TL;DR:

- Owning many stocks within the same sector does not provide true diversification because asset interactions and correlations matter more than quantity.

- Effective diversification involves combining low or negatively correlated assets, such as US stocks, international stocks, and bonds, to reduce overall portfolio risk.

You probably already know that putting all your money into one stock is a bad idea. But here’s what most beginner investors get wrong: owning 50 different stocks inside the same sector is not diversification. True diversification explained properly is about how your assets interact with each other, not just how many you own. In this guide, Finblog breaks down what diversification really means, why correlation is the key concept most people miss, and how to build a portfolio that genuinely reduces risk without sacrificing returns.

Table of Contents

- Key takeaways

- Diversification explained: the fundamentals

- Common diversification strategies for your portfolio

- Why traditional diversification is under pressure

- How to build and maintain a diversified portfolio

- Comparing popular diversification approaches

- My take on what really matters with diversification

- Build your knowledge with Finblog

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Correlation drives real diversification | Assets with low or negative correlation protect your portfolio better than simply owning more holdings. |

| Three asset classes form a solid core | Combining US stocks, international stocks, and investment-grade bonds covers the foundation for most investors. |

| Rebalancing adds measurable returns | Disciplined rebalancing can add 0.5% to 1.0% in annualized return over time by forcing a buy-low approach. |

| Stock-bond correlation is shifting | Recent years have seen stocks and bonds move more in sync, making uncorrelated assets like gold more important. |

| Simplicity outperforms complexity | Low-cost index funds and ETFs give most investors better long-term outcomes than complex multi-asset strategies. |

Diversification explained: the fundamentals

Diversification in investments means spreading your money across assets that do not all react the same way to the same events. When one investment falls, another may hold steady or rise. That offset is what reduces overall portfolio risk.

The academic backbone behind this idea comes from Nobel laureate Harry Markowitz, who showed that combining low-correlation assets reduces risk without necessarily cutting returns. Markowitz called this the only free lunch in investing, and that framing has stuck in financial theory for good reason.

The concept you need to understand is correlation, which measures how two assets move relative to each other. A correlation of +1 means they move in perfect lockstep. A correlation of 0 means they move independently. A correlation of -1 means when one goes up, the other goes down. For diversification to actually work, you want assets closer to 0 or negative territory.

Here is what that looks like in practice:

- Stocks and bonds have historically had a correlation of about 0.08 since 1960, which is why the classic stock/bond mix became the default for decades.

- During a stock market selloff, bonds often hold value or gain, acting as a shock absorber.

- Concentration risk in single sectors increases volatility because holdings within the same asset class tend to fall together in a downturn.

The diversification meaning here is simple: own things that do not all lose value at the same moment, for the same reasons.

Common diversification strategies for your portfolio

Knowing the theory is step one. Applying it is where most people stall. There are several practical diversification strategies you can use, and they work at multiple levels of your portfolio.

Asset class diversification

The most foundational level involves spreading money across different types of investments. Stocks carry high return potential with high volatility. Bonds provide income and stability. Commodities like gold often move independently of financial markets. Cash preserves capital and reduces overall volatility. You can explore the full breakdown of asset classes in detail to understand how each behaves across market cycles.

Sector and geographic diversification

Even within stocks, you can diversify further. Owning technology stocks, healthcare stocks, energy stocks, and consumer goods stocks means your portfolio does not collapse when one sector has a bad year. Geographic diversification adds another layer. US markets, international developed markets like Europe and Japan, and emerging markets such as India and Brazil do not always move together.

Here is a practical approach to building a diversified portfolio step by step:

- Set your target allocation based on your age, risk tolerance, and time horizon. A 35-year-old might hold 80% stocks and 20% bonds. A 60-year-old might shift to 50/50.

- Split your stock allocation across US, international developed, and emerging market funds. A simple split might be 60% US, 30% international developed, 10% emerging markets.

- Add sector exposure using broad index funds that cover multiple sectors automatically, or add specific sector ETFs where you see gaps.

- Include stabilizing assets such as bonds, Treasury Inflation-Protected Securities (TIPS), or commodity funds to counterbalance stock volatility.

- Use low-cost ETFs or index funds for each category. They give you instant broad coverage without requiring you to pick individual securities.

A typical 60/40 portfolio (60% stocks, 40% bonds) has historically generated better risk-adjusted returns than equity-only benchmarks in about 80% of rolling periods since 1976. That is a powerful argument for staying disciplined with asset class diversification.

Why traditional diversification is under pressure

The investing environment has shifted, and some of what used to be reliable no longer holds the same way. Understanding these shifts is critical for anyone building a portfolio today.

The biggest challenge is that stock-bond correlations have increased in recent years. During the inflationary period of 2022, both stocks and bonds fell sharply at the same time, which left traditionally diversified portfolios without a safe corner to hide in. When your “hedge” falls alongside your main holdings, the diversification benefit disappears.

This is not a reason to abandon bonds entirely. It is a reason to broaden your thinking about what counts as an uncorrelated asset:

- Gold and commodities tend to perform well during inflationary periods. Gold’s near-zero or negative correlation with stocks over recent periods makes it a genuine diversifier.

- Managed futures strategies are funds that can go long or short across many markets and historically perform independently from stocks and bonds.

- Market-neutral strategies aim to produce returns regardless of market direction by balancing long and short positions.

On the other hand, not every alternative asset delivers genuine diversification. Private equity and cryptocurrency can carry high volatility and significant equity market sensitivity, which limits their value as diversifiers even when their correlation appears low on paper. A small allocation to Bitcoin, for instance, does not meaningfully stabilize a portfolio when crypto markets crash by 70% in a year.

Pro Tip: Before adding any “alternative” asset class, check its behavior during equity market selloffs specifically. Low average correlation is less useful if the asset crashes alongside stocks during the exact moments you need protection.

Finblog’s analysis of evolving diversification strategies in 2026 covers how these shifting correlations are reshaping how smart investors approach asset allocation right now.

How to build and maintain a diversified portfolio

Theory and strategy are only useful if you follow through consistently. Here is where most investors fall short.

The first step is choosing an allocation that reflects your personal goals. A young investor with a 30-year time horizon can absorb more volatility and should lean heavier into stocks for growth. Someone five years from retirement needs capital preservation and should tilt toward bonds and stable assets. There is no universal answer, but your time horizon is the clearest guide.

The second step is rebalancing regularly. Over time, your winners grow and your losers shrink, which means your original allocation drifts. If stocks surge, your portfolio might shift from 60/40 to 75/25 without you doing anything. Rebalancing brings it back into line and, importantly, forces you to sell what has risen and buy what has fallen. Rebalancing can add 0.5% to 1.0% in annualized returns over the long run by enforcing this buy-low, sell-high discipline.

Pro Tip: Set a calendar reminder to review your allocation every six months. Alternatively, rebalance any time an asset class drifts more than 5% from its target weight.

A few common mistakes to avoid:

- Over-diversifying: Owning 15 funds that all track the same broad US market index does not reduce risk. You are duplicating exposure, not adding true diversification.

- Chasing last year’s winners: Rotating into the best-performing asset class after its run often means buying high and setting yourself up for disappointment.

- Ignoring costs: Diversification is not free. Management fees, trading costs, and tax consequences from rebalancing all reduce net returns. Low-cost index funds minimize this friction significantly.

- Neglecting international exposure: Many US investors are home-country biased. International stocks have historically provided genuine return and diversification benefits over long periods.

For a practical framework on how to diversify investments across your whole financial picture, the Finblog guide on diversifying your investments covers both the logic and the mechanics in plain terms.

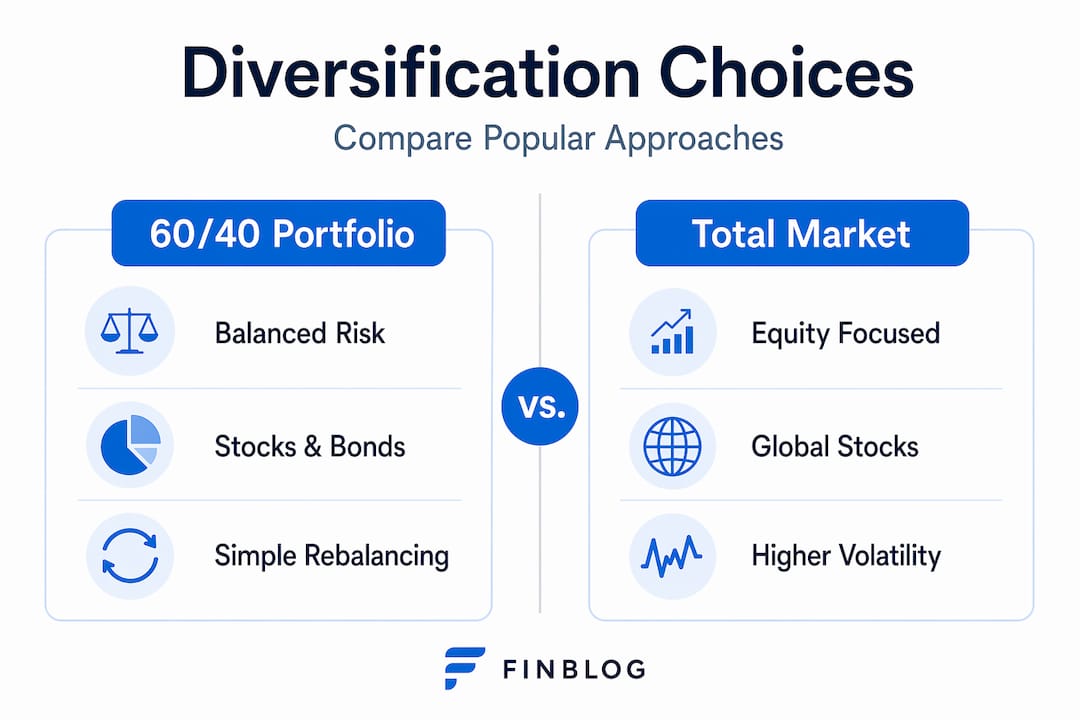

Comparing popular diversification approaches

Not all portfolios are built the same way. Here is how the most common approaches compare so you can assess which fits your situation.

| Approach | Typical allocation | Best for | Key risk |

|---|---|---|---|

| Classic 60/40 | 60% stocks, 40% bonds | Moderate risk investors | Stock-bond correlation rising |

| Aggressive growth | 90% stocks, 10% bonds | Long time horizon, high risk tolerance | High short-term volatility |

| Conservative | 30% stocks, 70% bonds/cash | Near-retirement investors | Low growth, inflation risk |

| Multi-asset class | Stocks, bonds, gold, alternatives | Sophisticated investors | Complexity and higher fees |

| Three-asset core | US stocks, intl stocks, bonds | Most individual investors | Requires discipline to maintain |

Combining US stocks, international stocks, and investment-grade bonds is effective for most individual investors and does not require active management or expensive funds. The three-asset core approach is where most novices should start before adding complexity.

The data supports simplicity. The 60/40 portfolio has outperformed equity-only portfolios in the vast majority of rolling periods measured since 1976, not because it is clever, but because it is consistent. More complex multi-asset portfolios can improve on that record, but only when managed thoughtfully. Adding alternatives without understanding their cost structure and behavior typically hurts more than it helps.

My take on what really matters with diversification

I have spent years watching investors overcomplicate portfolios in the belief that more complexity equals better protection. It rarely does.

The most common mistake I see is confusing quantity with quality. Someone owns 12 funds and feels diversified, but eight of those funds are variations of US large-cap growth. They have a crowded portfolio, not a diversified one. True diversification is about what is different in your holdings, not how many you have.

What actually works, in my experience, is a simple allocation held consistently over a long time, with regular rebalancing and low fees. The investors who do best are not the ones with the most sophisticated strategies. They are the ones who do not panic when markets drop, stay consistent with their allocation, and avoid the temptation to redesign their portfolio every time something shifts.

My honest advice for anyone starting out: build a three or four fund portfolio using low-cost index funds, set a rebalancing schedule, and then leave it alone. The emotional discipline of staying the course is worth more than any complex strategy that requires constant attention or expensive management.

— Povilas

Build your knowledge with Finblog

Understanding diversification in investments is one of the best foundations you can build as an investor. Finblog has a growing library of resources to help you go deeper. The article on why diversification pays off covers the data behind long-term diversification benefits with concrete historical performance evidence. If you want the full strategic picture, the Finblog guide to diversifying investments walks through why diversification matters at every stage of your investing life, with advice tailored to different risk profiles. For traders interested in diversification across different market types, diversified portfolio approaches in forex trading offers a useful perspective on extending these principles beyond traditional assets. Whether you are building your first portfolio or refining one you already have, these resources will sharpen your thinking and give you practical steps to act on.

FAQ

What does diversification mean in investing?

Diversification in investments means spreading your money across different asset types, sectors, and geographies so that poor performance in one area does not sink your whole portfolio. The goal is to own assets with low or negative correlation to each other.

How many assets do you need for diversification?

You do not need dozens of holdings. Combining US stocks, international stocks, and investment-grade bonds in a simple three-fund portfolio covers the core diversification needs of most individual investors effectively.

Does diversification eliminate all investment risk?

No. Diversification reduces unsystematic risk (the risk specific to individual companies or sectors) but cannot eliminate systematic risk, which is the broad market risk that affects all assets during major economic downturns.

Why is the 60/40 portfolio under scrutiny today?

Rising stock-bond correlations in recent years have weakened the traditional 60/40 approach. When both asset classes fall simultaneously (as in 2022), the portfolio’s protective balance breaks down, prompting investors to consider adding uncorrelated assets like gold or managed futures.

What is the cheapest way to diversify a portfolio?

Low-cost total market index funds and ETFs are the most affordable way to achieve broad diversification. They offer instant exposure across hundreds or thousands of securities at a fraction of the cost of actively managed alternatives.