More than 40% of American investors hold bonds in their retirement portfolios, yet many still feel uncertain about how these investments work. Understanding bonds matters because they play a unique role in balancing risk and generating stable income compared to stocks. Whether you are looking to diversify or seeking reliable returns, learning how bonds function can empower any American to make smarter financial choices for long-term success.

Table of Contents

- What Are Bonds And How Do They Work

- Types Of Bonds And Their Unique Roles

- Risk And Return Profile Of Bonds

- Bonds For Portfolio Stability And Income

- Taxation, Costs, And Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understanding Bonds | Bonds are debt securities where investors lend capital to issuers in exchange for interest payments and principal repayment at maturity. |

| Types of Bonds | Different bond types, such as Government, Municipal, Corporate, and High-Yield bonds, cater to various risk profiles and investment goals. |

| Risk Analysis | Key risks include credit risk, interest rate risk, and inflation risk; diversifying your bond portfolio can help mitigate these risks. |

| Tax Considerations | Tax implications vary by bond type, with Municipal bonds often providing tax-exempt income, making understanding taxes crucial for maximizing returns. |

What Are Bonds and How Do They Work

A bond is a fundamental financial instrument where an investor essentially becomes a lender, providing capital to an entity in exchange for regular interest payments and the promise of full principal repayment. Bonds are debt securities that represent a loan made by an investor to a borrower, typically a government, municipality, or corporation seeking to raise funds.

At its core, a bond works like a structured loan agreement with specific parameters. When you purchase a bond, you are lending money to the issuer for a predetermined period. In return, the issuer commits to paying you periodic interest payments, known as coupon rates, and ultimately returning the full face value of the bond when it reaches maturity. These interest payments are typically fixed and provide a predictable income stream for investors, making bonds an attractive option for those seeking steady returns with lower risk compared to more volatile investments like stocks.

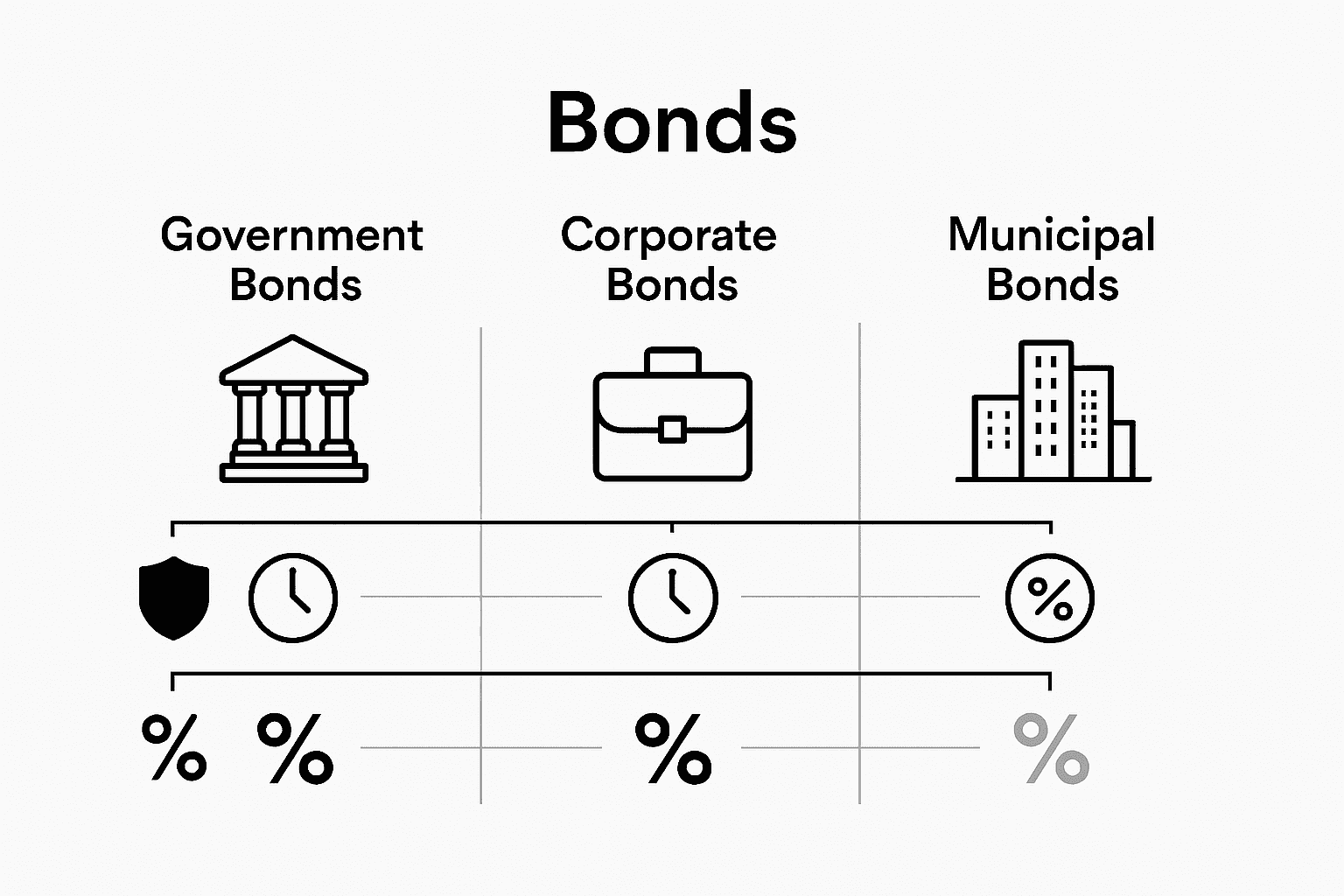

Bonds come in various types, each with unique characteristics:

- Government Bonds: Issued by national governments, considered the safest

- Municipal Bonds: Issued by local governments to fund public projects

- Corporate Bonds: Issued by companies to finance business operations

- Treasury Bonds: Specific U.S. government securities with longer maturity periods

Bond prices fluctuate based on several factors, including prevailing interest rates, the issuer’s creditworthiness, and overall economic conditions. When interest rates rise, existing bond prices typically fall, and vice versa. This dynamic relationship makes bonds not just a passive investment tool but a complex financial instrument responsive to broader economic trends.

Pro Tip – Bond Basics: Before investing, always check the bond’s credit rating and understand the issuer’s financial health to assess potential risks and expected returns.

Types of Bonds and Their Unique Roles

Investors have multiple bond options, each serving distinct financial purposes and risk profiles. Different bond types provide unique opportunities for generating income and managing investment portfolios. Understanding these variations helps investors strategically allocate their resources across diverse financial instruments.

Government bonds represent the most stable investment category. These securities, issued by national treasuries, are backed by the full faith and credit of the government, making them exceptionally low-risk. Treasury Bonds, Treasury Notes, and Treasury Bills offer varying maturity periods ranging from short-term to 30-year investments. These bonds are particularly attractive to conservative investors seeking guaranteed returns and minimal risk exposure.

Corporate and municipal bonds present more nuanced investment strategies:

- Corporate Bonds: Issued by companies to fund expansion, research, or operational needs

- Investment-Grade Bonds: Higher-rated securities from financially stable corporations

- High-Yield Bonds: Higher-risk securities offering potentially larger returns

- Municipal Bonds: Tax-advantaged securities issued by local governments

- Zero-Coupon Bonds: Sold at a discount, paying full face value at maturity

The bond market’s complexity extends beyond basic classifications. Risk levels, interest rates, and potential returns vary significantly across different bond types. Investors must carefully analyze credit ratings, economic conditions, and individual financial goals when selecting appropriate bond investments.

Here’s a concise comparison of major bond types and their key characteristics:

| Bond Type | Typical Risk Level | Average Maturity | Tax Implications |

|---|---|---|---|

| Government Bond | Very Low | 5-30 years | Taxable; some state exemptions |

| Municipal Bond | Low | 1-20 years | Often tax-exempt |

| Corporate Bond | Moderate-High | 1-30 years | Interest taxed as ordinary income |

| High-Yield Bond | High | 5-15 years | Fully taxable |

| Treasury Bond | Lowest | 10-30 years | Exempt from state tax |

Pro Tip – Bond Selection: Always diversify your bond portfolio across different types and issuers to balance potential risks and optimize overall investment performance.

Risk and Return Profile of Bonds

Bonds represent a nuanced investment vehicle with a spectrum of risk and potential returns that require careful analysis. Bond investments carry inherent risks that investors must understand to make informed decisions about their financial strategy. While generally considered more stable than stocks, bonds are not completely immune to economic fluctuations and potential financial challenges.

The risk profile of bonds varies significantly based on several key factors. Credit risk represents the primary concern, measuring the likelihood that the bond issuer might default on interest or principal payments. Government bonds typically carry the lowest credit risk, while corporate bonds—especially high-yield or “junk” bonds—present higher potential for default. Investment-grade corporate bonds offer a middle ground, providing somewhat higher returns with moderate risk compared to government securities.

Key risk factors influencing bond performance include:

- Interest Rate Risk: Bond values fluctuate inversely with interest rate changes

- Inflation Risk: Potential for bond returns to be eroded by rising inflation rates

- Credit Risk: Possibility of issuer defaulting on bond obligations

- Liquidity Risk: Difficulty selling bonds before maturity without potential loss

- Currency Risk: Potential value changes due to exchange rate fluctuations

Investors can mitigate bond investment risks through strategic diversification and careful selection. Understanding the relationship between risk and potential returns helps create a balanced portfolio that matches individual financial goals and risk tolerance. Higher-risk bonds generally offer higher potential returns, while lower-risk bonds provide more stability and predictable income streams.

The table below summarizes common bond risks and how investors can address them:

| Risk Type | Impact on Investor | Example Mitigation Strategy |

|---|---|---|

| Interest Rate | Lower bond prices | Laddering bond maturities |

| Credit | Loss from issuer default | Choosing higher-rated bonds |

| Inflation | Reduced real returns | Investing in TIPS or I-Bonds |

| Liquidity | Difficulty selling quickly | Favoring liquid bond markets |

| Currency | Value affected by FX shifts | Focus on domestic bonds |

Pro Tip – Risk Management: Regularly review and rebalance your bond portfolio, considering your changing financial circumstances and broader economic trends.

Bonds for Portfolio Stability and Income

Bonds serve as a critical component in creating a balanced investment strategy, offering investors a reliable mechanism for generating steady income and mitigating portfolio volatility. Understanding the role of fixed-income investments helps investors develop more robust financial frameworks that protect wealth while generating predictable returns.

The primary advantage of incorporating bonds into an investment portfolio is their ability to provide consistent income streams. Unlike stocks, which can experience significant price fluctuations, bonds typically offer fixed interest payments at predetermined intervals. This predictability makes them especially attractive for investors seeking steady cash flow, such as retirees or those approaching major financial milestones. Government and high-grade corporate bonds can generate annual yields ranging from 2% to 5%, providing a reliable supplement to other investment returns.

Key strategies for leveraging bonds in portfolio management include:

- Diversification: Spread investments across different bond types and sectors

- Income Generation: Create predictable cash flow through interest payments

- Risk Mitigation: Balance higher-risk investments with stable bond holdings

- Capital Preservation: Protect principal through low-risk bond selections

- Inflation Protection: Choose inflation-adjusted bonds to maintain purchasing power

Investors can optimize their bond strategy by carefully selecting instruments that align with their specific financial goals and risk tolerance. Some may prioritize higher-yield corporate bonds, while others might prefer the security of government Treasury bonds. The key is creating a balanced approach that provides both stability and potential growth. Younger investors might allocate a smaller percentage of their portfolio to bonds, while those approaching retirement could increase their bond allocation to reduce overall investment risk.

Pro Tip – Portfolio Balance: Regularly reassess your bond allocation, adjusting the percentage based on your age, financial goals, and changing market conditions.

Taxation, Costs, and Common Pitfalls

Investors must carefully navigate the complex landscape of bond investments, understanding the nuanced financial implications that extend beyond simple returns. Bond investment costs and tax considerations play a critical role in determining the actual profitability of these financial instruments, requiring meticulous analysis and strategic planning.

The tax treatment of bonds varies significantly depending on the type of bond and the investor’s specific financial circumstances. Municipal bonds often provide tax-exempt interest income, making them particularly attractive for investors in higher tax brackets. Conversely, corporate and Treasury bond interest is typically taxed as ordinary income at the federal level, and potentially at state and local levels as well. Understanding tax efficient investing can help investors minimize their overall tax liability and maximize net returns.

Common pitfalls in bond investing include:

- Transaction Costs: Brokerage fees and commissions that erode potential returns

- Inflation Risk: Potential for bond yields to be outpaced by inflation rates

- Interest Rate Sensitivity: Bond values fluctuating with market interest rate changes

- Reinvestment Risk: Challenges in finding comparable returns when bonds mature

- Credit Risk: Potential for issuer default or credit rating downgrades

Successful bond investing requires a comprehensive approach that goes beyond simple yield calculations. Investors must consider the total cost of ownership, including transaction fees, potential tax implications, and the impact of changing economic conditions. This holistic perspective allows for more informed decision-making, helping investors avoid common mistakes and optimize their fixed-income investment strategy.

Pro Tip – Tax Planning: Consult a tax professional to understand the specific tax implications of your bond investments and develop a strategy that minimizes your overall tax burden.

Secure Your Financial Future with Expert Bond Investment Guidance

Understanding how bonds balance growth and security is crucial for building a resilient investment portfolio. If you are looking to navigate complex risks like interest rate fluctuations, credit concerns, and tax implications discussed in this article, it is essential to have a clear strategy tailored to your goals. Whether you want to generate steady income or preserve capital, mastering the nuances of bonds can help you achieve peace of mind and financial stability.

Discover how bond basics and risk management can empower you to make informed choices that fit your unique situation. Don’t wait to optimize your portfolio with proven techniques explained at Finblog.com. Take action today by visiting our site and signing up for personalized consultations and educational resources designed to guide you through every step of your bond investing journey.

Frequently Asked Questions

What are the primary benefits of investing in bonds?

Investing in bonds provides a reliable income stream through fixed interest payments, portfolio stability, and lower risk compared to stocks, making them an attractive option for conservative investors.

How do interest rates affect bond prices?

Bond prices inversely correlate with interest rates; when interest rates rise, existing bond prices typically fall, and when rates decrease, bond prices generally rise.

What types of bonds should I consider for diversification?

For a well-diversified bond portfolio, consider including government bonds, corporate bonds, municipal bonds, and high-yield bonds to balance risk and optimize potential returns.

What risks should I be aware of when investing in bonds?

Key risks include credit risk ( issuer default), interest rate risk (price fluctuations due to rate changes), inflation risk (erosion of returns), and liquidity risk (difficulty selling before maturity). Investors should carefully assess these risks when choosing bonds.