NVIDIA is set to report quarterly results after the US market close on Wednesday, February 25, 2026, with numbers expected around 4:20 pm ET and the conference call at 5:00 pm ET. For investors in Baku, that means the release lands in the early hours of Thursday.

This is not just another earnings report. Nvidia has become the central barometer of global AI demand, and at a time when markets are debating whether the AI investment surge is sustainable or inflated, this print carries unusual weight.

Shares have been trading below their late October highs, as some investors question whether AI enthusiasm has run too far, too fast. The company remains one of the most valuable in the world, but sentiment has cooled compared to the peak excitement of 2025.

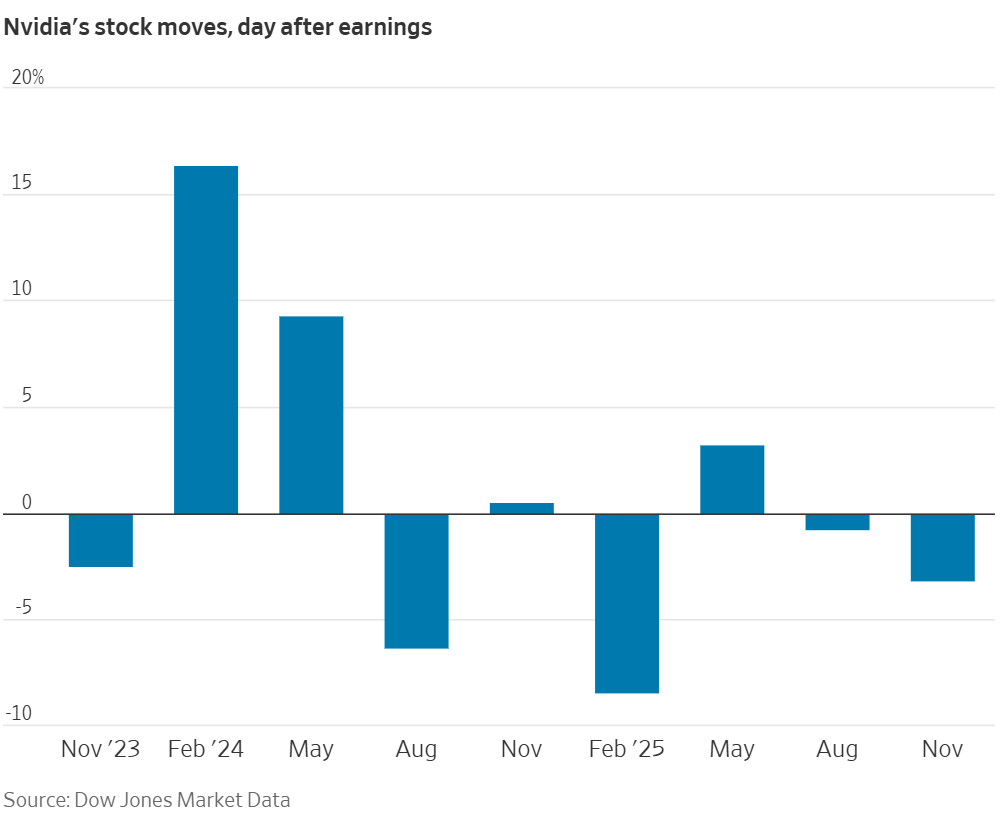

What Traders Expect After Earnings

Options markets suggest investors are bracing for a meaningful move.

Current pricing implies Nvidia stock could swing about 5% to 6% in either direction by the end of the week. From a pre-earnings level around $190 to $196, that points to a potential range near:

- $207 on the upside

- $185 on the downside

Interestingly, this is one of the smallest implied earnings moves in several years, suggesting traders expect volatility but not chaos.

It is important to remember that this is not a prediction. It simply reflects how much movement the market is pricing in based on option costs.

Wall Street’s Expectations: The Bar Is Extremely High

Analysts broadly expect another record quarter.

Consensus estimates cluster around:

- Revenue near $65.6 billion to $66.2 billion

- Adjusted earnings per share around $1.52 to $1.54

- Year over year revenue growth near 67% to 70%

- Gross margin around 75%

That would represent massive growth for a company already generating tens of billions per quarter.

The challenge is not whether Nvidia will post strong numbers. The challenge is whether those numbers will be strong enough to exceed already elevated expectations.

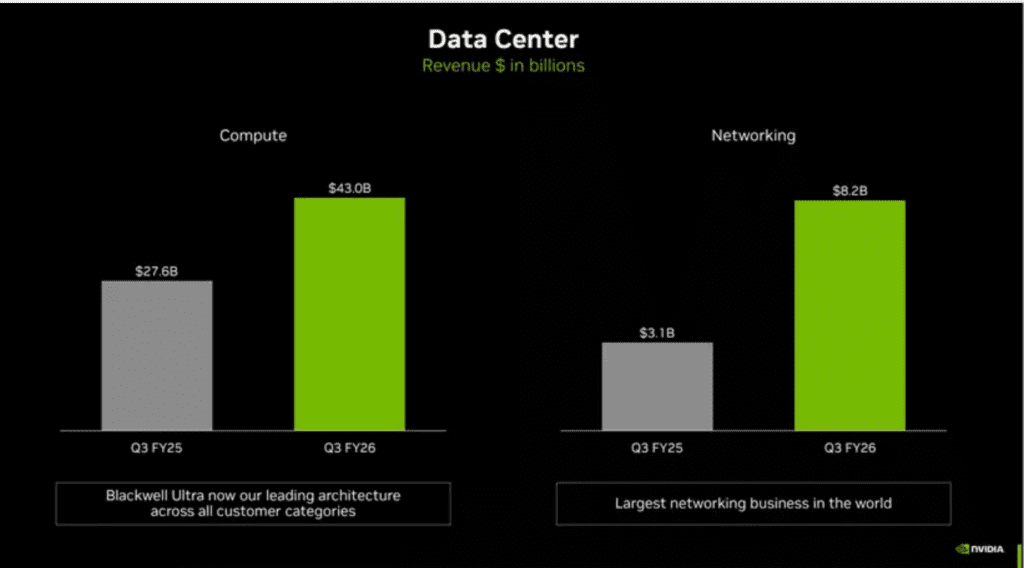

Data Center Remains the Core Story

The heart of Nvidia’s business is now its Data Center segment, which has transformed the company from a gaming chip maker into the backbone of AI infrastructure.

Last quarter:

- Total revenue was $57 billion

- Data Center revenue was $51.2 billion

For this report, analysts expect Data Center revenue to be around $61 billion, up roughly 70% year over year.

This division reflects spending from major cloud and tech companies such as Alphabet, Amazon, Meta and Microsoft, all of which are pouring billions into AI infrastructure.

Investors will be listening closely to see whether that spending momentum remains strong.

What Matters Most on the Conference Call

The numbers are important. But the guidance and tone may matter even more.

1. Blackwell Chip Ramp

NVIDIA’s next-generation platform, Blackwell, is expected to power the next phase of AI expansion. Investors want clarity on: Production ramp speed, Shipment volumes, Order visibility

If management suggests demand remains broad and supply is improving, that could support the stock.

2. Margins

Margins are a key indicator of pricing power.

Nvidia previously reported gross margins in the low 70% range and guided toward mid 70%. If margins stay near or above 75%, it signals that rising production complexity is not hurting profitability.

Any margin weakness could spark concern.

3. Supply Constraints

Some analysts argue that supply chain bottlenecks, especially around advanced manufacturing capacity, could limit upside even if demand remains strong.

Investors will look for updates on capacity and delivery timelines.

China and Geopolitics

China remains a major variable.

US export controls have reshaped Nvidia’s access to the Chinese market. While certain chip sales have received conditional approval, shipments are subject to strict rules.

There are also political tensions around enforcement and technology restrictions. Any commentary on: China revenue potential, Regulatory clarity, Export approvals could move the stock sharply.

Even if China revenue is not included in this quarter’s results, guidance about future sales can influence sentiment.

Why This Moves the Entire Market

Nvidia’s weight in the S&P 500 is so large that even a mid single digit move can affect the broader index.

If Nvidia jumps 6%, it can lift tech stocks and boost overall market sentiment.

If it drops sharply, it can drag down AI related names across semiconductors, software and infrastructure.

This report will likely influence: The broader AI trade, Semiconductor stocks, Major indices, Risk appetite heading into March

The Real Question

The key issue is no longer whether Nvidia is growing.

It is whether AI spending is still accelerating or beginning to normalise. If Nvidia delivers strong results and confident guidance, it could reignite enthusiasm around the AI boom.

If guidance is cautious, even slightly, markets may interpret it as the first sign that the AI investment wave is slowing.

Wednesday’s report is not just about earnings. It is a test of the AI narrative itself.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.