TL;DR:

- Building a diversified portfolio involves spreading investments across different asset classes, sectors, and regions to reduce risk.

- The four core assets are stocks, bonds, cash equivalents, and alternatives, each serving distinct roles and responding differently to economic changes.

- The best long-term strategy is to choose simple, low-cost index funds, rebalance annually, and allocate based on your time horizon rather than emotional risk tolerance.

Building a diverse portfolio is defined as spreading your investments across multiple asset classes, sectors, and geographies to reduce the impact of any single loss on your overall wealth. Diversification helps reduce risk but never guarantees a profit during market declines. That distinction matters. The goal is not to eliminate risk entirely. The goal is to make sure one bad bet does not sink your financial future. This guide walks you through the asset classes, allocation frameworks, and behavioral habits that separate disciplined investors from reactive ones.

What asset classes belong in a diverse portfolio?

True diversification requires thoughtful selection of complementary asset classes, not just a high quantity of holdings. Morningstar experts are clear on this point: collecting many similar assets does not provide the protection investors expect. You need assets that respond differently to the same economic conditions.

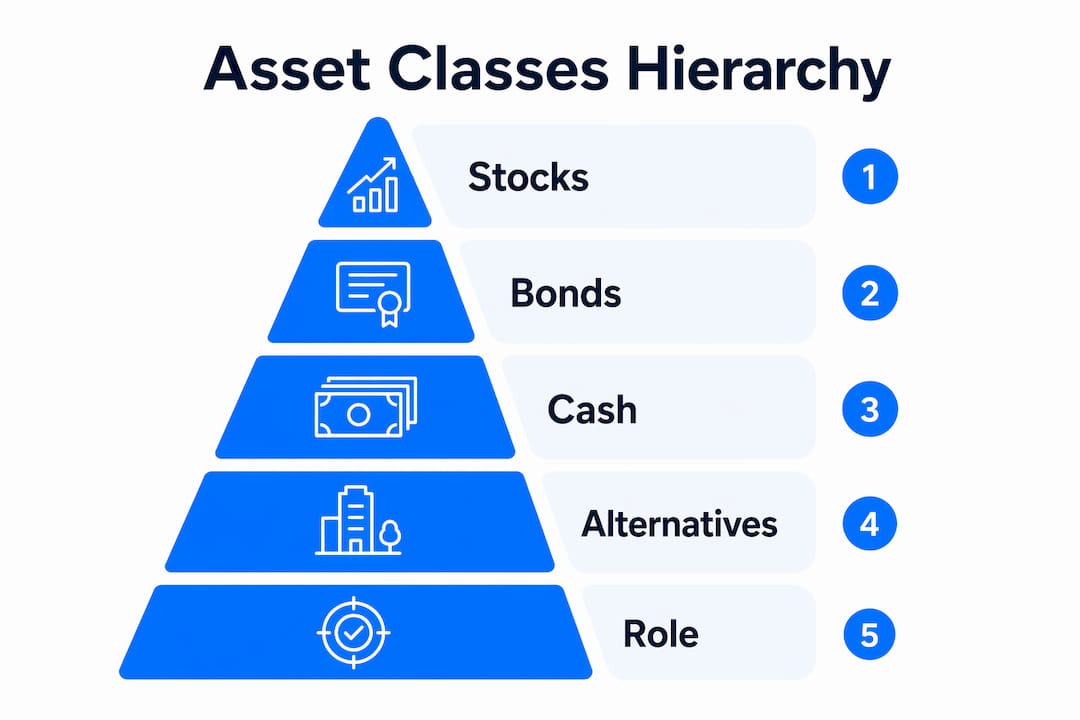

The four core asset classes are stocks, bonds, cash equivalents, and alternatives. Each plays a distinct role.

Stocks deliver long-term growth but carry the highest short-term volatility. A technology stock and a consumer staples stock may both be equities, but they behave very differently during a recession. Sector diversification within stocks matters as much as the stock-to-bond ratio.

Bonds act as a stabilizer. When stock markets fall, high-quality bonds often hold their value or rise. Short-term bonds and Treasury Inflation-Protected Securities (TIPS) add fixed-income diversification that a total bond market index alone cannot provide. TIPS, in particular, protect purchasing power when inflation rises.

Cash equivalents include money market funds and short-term Treasury bills. They earn modest returns but give you liquidity when markets drop, so you are not forced to sell stocks at a loss to cover expenses.

Alternatives such as real estate investment trusts (REITs), commodities, and infrastructure funds add another layer of protection. These assets often move independently of stocks and bonds, which is exactly what you want.

| Asset class | Risk level | Typical role |

|---|---|---|

| Stocks | High | Long-term growth engine |

| Bonds | Low to medium | Stability and income |

| Cash equivalents | Very low | Liquidity and capital preservation |

| REITs | Medium to high | Inflation hedge and income |

| Commodities | High | Inflation protection and diversification |

| TIPS | Low to medium | Inflation-adjusted income |

Pro Tip: Index mutual funds and ETFs are the most cost-efficient way to gain broad market exposure across all these classes. Christine Benz of Morningstar advocates index products as the core of any well-built portfolio.

How do you determine the right asset allocation?

Your time horizon is the single most important factor in deciding how to allocate your investments. Christine Benz of Morningstar states that risk tolerance should “jump in the backseat” to time horizon in allocation decisions. That is a direct challenge to conventional wisdom, and it is correct.

Most investors confuse risk tolerance with risk capacity. Risk tolerance is how much volatility you can stomach emotionally. Risk capacity is how much loss you can absorb financially without derailing your goals. A 35-year-old saving for retirement has high risk capacity even if they feel anxious watching markets drop. A 60-year-old planning to retire in two years has low risk capacity even if they feel calm about volatility.

The classic 60/40 portfolio, which holds 60% stocks and 40% bonds, remains a useful starting point for investors with a medium time horizon of 10–20 years. Younger investors with 30-plus years before retirement can tilt heavier toward equities. Investors within five years of a major financial goal should shift toward bonds and cash to protect what they have built.

The bucket approach, formally called time segmentation, organizes your portfolio by spending horizon rather than asset class alone. Time segmentation buckets cash, fixed income, and equities by when you plan to spend the money. Bucket one holds one to two years of living expenses in cash. Bucket two holds bonds for years three through ten. Bucket three holds stocks for everything beyond that. This structure gives you the psychological security to leave your equity bucket alone during downturns.

- Short time horizon (under 5 years): Weight toward bonds, TIPS, and cash equivalents.

- Medium time horizon (5–15 years): A 60/40 or 70/30 stock-to-bond split works well.

- Long time horizon (15-plus years): Equities can make up 80–90% of the portfolio.

- Near-retirement adjustment: Shift 5–10% from equities to bonds every three to five years as you approach your goal date.

Pro Tip: Even young investors with near-term financial goals should keep some liquid, low-risk assets on hand. Selling stocks during a downturn to cover a short-term expense locks in losses and disrupts your long-term plan.

What practical steps build and maintain a well-diversified portfolio?

Building asset diversity is a process, not a single decision. Follow these steps to move from intention to execution.

-

Set your goals and time horizon. Write down what you are investing for and when you need the money. Retirement in 25 years and a home purchase in 3 years require completely different approaches. Separate these goals into separate accounts if possible.

-

Choose your asset class mix. Use your time horizon and risk capacity to set target percentages. A simple starting point: subtract your age from 110 to get your stock allocation percentage. A 40-year-old would hold roughly 70% stocks and 30% bonds and cash.

-

Select your investment vehicles. Broad index funds and ETFs cover entire markets at low cost. A total stock market index fund, an international stock index fund, a total bond market fund, and a TIPS fund give you global diversification in four holdings. Check the asset allocation strategies guide at Finblog for detailed vehicle comparisons.

-

Purchase and document your holdings. Record your target allocation and the actual percentage each holding represents. This baseline is what you will return to when you rebalance.

-

Rebalance once a year. Rebalancing annually keeps your portfolio aligned with its intended allocation as markets move. If stocks surge and now represent 80% of your portfolio instead of 70%, sell enough to bring them back to target and buy underweighted assets.

-

Review after major life events. A new job, a marriage, a child, or a health change can shift your risk capacity. Review your allocation after any event that changes your financial picture.

Common pitfalls to avoid during this process:

- Fund overlap: Owning three large-cap growth funds feels like diversification but is not. Check the top holdings of each fund to confirm they are not duplicating each other.

- Chasing performance: Buying last year’s top-performing sector is a reliable way to buy high and sell low. Stick to your allocation plan.

- Ignoring international exposure: U.S. stocks represent roughly half of global market capitalization. Holding only domestic equities leaves half the world’s growth on the table.

Pro Tip: Use your tax-advantaged accounts, such as a 401(k) or IRA, to hold your least tax-efficient assets. Bonds and REITs generate ordinary income, which is taxed at higher rates. Keep them in tax-sheltered accounts and hold index funds in taxable accounts.

What mistakes undermine investment diversification?

The most common mistake is assuming that owning more funds automatically means better diversification. Spreading money across too many investments can add complexity and increase transaction costs without reducing risk proportionally. Twenty funds that all hold the same 500 large-cap stocks give you the illusion of variety with none of the protection.

Overlapping holdings are the hidden enemy of a balanced portfolio. Two funds labeled “growth” and “blend” may share 70% of their top ten holdings. Before adding any new fund, compare its holdings against what you already own.

Behavioral mistakes cause more damage than poor fund selection. Investors who check their portfolios daily are more likely to react to short-term noise. Focusing on your investment timeline reduces emotional decisions and aligns your risk with your actual financial needs.

“True diversification requires thoughtful selection of complementary asset classes, not just a high quantity of holdings. Morningstar’s research confirms that investors who collect many similar assets often discover their protection was an illusion when markets fall together.”

Neglecting to rebalance is equally damaging in the opposite direction. A portfolio that started at 60% stocks can drift to 80% stocks after a multi-year bull market. That investor now carries far more risk than they intended, without ever making a conscious decision to do so.

Key Takeaways

A well-built portfolio spreads investments across complementary asset classes, allocates based on time horizon rather than emotion, and rebalances annually to stay on target.

| Point | Details |

|---|---|

| Asset class variety matters | Stocks, bonds, TIPS, REITs, and cash each respond differently to market conditions. |

| Time horizon drives allocation | Set your stock-to-bond ratio based on when you need the money, not how you feel about risk. |

| Index funds are the core | Low-cost index ETFs and mutual funds provide broad exposure with minimal overlap. |

| Rebalance once a year | Annual rebalancing keeps your actual allocation aligned with your intended risk level. |

| More funds is not better | Overlapping holdings create false diversification and add unnecessary cost and complexity. |

Why simplicity beats complexity in portfolio building

I have watched investors spend months researching exotic funds, sector rotations, and alternative strategies, only to end up with a portfolio that underperforms a simple three-fund index approach. The research consistently backs this up, and so does my experience.

The investors who do best are not the ones who trade the most. They are the ones who set a clear allocation, automate their contributions, and rebalance once a year without drama. They treat their portfolio like a long-term project, not a daily puzzle to solve.

The bucket approach changed how I think about retirement planning. When you can point to a specific account holding two years of cash, you stop worrying about what the stock market did this week. That peace of mind is not just psychological comfort. It prevents the panic selling that destroys long-term returns.

My honest advice: start with four index funds covering U.S. stocks, international stocks, bonds, and TIPS. Add complexity only when you have a specific reason, not because more feels like more. Discipline and consistency beat sophistication every time.

— Povilas

Finblog resources for your next portfolio step

Finblog offers a growing library of guides built specifically for individual investors who want to move from theory to practice. Whether you are setting your first allocation or refining a portfolio you have held for years, the investment diversification resources at Finblog cover the full process in plain language. For investors ready to go deeper on allocation mechanics, the asset allocation strategies guide breaks down how to distribute holdings across asset classes for specific long-term goals. Sign up for the Finblog newsletter to get new research and practical frameworks delivered directly to your inbox.

FAQ

What is the simplest way to build a diverse portfolio?

Buy a total stock market index fund, an international stock index fund, and a total bond market fund. These three holdings give you exposure to thousands of securities across global markets at low cost.

How often should I rebalance my portfolio?

Rebalance once a year. Annual rebalancing keeps your allocation aligned with your original targets without generating excessive transaction costs or tax events.

Does diversification guarantee I won’t lose money?

No. Diversification reduces risk but does not eliminate it. During broad market downturns, most asset classes can fall together, though a well-diversified portfolio typically loses less than a concentrated one.

What is the 60/40 portfolio rule?

The 60/40 portfolio holds 60% stocks and 40% bonds. It serves as a baseline for investors with a medium time horizon of 10–20 years and balances growth potential with stability.

How do I know if my portfolio is truly diversified?

Check for fund overlap by comparing the top holdings of each fund you own. True diversification means your assets respond differently to the same economic conditions, not just that you hold many funds with different names.