If you watched gold rocket past $5,600 an ounce this week and then collapse toward $4,900 almost overnight, you are probably asking the same question as everyone else:

Did we just witness the top, or was this only a brutal reset before another leg higher?

The answer is not simple. But the wild price action is telling us a lot about how investors are thinking right now and why gold has suddenly become one of the most emotional trades in global markets.

More about: Gold and Silver Crashed. Here’s What Really Happened and Why It Matters

Why many investors are suddenly cautious

For some analysts, this was the moment gold crossed from a structural rally into speculative territory.

Several fund managers told Barron’s that the easy money may already have been made. Scott Tiras of Tiras Wealth Management summed it up bluntly: early gold rallies are often driven by fundamentals, but late-stage surges are increasingly driven by sentiment. And sentiment can reverse fast.

Eric Parnell of GVA put it another way. Gold might still rise, but after such an extraordinary run, waiting for a deeper pullback could be the smarter move.

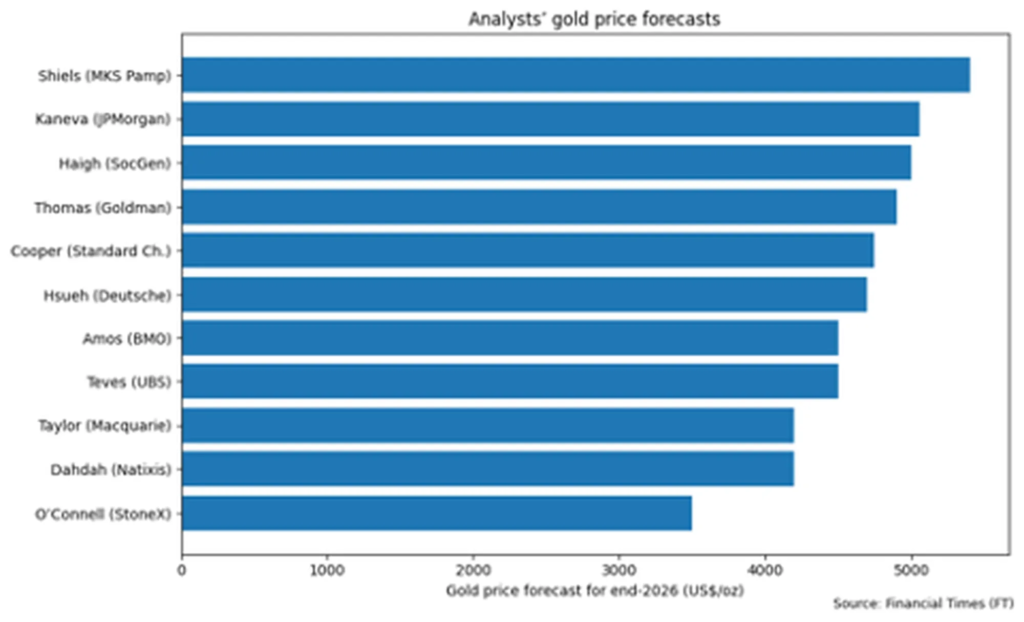

That caution shows up clearly in forecasts. A recent Financial Times survey of strategists put the average 2026 year-end gold target at $4,600, well below current levels. Macquarie’s Peter Taylor went further, warning that gold’s path is now being shaped as much by speculation as fundamentals, with prices potentially slipping toward $4,200 by late 2026.

In other words, even after the crash, many analysts think gold may still be overpriced.

But the bull case refuses to die

And yet, gold’s supporters are not backing down.

They argue that this was not the end of the story, but a violent shakeout. Central banks are still buying gold to diversify away from the dollar. Government debt continues to rise. Trade tensions remain unresolved. And expectations for US rate cuts later this year are very much alive.

Ben McMillan of IDX framed it in stark terms. Since the pandemic, an enormous share of US dollars in existence has been created. That monetary expansion, he argues, is a long-term tailwind for gold, not a temporary one.

Others point to geopolitics. Sanctions, fractured trade relationships, and de-dollarisation have changed how countries think about reserves. Gold, unlike bonds or currencies, is not tied to anyone else’s balance sheet.

James Luke of Schroders believes gold’s true peak will only come when either geopolitical tensions ease meaningfully, or demand becomes clearly exhausted. In his view, neither has happened yet.

So where does that leave investors?

The truth sits uncomfortably in the middle.

Gold is no longer just reacting to inflation or central bank buying. It is reacting to positioning, leverage, and emotion. That makes it more powerful on the way up and more dangerous on the way down.

The past week showed how quickly a “safe haven” can behave like a momentum trade once liquidity dries up. If central banks slow purchases, if the dollar strengthens, or if political risk eases even slightly, gold’s speculative premium could unwind just as fast as it appeared.

At the same time, the forces that drove gold higher have not disappeared. Debt is still rising. Rate cuts are still expected. Geopolitical risks are still real.

So is it too late to invest in gold in 2026?

For investors chasing fast gains, possibly. For those looking to hedge uncertainty and currency risk over the long term, gold still has a role. But the events of this week delivered a clear message: this is no longer a calm, defensive trade. It is a volatile one.

Gold’s history as a store of value stretches back thousands of years. But in today’s markets, timing and discipline matter more than ever.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.