TL;DR:

- Estate planning involves key legal documents that ensure your assets and family are cared for if you become unable to make decisions. Properly funding, updating, and communicating with your fiduciaries are essential to avoid delays and legal issues. Regular reviews and organized records help ensure your plan is effective and aligned with your life changes.

Estate planning essentials are the core documents and actions that determine what happens to your assets, your health, and your family when you can no longer make decisions yourself. A complete plan requires at least five to six legal documents, including a will, a revocable living trust, powers of attorney, and healthcare directives. Without these in place, courts decide who gets your property, who raises your children, and who speaks for you in a medical crisis. Getting this right is not complicated, but it does require knowing exactly what to prepare and in what order.

What are the key estate planning documents you must have?

A fundamental estate plan requires five to six core documents. Each one covers a different gap that the others cannot fill on their own.

- Last will and testament. A will directs how your property is distributed after death and names a guardian for minor children. Without one, state intestacy laws decide both, and the court’s choice may not match yours.

- Revocable living trust. A living trust holds your assets during your lifetime and transfers them to beneficiaries without going through probate. This saves your family months of court delays and keeps the details of your estate private.

- Pour-over will. This document works alongside a trust. Any asset you forgot to transfer into the trust during your lifetime gets “poured over” into it at death, so nothing falls through the cracks.

- Durable financial power of attorney. This grants a trusted person the legal authority to manage your bank accounts, pay bills, and handle financial transactions if you become incapacitated. Without it, your family may need a court-ordered conservatorship, which is expensive and slow.

- Healthcare power of attorney. This names a healthcare proxy to make medical decisions on your behalf when you cannot. The proxy’s authority is only as good as the instructions you give them.

- Advance healthcare directive. Also called a living will, this document spells out your specific wishes for life-sustaining treatment, resuscitation, and end-of-life care. It removes the burden of guessing from your family during the worst moments.

- HIPAA authorization. This allows named individuals to access your medical records. Without it, even a spouse can be legally blocked from getting information from your doctors.

Powers of attorney carry significant weight. They can grant authority to move assets or make gifts, so appointing trusted individuals is non-negotiable. In high-risk situations, naming two agents who must act jointly adds a layer of protection against misuse.

One document that families often overlook is the Certificate of Trust. A Certificate of Trust proves a trust exists and confirms the trustee’s authority without revealing the private details of the trust itself. Banks and title companies require this when you transfer accounts or property into the trust’s name. Having it ready speeds up every transaction.

How to prepare your asset and beneficiary information

Preparation before you meet an estate planning attorney cuts consultation time and reduces costs. Attorneys who receive organized client information can focus on legal strategy rather than basic fact-finding. Gathering a comprehensive asset list before your first meeting can reduce that initial consultation to 30–60 minutes.

Compile the following before any attorney meeting:

- Real estate. List every property you own, including the address, how title is held, and any outstanding mortgage balance.

- Bank and investment accounts. Include account numbers, institutions, and current approximate balances.

- Retirement accounts. Note the account type (IRA, 401(k), Roth IRA), the institution, and the current beneficiary designations on file.

- Life insurance policies. Record the insurer, policy number, death benefit amount, and named beneficiaries.

- Business interests. If you own a business or partnership stake, document the entity type, your ownership percentage, and any buy-sell agreements.

- Vehicles and personal property. List vehicles, boats, and any high-value collectibles or artwork.

- Debts and obligations. Include mortgages, car loans, credit card balances, and any personal loans.

- Beneficiary contact information. Collect full legal names, addresses, and Social Security numbers for everyone you plan to name.

This list does more than save time. It forces you to see your full financial picture in one place, which often reveals gaps, like an old 401(k) from a previous employer with an ex-spouse still listed as beneficiary.

Pro Tip: Store your asset inventory in a secure, accessible location and tell your executor exactly where to find it. A binder or encrypted digital file works well. Your family should not be hunting for account numbers during a crisis.

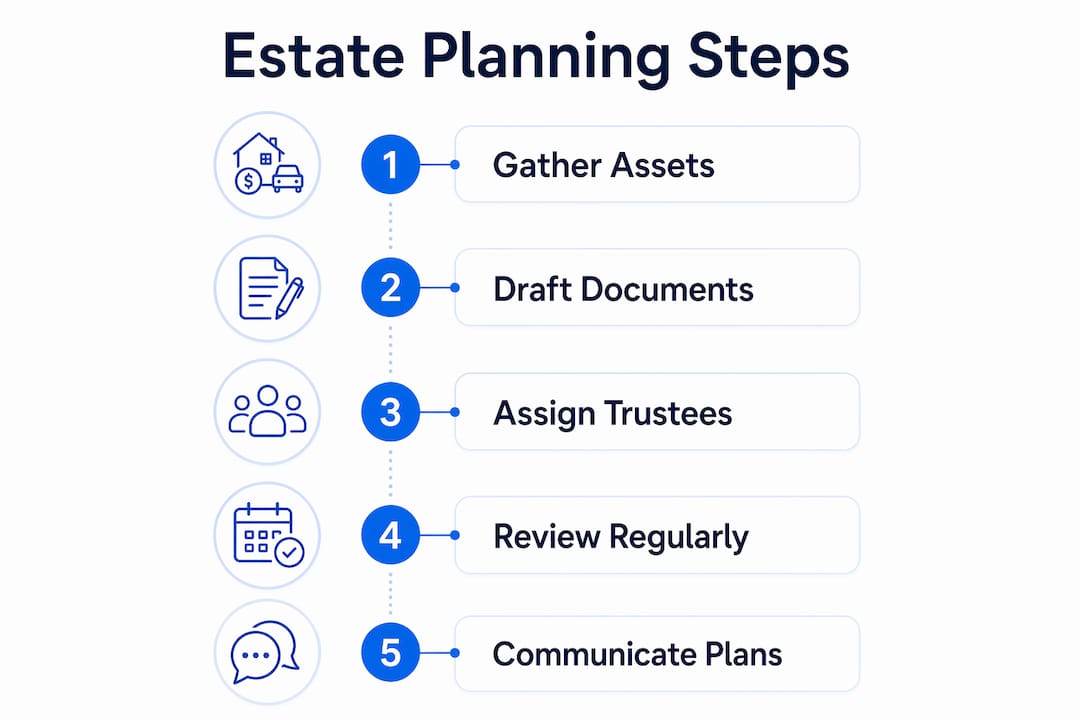

What steps create or update an effective estate plan?

Building or revising an estate plan follows a clear sequence. Skipping steps creates the exact problems the plan is supposed to prevent.

-

Choose your fiduciaries. Select an executor for your will, a trustee for your trust, agents for your financial and healthcare powers of attorney, and a guardian for any minor children. These roles require people who are organized, trustworthy, and willing to serve. Confirm their willingness before naming them in any document.

-

Draft your documents with an attorney. Work with an estate planning attorney to prepare all five to six core documents. Online templates exist, but they frequently miss state-specific requirements and can be invalidated for technical reasons.

-

Fund your trust. A trust that holds no assets does nothing. Transfer real estate by recording a new deed in the trust’s name. Move bank and investment accounts by updating the account title at each institution. This step is where most families stall, and an unfunded trust is one of the most common estate planning failures.

-

Align your beneficiary designations. Beneficiary designations override wills. A retirement account or life insurance policy pays out to whoever is named on the beneficiary form, regardless of what your will says. Review every account and policy to confirm the named beneficiaries match your overall plan.

-

Brief your representatives. Simply naming a healthcare proxy is not enough. Sit down with your proxy and your financial agent and explain your specific wishes. Tell them where your documents are stored. A prepared representative acts quickly and confidently. An unprepared one hesitates, and that hesitation can cost your family time and money.

-

Schedule regular reviews. An estate plan is not a one-time task. Review it after every major life event: marriage, divorce, the birth of a child, a death in the family, a significant change in assets, or a move to a different state. Outdated documents cause delays, increased costs, and incorrect asset distribution.

Pro Tip: Set a calendar reminder every two years to review your estate plan, even if nothing major has changed. Tax laws and state regulations shift, and your plan needs to keep pace.

For a broader look at how your estate plan fits into long-term financial security, Finblog’s wealth protection strategies guide covers the full picture.

Common mistakes to avoid in estate planning

Most estate plans fail not because of bad intentions but because of predictable, avoidable errors. Knowing what they are puts you ahead of most families.

- Failing to update beneficiary designations. Life changes constantly. Divorce, remarriage, and the birth of children all require immediate updates to beneficiary forms on retirement accounts and insurance policies. A will cannot override a beneficiary designation.

- Skipping the conversation with fiduciaries. Naming someone as your healthcare proxy without telling them your specific medical preferences leaves them guessing. Prepared fiduciaries enable smooth estate administration and medical decision-making. Unprepared ones create delays and sometimes court involvement.

- Forgetting the Certificate of Trust. Families who set up a trust but never obtain a Certificate of Trust face friction every time they try to conduct a transaction in the trust’s name. Banks and title companies need this document to verify the trust’s authority.

- Assuming a will covers everything. A will only controls assets that go through probate. Accounts with named beneficiaries, jointly held property, and trust assets all pass outside the will entirely. Relying on a will alone leaves major gaps.

- Delaying reviews after life changes. An estate plan written when your children were minors may be completely wrong once they are adults. A plan drafted before a divorce may still name the wrong people.

“Discussing wills, trusts, proxies, and document locations with fiduciaries helps prevent administrative chaos, delays, and court involvement during crises. Prepared fiduciaries enable smooth estate administration and medical decision-making.”

For families thinking about how estate planning connects to generational wealth, the structure of your documents today determines what your heirs receive tomorrow.

Key Takeaways

A complete estate plan requires five to six core documents, properly funded and regularly updated, to protect your assets and guarantee your wishes are followed.

| Point | Details |

|---|---|

| Core documents required | Every plan needs a will, living trust, powers of attorney, healthcare directive, and HIPAA authorization. |

| Fund your trust | Transferring assets into the trust is required. An unfunded trust provides no probate protection. |

| Beneficiary designations override wills | Review and update beneficiary forms on all accounts and policies to match your overall plan. |

| Brief your fiduciaries | Tell your agents and proxies your specific wishes and where your documents are stored. |

| Review after life changes | Update your plan after marriage, divorce, births, deaths, or significant changes in assets or state law. |

Why I think most families wait too long on this

People treat estate planning like a task for later, for when they are older, wealthier, or have more time. I have seen what happens when “later” never comes. A family spends months in probate court over a modest estate because there was no trust. A spouse is blocked from a hospital room because there was no HIPAA authorization on file. These are not rare edge cases. They are common outcomes of common delays.

The part that surprises most people is how much of estate planning comes down to communication, not paperwork. You can have every document signed and notarized, but if your healthcare proxy does not know your wishes on life support, that document is nearly useless in a crisis. The legal framework matters, but the conversations you have with the people you name matter just as much.

My strong view is that combining a will with a revocable living trust is the right move for most families, not just wealthy ones. Probate is slow, public, and expensive in most states. A trust sidesteps all of that. The upfront cost of setting one up is almost always less than what probate costs your heirs later.

Keep your documents organized and tell someone where they are. A binder in a fireproof safe, with a note to your executor explaining what is inside, is worth more than the most sophisticated legal structure that nobody can find when it matters.

— Povilas

Finblog’s estate planning resources for your next step

Finblog covers estate planning in depth, from the basics of document selection to the details of wealth transfer strategies that protect what you have built. The Finblog estate planning guide walks through every core document, explains how trusts and wills work together, and covers how tax law changes affect your plan. For families focused on passing wealth across generations, Finblog also addresses how estate taxes interact with your documents and beneficiary choices. Use these resources to stay current as laws change and your financial situation evolves.

FAQ

What is estate planning, and why does it matter?

Estate planning is the process of preparing legal documents that direct how your assets are managed and distributed during incapacity or after death. Without a plan, courts make those decisions for you, often slowly and at significant cost to your family.

What documents does a basic estate plan include?

A basic estate plan includes a last will and testament, a revocable living trust, a durable financial power of attorney, a healthcare power of attorney, an advance healthcare directive, and a HIPAA authorization. These five to six documents cover the full range of financial and medical scenarios.

Do beneficiary designations override a will?

Yes. Beneficiary designations on retirement accounts and life insurance policies override whatever your will says. Keeping these designations synchronized with your overall estate plan is critical to avoiding unintended inheritance outcomes.

How often should you update your estate plan?

Review your estate plan after every major life event, including marriage, divorce, the birth of a child, or a significant change in assets. A general review every two years is also good practice, since tax laws and state regulations change regularly.

What is a Certificate of Trust, and do you need one?

A Certificate of Trust is a short document that proves your trust exists and confirms the trustee’s authority without revealing the trust’s private terms. Banks and title companies require it when you transfer accounts or property into the trust’s name.