Most american households have never created a personal balance sheet, even though experts say this tool offers a clear view of your true financial health. With so many spending decisions and financial obligations, understanding what you own versus what you owe becomes critical for making smarter money choices. A personal balance sheet brings order to chaos and helps you track your progress toward goals, offering a practical method to assess your net worth at any moment.

Table of Contents

- Defining A Personal Balance Sheet Example

- Core Components And Layout Explained

- How To Create Your Own Balance Sheet

- Common Use Cases For Individuals

- Mistakes To Avoid When Building One

Key Takeaways

| Point | Details |

|---|---|

| Personal Balance Sheet Overview | A personal balance sheet captures an individual’s financial landscape, including assets, liabilities, and net worth, serving as a financial roadmap. |

| Components of a Balance Sheet | It includes current and non-current assets and liabilities, providing a clear view of financial health. |

| Importance of Regular Updates | Regularly updating your balance sheet is crucial to accurately assess financial standing and make informed decisions. |

| Common Mistakes | Avoid misvaluing assets and underreporting liabilities to maintain a reliable financial overview. |

Defining a Personal Balance Sheet Example

A personal balance sheet represents a comprehensive financial snapshot that captures your entire monetary landscape at a specific moment in time. According to Virginia Tech Pubs, it provides a detailed accounting of your assets, liabilities, and net worth, offering a clear picture of your financial health.

At its core, a personal balance sheet functions like a financial roadmap, revealing where your money is allocated and your overall economic standing. As Cambridge University explains, this document lists all personal assets and liabilities, creating a transparent overview of an individual’s financial position at a precise moment.

The typical personal balance sheet includes three fundamental components:

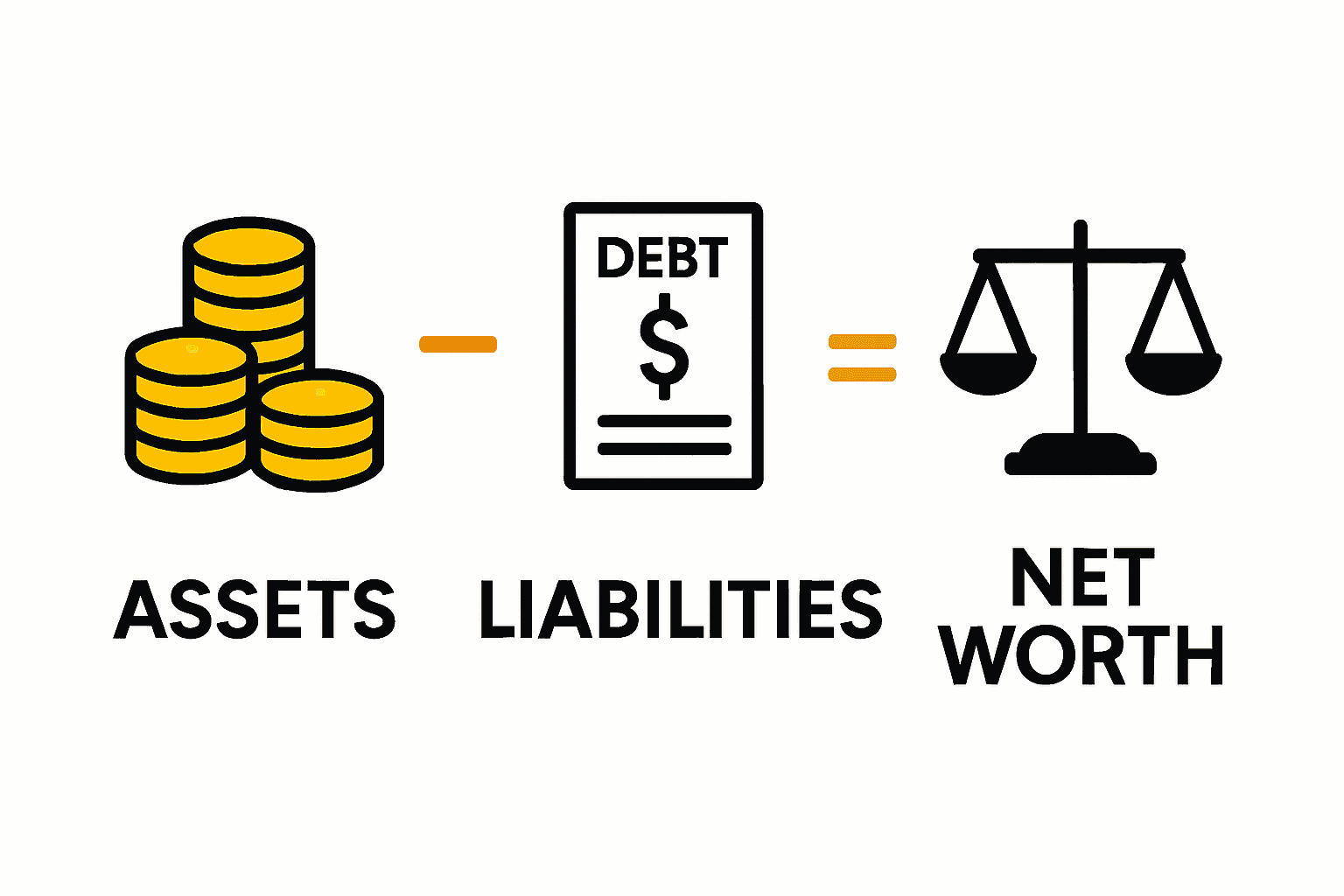

- Assets: Everything you own with monetary value

- Liabilities: All financial obligations and debts

- Net Worth: The difference between your total assets and total liabilities

Think of a personal balance sheet as your financial report card. It doesn’t just show numbers; it tells a story about your financial decisions, spending habits, and potential for future wealth accumulation. By tracking these elements regularly, you gain powerful insights into your financial trajectory and can make more informed monetary choices.

Core Components and Layout Explained

A comprehensive personal balance sheet breaks down into three critical financial categories: assets, liabilities, and net worth. According to GeeksForGeeks, these components are typically divided into current and non-current classifications, providing a granular view of an individual’s financial landscape.

Assets represent everything of monetary value that you own, which can be further categorized into two primary types:

- Current Assets: Cash, checking/savings accounts, investments you can quickly convert to cash

- Non-Current Assets: Real estate, retirement accounts, long-term investments, valuable personal property

On the opposite side of the balance sheet, liabilities capture your financial obligations. These are similarly categorized into current and non-current segments. University of Minnesota Extension highlights that traditional balance sheet layouts place assets on the left side and liabilities on the right, with net worth balanced at the bottom.

Liabilities typically include:

- Current Liabilities: Credit card balances, short-term loans, upcoming bill payments

- Non-Current Liabilities: Mortgage, student loans, long-term financing arrangements

The final component, net worth, represents your true financial standing. It’s calculated by subtracting total liabilities from total assets. A positive net worth indicates financial health, while a negative net worth suggests you owe more than you own. This simple yet powerful calculation provides immediate insight into your overall financial condition.

How to Create Your Own Balance Sheet

Creating a personal balance sheet requires careful organization and thorough financial inventory. According to Dominican University, the fundamental process involves listing all assets and liabilities, then subtracting total liabilities from total assets to determine your net worth.

Gathering Financial Information

To start your balance sheet, you’ll need to collect comprehensive financial documentation:

- Bank statements

- Investment account records

- Mortgage and loan documents

- Credit card statements

- Retirement account summaries

- Vehicle and property ownership documents

Calculating Your Assets

Begin by itemizing all current and non-current assets. This includes:

- Cash in checking and savings accounts

- Investment portfolio values

- Real estate property values

- Vehicle market values

- Retirement account balances

- Valuable personal property

Recording Your Liabilities

Next, document all financial obligations, categorizing them as current or non-current:

- Credit card balances

- Personal loans

- Student loan debt

- Mortgage outstanding balance

- Car loan remaining balance

- Any other outstanding financial commitments

For those seeking additional support, University of Illinois FarmDoc recommends utilizing specialized financial tools that can help streamline the balance sheet preparation process. These digital resources can simplify complex calculations and provide a structured approach to tracking your financial position.

The final step involves calculating your net worth by subtracting total liabilities from total assets.

This simple yet powerful calculation offers immediate insight into your overall financial health, helping you understand your current economic standing and identify areas for potential improvement.

This simple yet powerful calculation offers immediate insight into your overall financial health, helping you understand your current economic standing and identify areas for potential improvement.

Common Use Cases for Individuals

Personal balance sheets serve multiple critical financial planning purposes for individuals across different life stages. Virginia Tech Publications highlights that regularly creating these documents helps individuals monitor financial health, track progress toward goals, and make informed financial decisions.

Financial Planning and Goal Setting

Individuals use personal balance sheets as strategic tools for comprehensive financial planning. These documents enable precise tracking of financial progress and help establish realistic monetary objectives. Key planning use cases include:

- Retirement Preparation: Assessing current savings and projecting future needs

- Debt Management: Understanding total debt load and creating reduction strategies

- Investment Allocation: Evaluating current asset distribution and potential rebalancing

Major Life Transitions

Balance sheets become especially valuable during significant life changes. According to Cambridge University, these documents help individuals assess financial stability and evaluate the impact of major decisions. Critical transition scenarios include:

- Getting married

- Purchasing a home

- Career changes

- Starting a family

- Planning for children’s education

- Preparing for potential inheritance

Risk Assessment and Financial Health

A personal balance sheet acts like a financial health check, providing immediate insights into your economic resilience. By comparing assets and liabilities, you can:

- Determine your net worth

- Identify potential financial vulnerabilities

- Understand your liquidity position

- Track wealth accumulation over time

- Prepare for unexpected financial challenges

Think of your balance sheet as a personal financial dashboard. It’s not just a static document, but a dynamic tool that evolves with your financial journey, helping you make smarter, more informed decisions about your money.

Mistakes to Avoid When Building One

Creating an accurate personal balance sheet requires meticulous attention to detail and strategic financial assessment. Virginia Tech Publications warns against common pitfalls such as overestimating asset values, underestimating liabilities, and neglecting to update the balance sheet regularly.

Valuation Errors

One of the most critical mistakes individuals make involves improper asset valuation. These errors can significantly distort your financial picture:

- Outdated Property Values: Using old real estate or vehicle appraisals

- Unrealistic Investment Assessments: Failing to adjust investment portfolio values

- Emotional Asset Pricing: Overvaluing personal property based on sentimental attachment

Incomplete Financial Reporting

According to Cambridge University, ensuring accuracy means including all assets and liabilities with current values. Common omission mistakes include:

- Forgetting about small investment accounts

- Overlooking personal loans to friends or family

- Ignoring potential tax liabilities

- Leaving out retirement account contributions

- Neglecting insurance policies with cash value

Frequency and Maintenance Errors

A balance sheet is not a one-time document but a dynamic financial tool. Critical maintenance mistakes include:

- Infrequent Updates: Allowing years to pass without revision

- Inconsistent Tracking: Using different valuation methods each time

- Ignoring Life Changes: Not adjusting after major financial events

Think of your balance sheet like a car. Regular maintenance prevents unexpected breakdowns. An annual review can reveal financial blind spots, help you course-correct, and provide a clear snapshot of your economic health.

Take Control of Your Financial Future with a Personal Balance Sheet

Understanding your personal balance sheet is essential for clear financial planning and achieving your goals such as retirement preparation or debt management. If you find yourself overwhelmed by asset valuation, tracking liabilities, or updating your financial snapshot regularly you are not alone. Many struggle with building an accurate balance sheet that truly reflects their net worth and financial health.

At finblog.com, we help you simplify this process with expert guidance and tools designed to keep your finances organized and up to date. Stop guessing your financial standing and start making informed decisions based on precise data. Visit finblog.com today to get personalized insights and resources that empower you to monitor your assets and liabilities effectively. Take the first step toward stronger financial health and better wealth management now.

Frequently Asked Questions

What is a personal balance sheet?

A personal balance sheet is a financial document that provides a snapshot of an individual’s assets, liabilities, and net worth at a specific point in time. It helps to assess overall financial health.

How do I create my own personal balance sheet?

To create a personal balance sheet, gather financial information such as bank statements, investment records, and loan documents. Then, list your assets and liabilities, categorize them, and calculate your net worth by subtracting total liabilities from total assets.

What are the key components of a personal balance sheet?

The key components of a personal balance sheet include assets (everything you own with monetary value), liabilities (all debts and financial obligations), and net worth (the difference between total assets and total liabilities).

Why is it important to maintain a personal balance sheet?

Maintaining a personal balance sheet is important because it helps you monitor your financial health, track your progress towards financial goals, and make informed financial decisions. Regular updates can also reveal changes in your financial situation and help you address potential vulnerabilities.