Global markets turned cautious on Thursday as investors digested a mix of economic signals, corporate earnings, and political developments ahead of FED Chair Jerome Powell’s highly anticipated remarks at Jackson Hole on Friday.

Macro Signals: Inflation vs. Labor Weakness

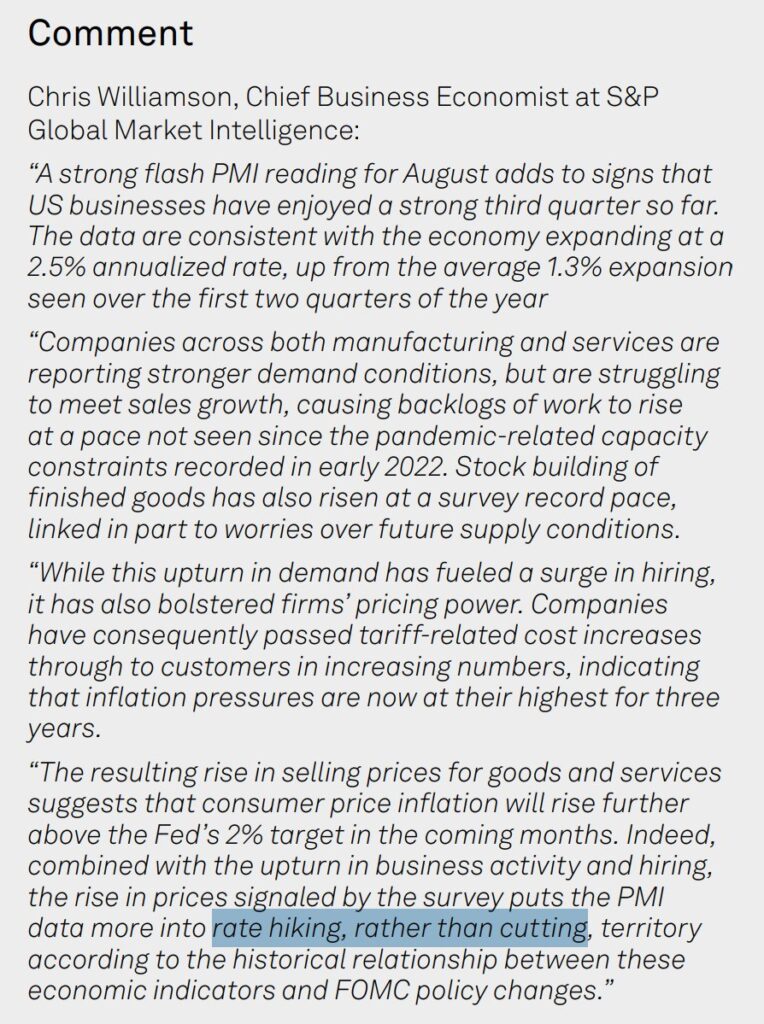

Fresh PMI data painted a picture of strong U.S. demand in August. According to S&P’s Chris Williamson, business activity is running at a 2.5% annualized rate, the fastest since early 2022, with firms reporting order backlogs and aggressive stockpiling of finished goods. However, this demand surge is also translating into higher prices as companies pass tariff-driven costs to consumers — pushing inflation pressures to three-year highs.

Williamson noted the data “puts the PMI more into rate hiking, rather than cutting, territory,” complicating the Fed’s balancing act.

Meanwhile, labor market signals were mixed. Weekly jobless claims rose to 235,000, the highest since June, while continuing claims ticked up to 1.97 million. The Philadelphia Fed index collapsed to -0.3 from 15.9, suggesting manufacturing activity is stalling.

Fed Speak: Divided Voices

Policymakers offered little clarity.

- Raphael Bostic (Atlanta Fed) reaffirmed his outlook for one rate cut in 2025 but stressed his forecast is “in flux” given labor weakness.

- Jeff Schmid (Kansas City Fed) warned upcoming jobs data will be “very consequential” and said inflation risks still outweigh labor softness.

- Beth Hammack (Cleveland Fed) and others signaled little urgency to cut, aligning with Fed minutes that showed a divided committee.

Adding to the intrigue, the DOJ has urged Powell to remove Governor Lisa Cook, citing mortgage-related allegations — a move that could tilt the board more toward Trump-aligned policymakers.

Corporate Spotlight: Walmart Disappoints

Walmart (-4.8%) became the session’s biggest drag after reporting Q2 earnings below expectations — its first miss since 2022. While U.S. sales growth topped forecasts at +4.6%, profits fell short due to tariff-related costs and one-time charges. The company raised its full-year sales outlook but flagged continued margin pressures as imported goods are replenished at higher post-tariff prices. Walmart CEO Doug McMillon recently stated, “Our costs are rising each week as we replenish inventory at post-tariff price levels. – We expect tariff-related costs to continue increasing into Q3 and Q4.”

Coty (-20%) also tumbled after forecasting a sharp U.S. sales slowdown, adding to fears of softer consumer demand.

Market Reaction

- Equities: The Dow fell 0.3%, S&P 500 -0.2%, and Nasdaq -0.2%, extending the week’s tech-led selloff.

- Bonds: Treasury yields climbed as traders priced in just a 79% chance of a September cut, down from nearly 100% last week.

- Commodities: Oil eased on chatter of a ceasefire opening Russian supply, while gold held firm on geopolitical hedging.

- Dollar: The U.S. currency remained steady despite political noise.

Looking Ahead

Markets are now laser-focused on Powell’s Jackson Hole address Friday at 10 a.m. ET. With inflation indicators running hot but labor market cracks widening, investors are desperate for clarity: Will the Fed validate September cut bets — or signal a longer wait?

As one strategist put it: “Anything short of Powell signaling a cut could trigger a deeper pullback, especially with valuations stretched and August liquidity thin.”

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related:

Morning Bid: Jackson Hole Opens Under Trump’s Shadow