Every few weeks, the same idea resurfaces on social media: Europe could hit Washington where it hurts by dumping US Treasury bonds and choking off US funding. It sounds dramatic. It sounds powerful. And according to market insiders, it is almost entirely unrealistic.

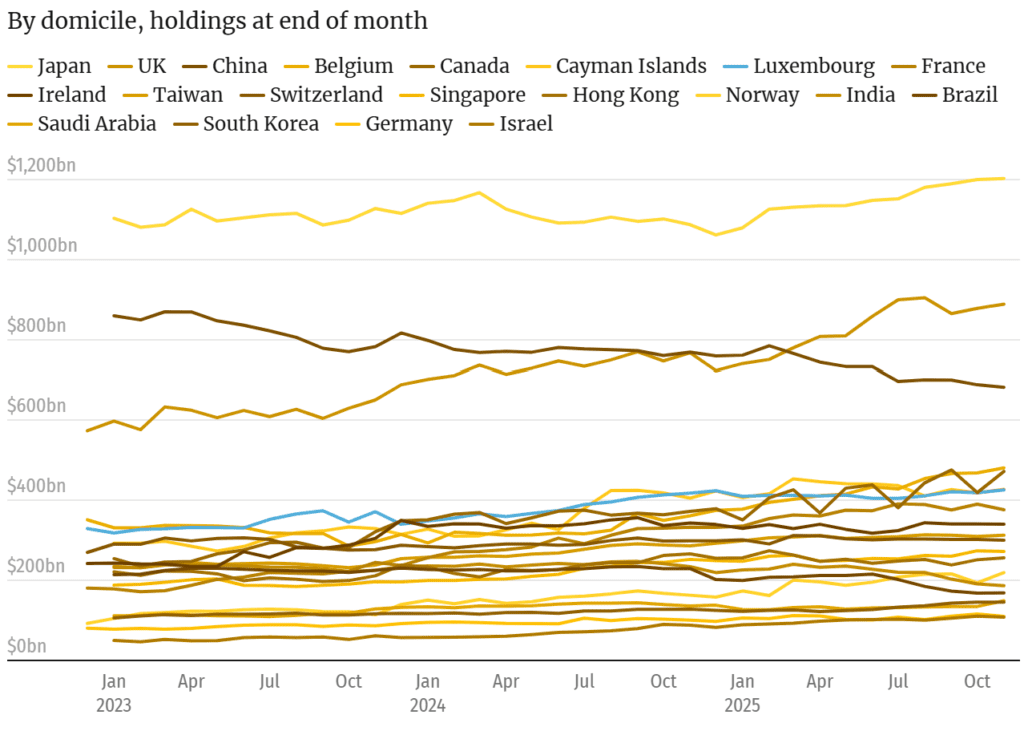

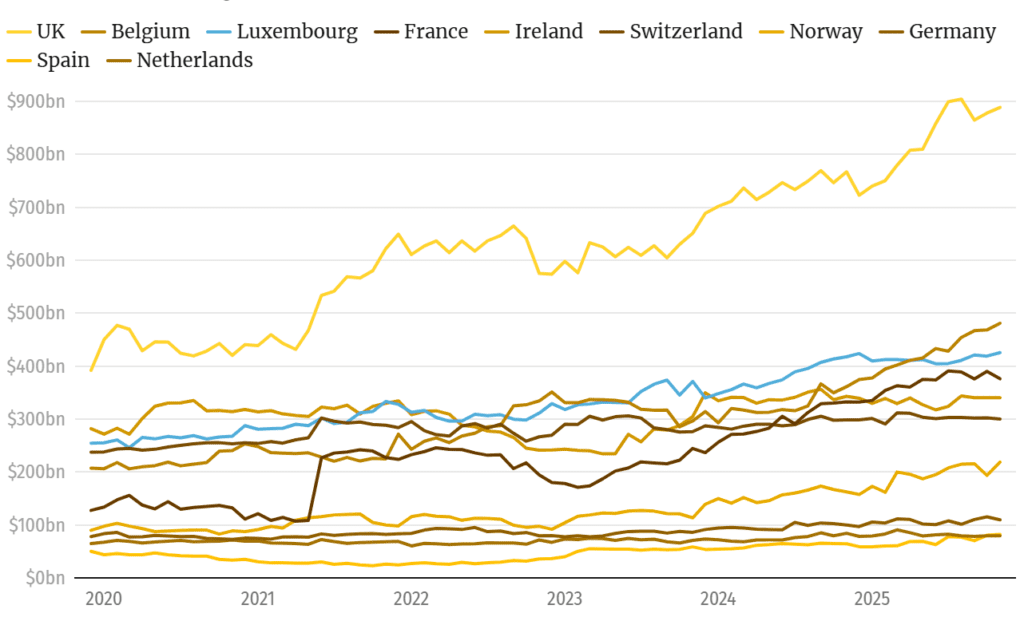

The theory gained momentum in January as tensions flared around Donald Trump’s comments on Greenland and trade. Since foreign investors hold roughly one-third of America’s $37 trillion-plus government debt, some argued Europe could coordinate a sell-off, crash the dollar, and force a policy rethink in Washington.

In practice, markets simply do not work that way.

There is no “Europe trade button”

European holders of US Treasuries are not a single bloc. They include pension funds, insurers, asset managers, hedge funds, and global custodians, many of whom are trading against each other every day.

“Collective retaliation is a social media fantasy,” said Rebecca Christie, senior fellow at Bruegel. Investors are too diverse, too competitive, and too globally spread to suddenly act in unison.

Some selling is happening, but not for political reasons

Yes, a few European investors have reduced exposure to US bonds. Luxembourg-based Pure Capital cut its Treasury holdings late last year, shifting part of its portfolio into German bunds. The reason was not geopolitics, but risk management.

“The dollar didn’t hedge volatility the way investors expected,” said portfolio manager Jean-Philippe Vanderborght. When the source of volatility becomes US policy itself, investors naturally rethink their hedges.

That is portfolio strategy, not punishment.

Custody data distorts the story

Another misconception comes from Treasury ownership statistics. Large holdings reported in Luxembourg or Belgium often sit there because of custodians like Clearstream and Euroclear. The real owners may be in Asia, the Middle East, or elsewhere.

On paper, it looks European. In reality, it is global.

Big money is not going to rage-sell

Large institutions are unlikely to dump US assets out of political frustration. “I don’t see governments issuing directives telling investors to sell US bonds,” said Paul Jackson, global market strategist at Invesco. Institutional investors, he added, are run professionally, not emotionally.

Individual funds may shift allocations, but the market impact is close to zero compared with the scale of global capital flows.

So what actually changes? Slowly, not suddenly

Some northern European pension funds have trimmed Treasury exposure, and geopolitical risk is increasingly part of allocation discussions. Over time, this could mean gradual diversification into assets like gold, German bunds, or even China-linked markets.

But a coordinated European bond dump designed to hurt the US? Markets say that belongs to Twitter, not reality.

Europe can rebalance. It cannot pull the plug.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Main resource: Coordinated European sell‑off of US bonds is ‘social media fantasy’

Related: Trump’s Greenland tariffs: What’s Europe’s ‘trade bazooka’ option to hit back?