The Iran conflict did more than push oil prices higher. It changed market leadership, pressured global equities, and forced investors to rethink inflation and interest-rate expectations.

After the war escalated at the end of February, markets moved from optimism to risk-off positioning as concerns grew around energy supplies and trade disruption.

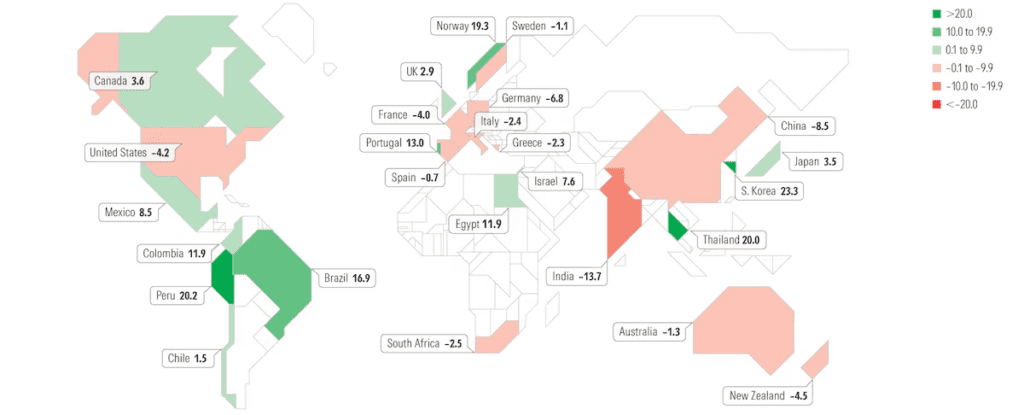

Emerging Markets Took the Hardest Hit

Global stocks were already performing well before the conflict. Countries across Asia, Latin America, and parts of Europe had posted strong gains, but sentiment shifted quickly after tensions escalated.

March performance showed:

- Morningstar Emerging Markets Index: -12.6% in one month

- Developed Markets ex-US: -9.9%

- Morningstar US Market Index: -5%

Emerging markets were hit harder because many economies are more sensitive to commodity prices and energy costs. At the same time, Europe and Japan faced additional pressure because of their dependence on Middle East energy flows.

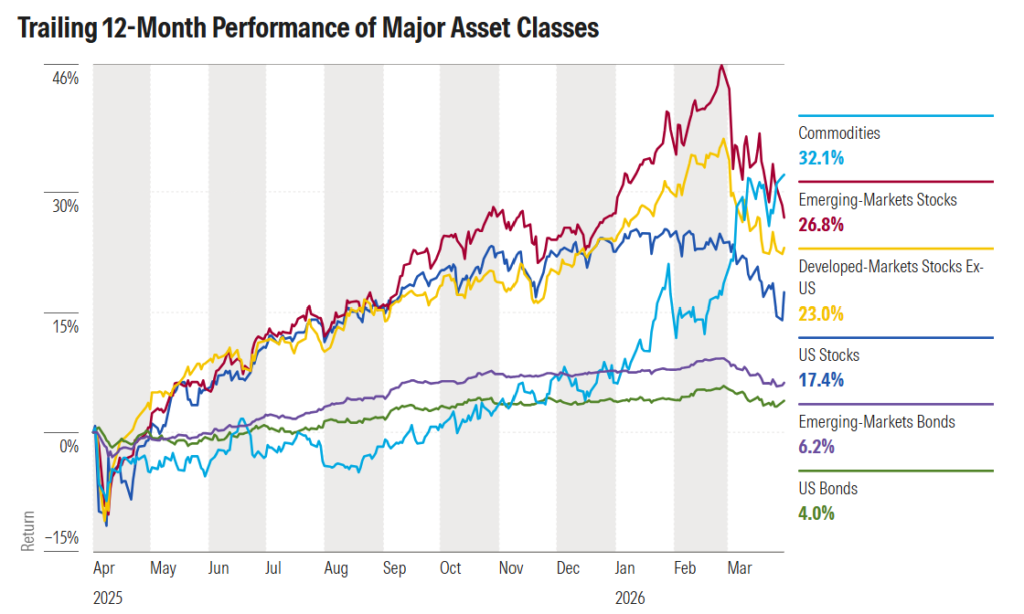

Oil Became the Center of the Story

The biggest market reaction came from energy.

Higher oil prices lifted: Energy producers, Commodity stocks, Oil-linked assets

But the same move created problems elsewhere. Rising energy costs increased inflation concerns and pressured broader equity markets. The risk became even bigger because of concerns around the Strait of Hormuz, one of the world’s most important energy shipping routes.

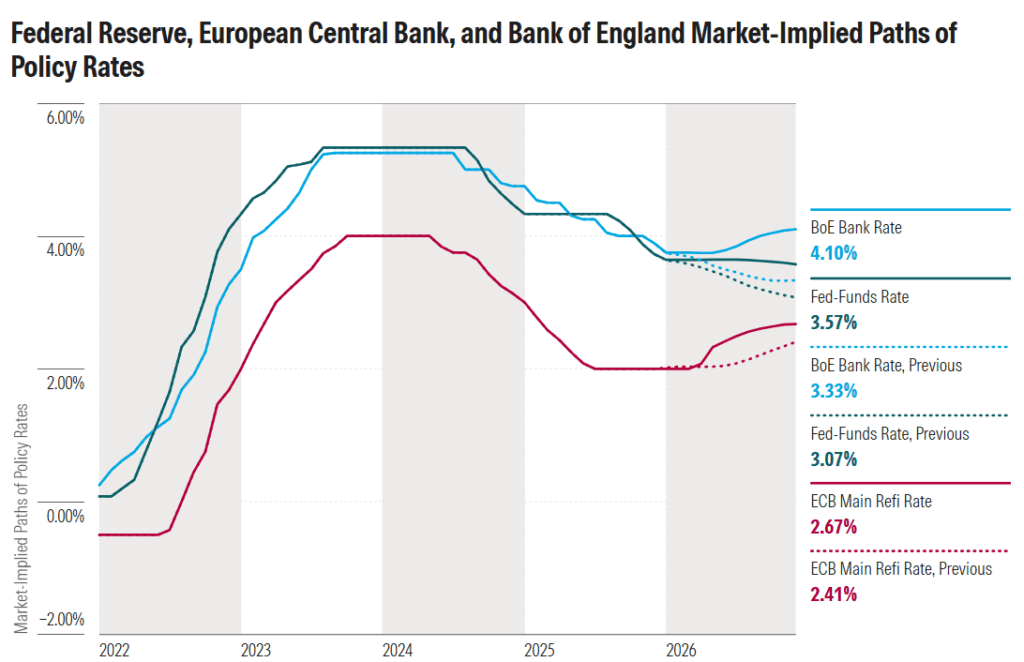

Markets Removed Rate Cuts

The conflict also changed monetary expectations. At the end of 2025, markets expected rate cuts in 2026.

That view largely disappeared after oil prices surged. Investors now expect:

- No Fed cuts in 2026

- Possible tightening pressure in Europe and the UK

- More restrictive policy to control inflation risks

The oil shock effectively pushed markets toward a higher-for-longer rate outlook.

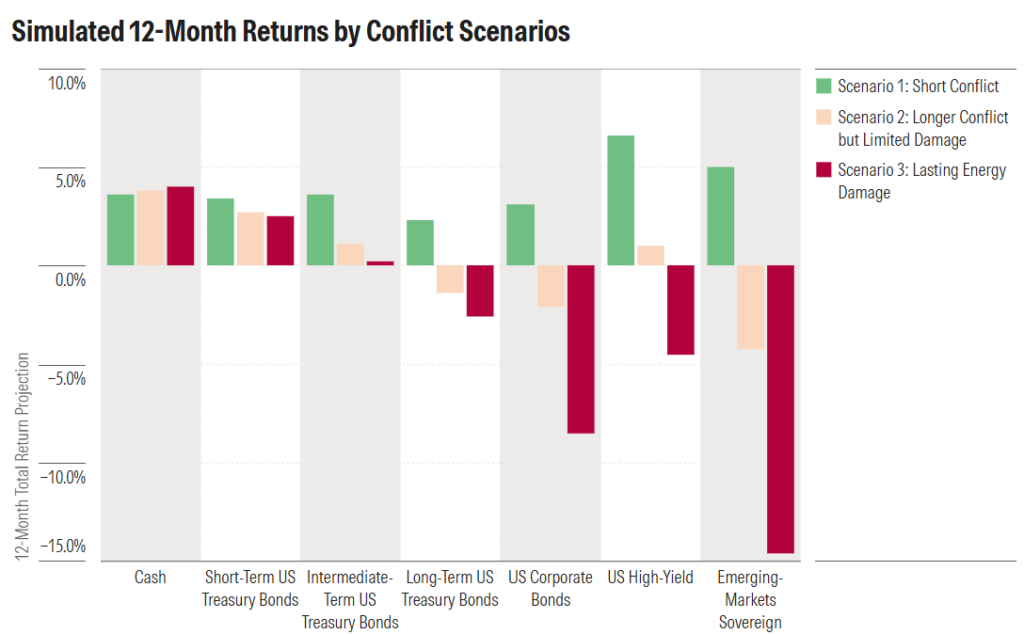

Three Possible Paths Ahead

Morningstar outlined three scenarios:

- Short disruption → temporary market pressure

- Longer contained conflict → winners and losers emerge

- Persistent oil shock → wider credit spreads, bond pressure, and larger losses in emerging markets

Markets have remained more resilient than many expected so far.

But investors are now watching something bigger than the conflict itself. Oil prices, inflation, and central-bank reactions may become more important than the war headline alone.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.