge ratios. You match your exposure with an equal offsetting position in futures contracts. No forecasting required. No correlation matrices to update. This approach proves especially valuable during market stress when correlations shift unexpectedly.

Consider these advantages of straightforward hedging:

- Eliminates model specification errors that plague complex approaches

- Requires minimal data inputs and computational resources

- Performs consistently across different asset classes and time periods

- Reduces implementation costs and operational complexity

- Maintains effectiveness during regime changes and market dislocations

The relationship between hedging and portfolio diversification benefits creates additional risk reduction. While hedging addresses specific exposures, diversification spreads risk across uncorrelated assets. Together, these strategies form a comprehensive risk management framework that does not rely on accurate forecasting or complex modeling.

Pro Tip: Start with naïve hedging for your largest exposures before exploring more sophisticated approaches. Master the basics first, then add complexity only when you can measure clear improvements in risk-adjusted returns.

Market practitioners often chase the newest hedging innovations, but empirical research consistently validates simpler methods. The hedge ratio that works is the one you can implement reliably and maintain through changing conditions. Complexity for its own sake adds cost without corresponding benefit. Focus on execution quality rather than model sophistication.

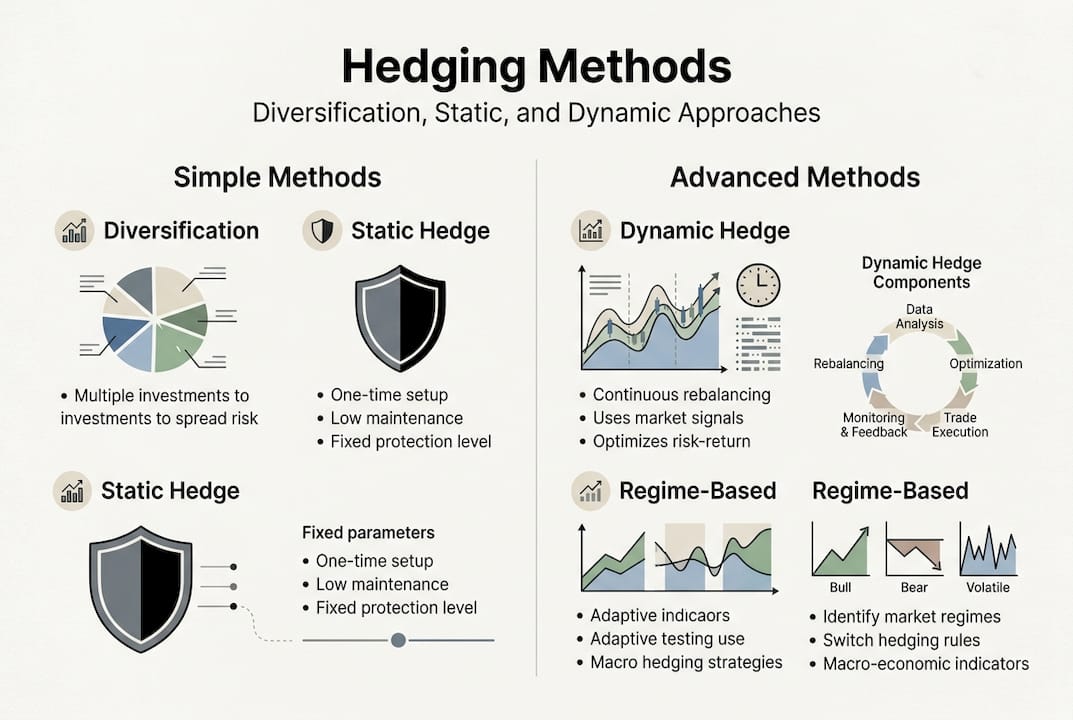

Core hedging methods: diversification, static, and dynamic approaches

Three fundamental hedging techniques form the foundation of portfolio protection strategies. Each serves distinct purposes and suits different investor circumstances. Understanding their mechanics and trade-offs helps you build an appropriate risk management framework.

Effective hedging strategies begin with diversification through Modern Portfolio Theory principles. Allocating capital across uncorrelated assets reduces volatility by ensuring that losses in one position offset gains elsewhere. This approach does not eliminate risk but spreads it across multiple sources, lowering overall portfolio variance.

| Hedging Method | Implementation | Best For | Key Limitation |

|---|---|---|---|

| Diversification | Allocate across uncorrelated assets | Long-term investors | Does not protect against systemic shocks |

| Static Hedging | Fixed hedge ratios maintained | Predictable exposures | Ignores changing market conditions |

| Dynamic Hedging | Adjust based on market factors | Active managers | Requires continuous monitoring |

| Naïve Hedging | 1:1 futures ratio | Simplicity seekers | May not optimize hedge efficiency |

Static hedging establishes fixed hedge ratios that remain constant regardless of market movements. You determine your exposure, calculate an appropriate hedge size, and maintain that position. This method offers simplicity and low transaction costs. Implementation requires minimal oversight once positions are established. However, static hedges cannot adapt when correlations shift or when market regimes change.

Dynamic hedging incorporates market factors like trend, value, and carry into hedge adjustments. Dynamic FX hedging performance demonstrates superior returns and risk management compared to static methods. The strategy responds to evolving conditions by increasing hedges when risk rises and reducing them when opportunities emerge.

Consider these implementation factors:

- Diversification works best for investors with long time horizons and tolerance for short-term volatility

- Static hedging suits situations with stable correlations and predictable risk exposures

- Dynamic approaches require analytical tools and active monitoring capabilities

- Transaction costs increase with dynamic strategies but may justify the expense through improved outcomes

The choice between static and dynamic hedging depends on your resources and market views. Static hedges provide peace of mind with minimal effort. Dynamic strategies demand attention but potentially deliver better risk-adjusted returns. Most investors benefit from combining approaches, using static hedges for core exposures while applying dynamic tactics to tactical positions.

Pro Tip: Track the correlation between your assets and hedge instruments monthly. When correlations deviate significantly from historical norms, reassess your hedge ratios even if you typically use static approaches.

Understanding dynamic asset allocation strategies enhances your ability to implement responsive hedging. The principles that guide tactical asset shifts apply equally to hedge adjustments. Market factors that signal allocation changes often indicate when hedge ratios need modification. Integration of these concepts creates a cohesive risk management system.

Your risk tolerance determines which methods suit your situation. Conservative investors may prefer diversification with static hedges, accepting some inefficiency for simplicity. Aggressive managers might embrace dynamic approaches despite higher costs and complexity. The optimal strategy balances protection effectiveness against implementation demands and personal capabilities.

Nuances of selective hedging and regime-based hedge allocations

Selective hedging tempts investors with the promise of improved returns through strategic timing. The approach incorporates return forecasts into hedge decisions, increasing hedges when losses seem likely and reducing them when gains appear probable. Research reveals this strategy backfires more often than it succeeds.

Selective versus traditional hedging shows that incorporating return forecasts increases portfolio risk without delivering commensurate returns. Traditional minimum-variance hedging, which ignores return predictions and focuses solely on risk reduction, proves empirically superior. The forecasting errors that plague return predictions contaminate hedge decisions, creating additional uncertainty rather than reducing it.

Why does selective hedging fail? Forecast accuracy remains elusive even for professional investors. Small prediction errors compound when translated into hedge adjustments. You end up under-hedged during downturns and over-hedged during rallies. The timing challenge that makes active management difficult applies equally to selective hedging.

Regime-based allocation offers a more robust alternative. Instead of forecasting returns, this approach identifies market volatility regimes and adjusts hedge assets accordingly. Regime-based hedge allocation using VIX demonstrates how volatility indexes guide shifts between hedge instruments.

| Volatility Regime | VIX Level | Recommended Hedge Asset | Rationale |

|---|---|---|---|

| Low Volatility | Below 15 | Long-duration bonds (TLT) | Negative correlation with equities |

| Moderate Volatility | 15-25 | Intermediate bonds | Balanced protection |

| High Volatility | Above 25 | Short-duration bonds (SHY) | Stability over correlation |

| Extreme Volatility | Above 35 | Cash equivalents | Capital preservation |

The VIX index serves as a market volatility proxy, signaling when correlations between assets may break down. During calm periods, traditional hedges like long-duration Treasury bonds provide effective equity protection. When volatility spikes, correlations converge and formerly uncorrelated assets move together. Shifting to stable assets like short-duration bonds or cash preserves capital when correlations fail.

This approach avoids return forecasting while remaining responsive to market conditions. You react to observable volatility rather than predict future returns. The distinction matters because volatility regimes persist longer and exhibit more stability than return patterns. Implementation requires monitoring the VIX and establishing predetermined thresholds for hedge shifts.

Pro Tip: Establish your regime thresholds during calm markets and commit to following them mechanically. Emotional override during volatile periods undermines the strategy’s effectiveness.

Understanding how to diversify investments naturally complements regime-based hedging. Natural diversification across truly uncorrelated assets provides baseline protection, while regime-aware hedging adds tactical adjustments. The combination delivers more robust risk management than either approach alone.

The lesson from selective hedging failures is clear: focus on what you can observe rather than what you must predict. Market volatility is measurable and actionable. Future returns remain uncertain despite sophisticated models. Regime-based approaches acknowledge this reality and build strategies around observable market conditions rather than hopeful forecasts.

Investors who insist on selective hedging should track their decisions rigorously. Document each hedge adjustment and the reasoning behind it. Review outcomes quarterly to assess whether your forecasting adds value or destroys it. Most investors discover that mechanical, regime-based rules outperform their discretionary timing attempts.

Applying hedge fund insights and professional hedging tactics

Professional hedge fund performance offers valuable lessons for individual investors seeking effective hedging strategies. Equity long/short strategies returned 15.0% in 2025, leading all hedge fund categories and outperforming major benchmarks. This success reflects sophisticated hedging techniques that balance long equity exposure with strategic short positions.

Equity long/short funds construct portfolios that capture upside while limiting downside through carefully selected short positions. The strategy hedges market risk by offsetting long holdings with shorts in overvalued securities or sectors expected to underperform. This approach delivered superior returns during 2025’s volatile conditions when traditional long-only portfolios struggled.

Professional hedging incorporates several advanced techniques:

- Options Greeks analysis to measure and manage exposure sensitivities

- Gamma exposure (GEX) monitoring to anticipate dealer hedging flows

- Factor models that identify systematic risk sources requiring hedges

- Correlation analysis across multiple timeframes and market regimes

- Dynamic position sizing based on realized and implied volatility

These methods require sophisticated tools and continuous monitoring, placing them beyond most individual investors’ capabilities. However, the underlying principles translate to simpler implementations. You can apply professional insights without replicating institutional infrastructure.

“The best hedge fund strategies succeed by identifying specific risks and addressing them directly rather than applying broad portfolio protection.”

Individual investors access equity long/short exposure through specialized ETFs and managed accounts. These vehicles provide professional management without requiring you to construct complex hedging positions. Evaluate options carefully, as fees and implementation quality vary significantly across providers. Review track records during both rising and falling markets to assess true hedging effectiveness.

The hedge funds performance during challenging periods reveals which strategies maintain discipline under stress. October 2024 tested many approaches, separating robust methodologies from fair-weather tactics. Strategies that preserved capital during that period demonstrated genuine hedging value rather than merely benefiting from favorable conditions.

Learning from investing strategies 2025 trends helps you understand which hedging approaches gained traction and why. Market conditions evolve, and effective hedging adapts accordingly. The strategies that worked in 2025’s environment may need adjustment for 2026’s challenges.

Professional investors increasingly incorporate market microstructure into hedging decisions. Dealer positioning and options market dynamics create predictable flows that informed hedgers exploit. While individual investors cannot trade based on real-time dealer hedging, understanding these forces explains sudden market moves and correlation breakdowns.

The gap between institutional and individual hedging capabilities narrows through education and selective tool adoption. You do not need a Bloomberg terminal to implement effective hedges. Focus on the core principles that drive professional success: identify specific risks, select appropriate hedge instruments, monitor effectiveness regularly, and adjust when conditions change.

Combining professional insights with accessible implementation creates practical hedging strategies. Study how hedge funds approach risk management, then translate those concepts into techniques you can execute with available resources. The goal is not to replicate institutional strategies exactly but to apply their proven principles within your constraints.

Explore comprehensive resources on investment and risk management

Effective hedging requires continuous learning as markets evolve and new techniques emerge. Finblog provides extensive resources to help you refine your portfolio management skills and stay current with proven strategies. Our guides cover everything from foundational concepts to advanced tactics used by professionals.

Explore detailed articles on portfolio diversification benefits that explain how spreading risk across uncorrelated assets enhances your hedging effectiveness. Learn about dynamic asset allocation strategies that adapt to changing market conditions, providing responsive protection when you need it most. Each resource offers actionable insights backed by empirical research and real-world application examples.

Our expert analysis helps you build robust investment strategies while protecting against downside risks. Whether you are establishing your first hedged positions or optimizing existing approaches, you will find practical guidance tailored to your experience level. Visit Finblog regularly for updates on market conditions, strategy performance reviews, and new techniques worth considering for your portfolio.

FAQ

What is the best hedging strategy for individual investors?

Naïve hedging using simple futures contracts often works best for individual investors due to its ease of implementation and proven effectiveness. This approach uses a 1:1 hedge ratio that requires minimal calculations and consistently reduces portfolio risk measures across different market conditions. The strategy avoids complex modeling errors while providing reliable protection.

How does diversification complement hedging?

Diversification reduces overall portfolio volatility by spreading investments across uncorrelated assets, creating a foundation that enhances specific hedging benefits. While hedging addresses particular exposures through offsetting positions, diversification provides broad-based risk reduction. Together, these approaches form a comprehensive risk management framework more robust than either technique alone.

Are dynamic hedging strategies suitable for all investors?

Dynamic hedging requires advanced analytical tools and continuous monitoring, making it better suited for professional investors or those with significant experience and resources. The strategy demands regular position adjustments based on evolving market factors, increasing transaction costs and time commitments. Most individual investors achieve better results with simpler static approaches unless they can dedicate substantial attention to active management.

What risks come with selective hedging?

Selective hedging that attempts to time markets by incorporating return forecasts often increases portfolio risk without delivering commensurate returns. Forecasting errors contaminate hedge decisions, leaving you under-protected during downturns and over-hedged during rallies. Research consistently shows traditional minimum-variance hedging outperforms selective approaches that rely on return predictions.

How important is volatility regime awareness in hedging?

Volatility regime awareness proves critical for determining which hedge assets to use, significantly improving risk management by adapting to observable market conditions. The VIX index serves as a reliable proxy for identifying regime shifts, guiding transitions between different hedge instruments as correlations change. This approach responds to measurable volatility rather than uncertain return forecasts, providing more robust protection.

What is naïve hedge ratio?

A naïve hedge ratio establishes a simple 1:1 relationship between your exposure and offsetting futures contracts, providing straightforward and effective risk reduction. This method avoids complex calculations and estimation errors while consistently lowering portfolio volatility measures. Despite its simplicity, empirical research shows it often outperforms sophisticated alternatives across multiple asset classes and time periods.

Can equity long/short hedge strategies benefit individual investors?

Equity long/short funds delivered 15.0% returns in 2025, demonstrating the strategy’s effectiveness, but implementation requires access to sophisticated platforms and deep market understanding. Individual investors can gain exposure through specialized ETFs or managed accounts that provide professional management without requiring direct position construction. However, you should carefully evaluate your risk tolerance and the fees associated with these vehicles before committing capital.