India’s strong economic momentum is facing new risks as the conflict involving Iran, the US, and Israel threatens to push energy prices higher and disrupt key trade links.

India’s $3.8 trillion economy, which has recently been benefiting from strong growth and relatively low inflation, could face significant pressure if the Middle East conflict drags on.

Analysts warn that higher oil prices, weaker worker remittances, and disruptions to trade and shipping routes could affect India’s economic outlook.

Oil Prices a Major Risk

India is particularly sensitive to energy shocks because of its heavy reliance on imported oil.

The Middle East currently provides:

• 55% of India’s crude oil imports

• 17% of its exports

• 38% of worker remittances

Following the latest military strikes, oil prices jumped about 8%, with Brent crude briefly rising above $82 per barrel. Some analysts warn prices could climb toward $100 per barrel if the conflict escalates.

Every $10 increase in oil prices could:

• Widen India’s current account deficit

• Push inflation higher

• Reduce economic growth

Trade and Shipping Risks

Another concern is the Strait of Hormuz, a critical shipping route through which about one third of global seaborne crude oil passes.

Any disruption there could significantly affect energy supplies to major Asian economies including India, China, Japan, and South Korea.

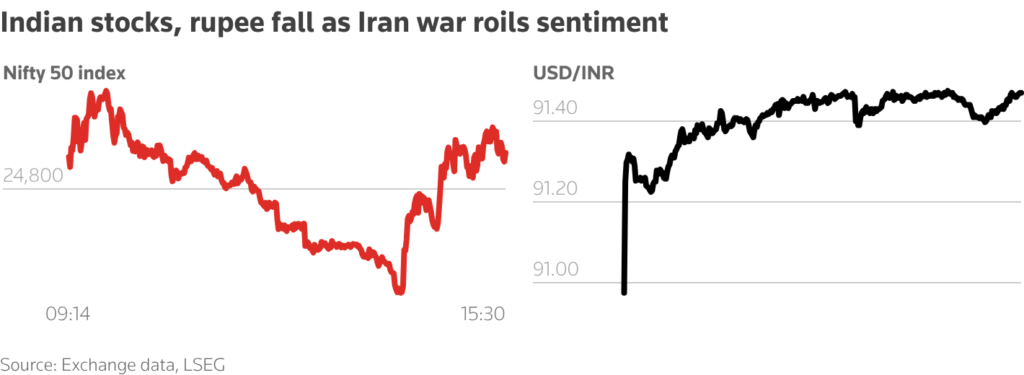

Financial markets have already reacted to these risks, with Indian stocks and the rupee falling while bond yields rose.

Remittances and Business Exposure

India could also be affected through its large workforce in the Middle East.

Around 10 million Indian workers are employed in the region, sending billions of dollars home each year. A slowdown in Gulf economies could reduce these remittance flows.

Several major Indian companies also have strong business ties to the region. Engineering firm Larsen & Toubro, for example, receives nearly 40% of its infrastructure orders from Middle Eastern projects.

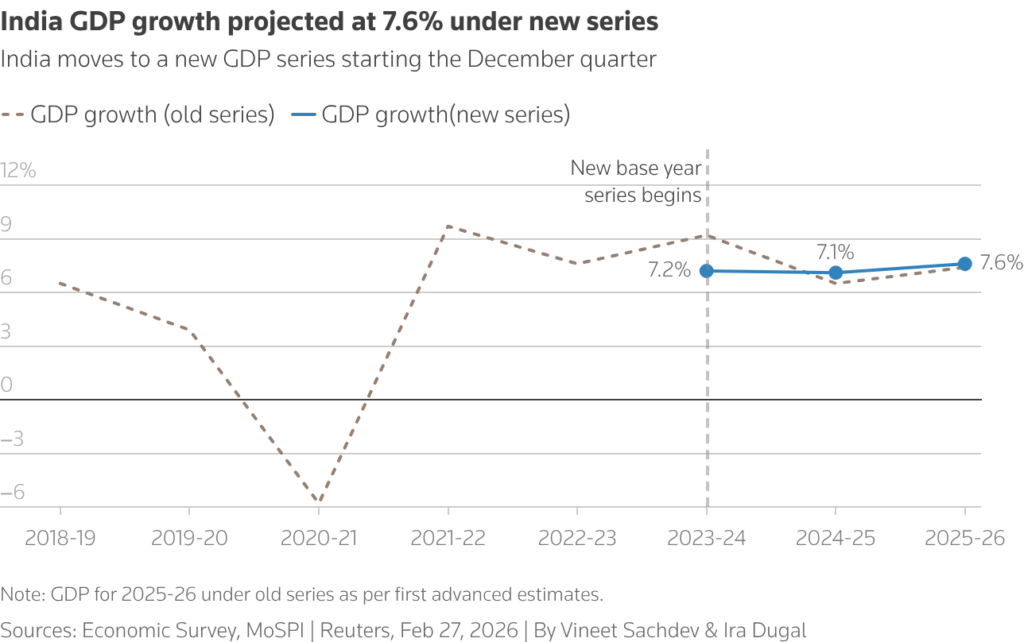

Strong Growth Still Expected

Despite these risks, India’s economy remains one of the fastest growing in the world.

Recent government data shows the economy expanding 7.8% in the October–December quarter, with growth projected at around 7.6% for the current financial year.

However, economists say the trajectory could change quickly if the Middle East conflict continues to push energy prices and geopolitical uncertainty higher.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.