Over 60 percent of Americans worry they will outlive their retirement savings. Planning for life after work matters more than ever as financial security in old age depends on the choices you make today. Understanding retirement accounts and their unique benefits can give you the structure and confidence needed for lasting peace of mind. This guide breaks down essential features, practical strategies, and helps you avoid costly pitfalls as you shape your financial future.

Table of Contents

- Retirement Accounts and Their Core Purpose

- Major Types of Retirement Accounts Explained

- Key Features and Tax Advantages Compared

- Contribution Limits, Withdrawals, and Rules

- Risks, Costs, and Common Mistakes to Avoid

Key Takeaways

| Point | Details |

|---|---|

| Purpose of Retirement Accounts | Designed to provide tax-advantaged savings and investment options for financial security in retirement. |

| Types of Accounts | Major types include Traditional IRA, Roth IRA, 401(k), and 403(b), each with distinct tax benefits and rules. |

| Contribution and Withdrawal Rules | Understanding annual limits and penalties for early withdrawals is vital for optimizing retirement savings. |

| Risks and Mistakes | Investors should be aware of market volatility, inflation, and common planning pitfalls to safeguard their retirement funds. |

Retirement Accounts and Their Core Purpose

Retirement accounts represent powerful financial instruments designed to help individuals systematically save and invest for their post-work years. According to FINRA, these accounts are “essential for long-term financial planning,” offering structured mechanisms to accumulate savings that will support individuals during retirement.

The primary objective of retirement accounts is to provide tax-advantaged methods for building financial security. As IRS documentation explains, these accounts offer critical tax incentives that encourage individuals to invest in their future financial stability. By allowing earnings to grow tax-deferred until withdrawal, retirement accounts create a compelling framework for wealth accumulation.

Key features of retirement accounts typically include:

- Tax-deferred or tax-free growth

- Potential employer matching contributions

- Structured investment options

- Flexibility in contribution levels

- Protection from immediate taxation

These accounts serve multiple strategic purposes beyond simple savings. They function as structured financial tools that help individuals:

- Reduce current taxable income

- Grow investments more efficiently

- Prepare for potential healthcare and living expenses in retirement

By understanding and leveraging retirement accounts, individuals can transform their long-term financial outlook and create a more secure future. Learn more about tax efficient investing to complement your retirement planning strategy.

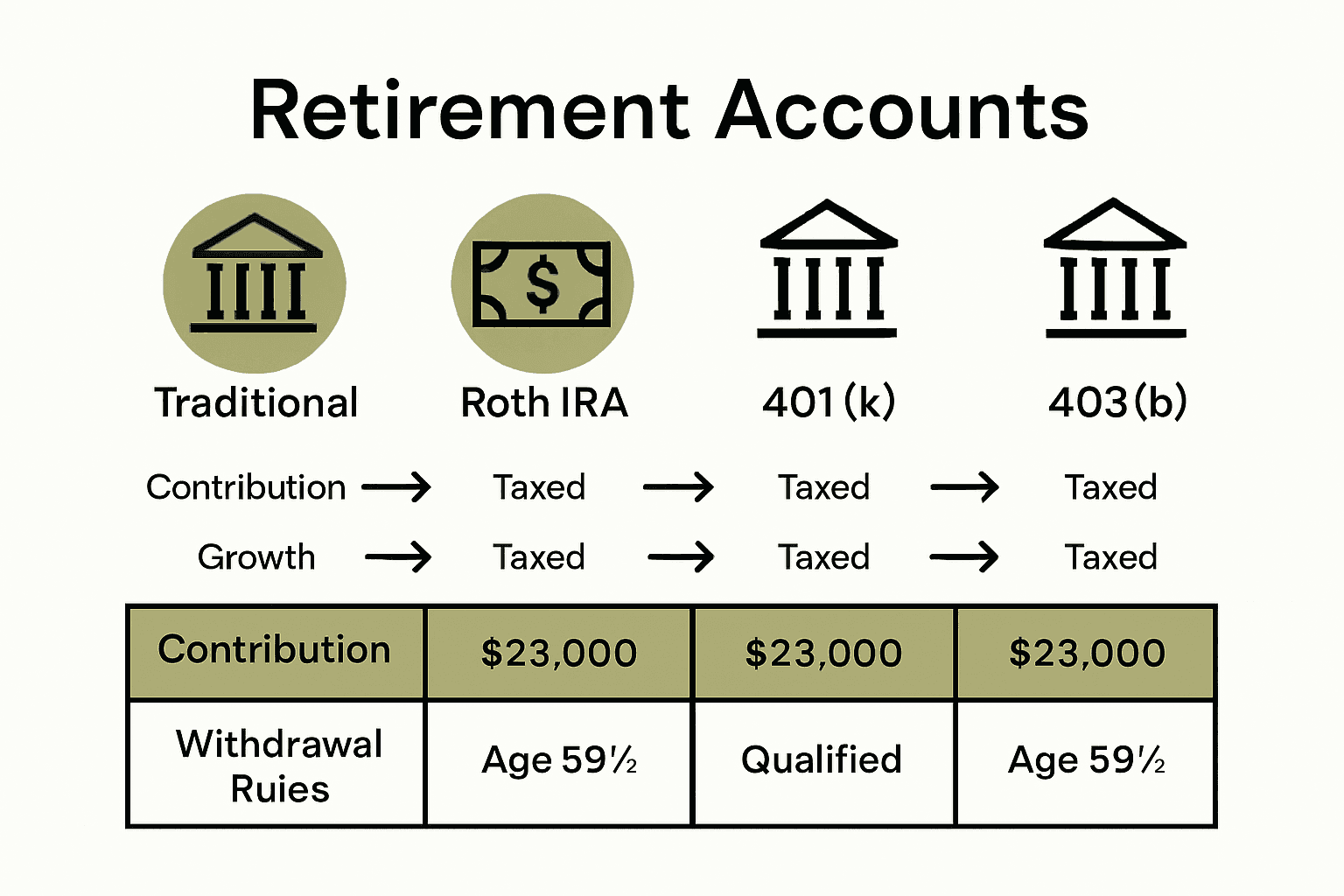

Major Types of Retirement Accounts Explained

Navigating the world of retirement accounts can feel complex, but understanding the major types is crucial for effective financial planning. According to FINRA, the primary types of retirement accounts include Individual Retirement Accounts (IRAs), 401(k) plans, and 403(b) plans, each offering unique features and tax implications.

NY MCU expands on these common retirement account options, highlighting the diversity of savings vehicles available to investors. These accounts are strategically designed to help individuals build long-term financial security through targeted tax advantages and structured savings mechanisms.

Key retirement account types include:

- Traditional IRA: Contributions may be tax-deductible, with taxes paid upon withdrawal

- Roth IRA: Contributions made with after-tax dollars, allowing tax-free withdrawals in retirement

- 401(k): Employer-sponsored plans with potential matching contributions

- 403(b): Similar to 401(k), typically offered by non-profit and educational institutions

- Solo 401(k): Designed for self-employed individuals and small business owners

Each retirement account type comes with specific eligibility requirements, contribution limits, and tax treatments. Understanding these nuances can help you optimize your retirement strategy.

Check out our retirement planning tips to further enhance your financial preparation for the future.

Check out our retirement planning tips to further enhance your financial preparation for the future.

Key Features and Tax Advantages Compared

Retirement accounts offer diverse tax strategies that can significantly impact long-term financial planning. According to Personal Finance, Traditional IRAs and Roth IRAs represent two distinct approaches to retirement savings, each with unique tax implications.

Traditional IRA tax advantages include:

- Tax-deductible contributions that reduce current taxable income

- Tax-deferred growth of investments

- Taxes paid upon withdrawal during retirement

Roth IRA tax advantages include:

- Contributions made with after-tax dollars

- Potential for completely tax-free withdrawals in retirement

- No required minimum distributions (RMDs) during the account holder’s lifetime

The key difference lies in the timing of tax benefits. Traditional IRAs provide immediate tax relief through deductible contributions, while Roth IRAs offer long-term tax advantages through tax-free growth and withdrawals. Income levels play a crucial role in determining eligibility and contribution limits for these accounts.

Understanding these nuanced tax strategies can help you optimize your retirement savings. For a deeper understanding of how taxes impact your investment strategy, explore our guide on tax implications of investing.

Contribution Limits, Withdrawals, and Rules

Retirement account management involves navigating complex regulations designed to encourage long-term savings. IRS guidelines establish strict annual contribution limits and withdrawal rules that investors must carefully understand to maximize their retirement strategies.

FINRA highlights critical rules regarding retirement account distributions, particularly emphasizing the importance of understanding potential penalties and age-related restrictions.

Key Contribution and Withdrawal Rules:

- Annual Contribution Limits: Vary by account type and change periodically

- Early Withdrawal Penalties: 10% additional tax for distributions before age 59½

- Required Minimum Distributions (RMDs): Mandatory withdrawals starting at age 72

Specific withdrawal regulations differ across retirement account types:

- Traditional IRA: Taxable withdrawals with 10% penalty before age 59½

- Roth IRA: Penalty-free withdrawals of contributions at any time

- 401(k): Typically stricter withdrawal rules with employer-specific restrictions

Understanding these nuanced rules is crucial for effective retirement planning. Explore our tax planning tips to help navigate these complex financial considerations and optimize your retirement strategy.

Risks, Costs, and Common Mistakes to Avoid

Retirement planning requires careful navigation of potential financial pitfalls. According to MICPA, investors must be aware of key retirement risks that can significantly impact long-term financial security, including market volatility, inflation, and longevity concerns.

NY MCU emphasizes the importance of understanding account fees and avoiding costly mistakes that can erode retirement savings.

Common Retirement Planning Risks:

- Market Volatility: Potential for investment value fluctuations

- Inflation: Erosion of purchasing power over time

- Healthcare Costs: Unexpected medical expenses

- Longevity Risk: Outliving your retirement savings

Top Mistakes to Avoid:

- Making early withdrawals with significant penalties

- Failing to diversify investment portfolio

- Underestimating healthcare and living expenses

- Ignoring tax implications of retirement accounts

- Not maximizing employer matching contributions

Proactive planning and continuous education are key to mitigating these risks. Learn from our guide on common retirement mistakes to develop a more robust financial strategy that protects your long-term financial health.

Secure Your Financial Future with Expert Retirement Account Guidance

Understanding retirement accounts can be overwhelming with all the rules, tax benefits, and types to consider. If you feel unsure about optimizing your 401(k), IRAs, or managing contribution limits and withdrawal penalties, you are not alone. Many face the challenge of navigating complex regulations while trying to avoid costly mistakes like early withdrawal penalties or missing out on employer matches. The article highlights the crucial importance of knowing these details to build long-term financial stability and avoid risks that can jeopardize your retirement goals.

Take charge of your retirement planning today by tapping into expert insights and practical strategies. At finblog.com, we offer tailored advice on tax planning tips and common retirement mistakes so you can confidently manage your retirement accounts and maximize your wealth. Don’t wait until it’s too late. Visit finblog.com now to access our trusted resources and start securing your financial future with clarity and confidence.

Frequently Asked Questions

What are the main types of retirement accounts?

The main types of retirement accounts include Traditional IRAs, Roth IRAs, 401(k) plans, and 403(b) plans. Each account type has unique features, eligibility requirements, and tax implications.

What are the benefits of using retirement accounts?

Retirement accounts offer tax-advantaged growth, potential employer matching contributions, and structured investment options, helping individuals save efficiently for their retirement while reducing taxable income.

What are the contribution limits and rules for retirement accounts?

Contribution limits vary by account type and change periodically. Key rules include a 10% penalty for early withdrawals before age 59½ and required minimum distributions (RMDs) starting at age 72 for certain accounts.

What are common mistakes to avoid when managing retirement accounts?

Common mistakes include making early withdrawals that incur penalties, failing to diversify your investment portfolio, underestimating healthcare costs, and ignoring tax implications associated with different retirement accounts.