Many high-net-worth individuals assume all trusts automatically avoid estate taxes, but this widespread belief is simply wrong. The reality is far more nuanced. Understanding which trust structures genuinely shield your wealth from taxation and which serve other strategic purposes is critical to effective estate planning. This guide clarifies trust fund fundamentals, compares key trust types, and shows you how to select and manage trusts that truly protect your financial legacy.

Table of Contents

- What Is A Trust Fund?

- Why Use Trust Funds For Wealth Preservation?

- Types Of Trust Funds: Revocable Vs. Irrevocable

- Types Of Specialized Trusts For Estate Planning

- Common Misconceptions About Trust Funds

- How To Select And Manage Trust Funds Effectively

- Conclusion: Leveraging Trust Funds For Legacy Planning

- Explore Expert Resources For Trust Fund Planning

Key takeaways

| Point | Details |

|---|---|

| Trust fund basics | A legal arrangement where a trustee manages assets for beneficiaries according to the grantor’s instructions. |

| Revocable vs. irrevocable | Revocable trusts offer flexibility but no tax benefits; irrevocable trusts provide estate tax savings and asset protection. |

| Specialized options | Credit shelter, charitable remainder, and special needs trusts serve specific estate planning and tax goals. |

| Selection strategy | Match trust types to your wealth goals, fund properly, and maintain ongoing professional oversight. |

| Common myths | Not all trusts avoid estate taxes, trusts aren’t always permanent, and costs vary widely by complexity. |

What is a trust fund?

A trust is a legal relationship where one person holds title to property for the benefit of another, established under state law. This formal arrangement involves three key parties working together to manage and distribute wealth according to specific terms.

The grantor creates the trust and transfers assets into it. The trustee holds legal title to those assets and manages them according to the trust document’s instructions. The beneficiary receives benefits from the trust assets, either immediately or at specified future times.

Key characteristics of trust funds include:

- Legal ownership separates from beneficial enjoyment of assets

- Written trust documents specify exactly how assets should be managed and distributed

- State laws govern trust formation, administration, and enforcement

- Trustees have fiduciary duties requiring them to act in beneficiaries’ best interests

- Trusts can hold virtually any asset including cash, investments, real estate, and business interests

This structure gives you remarkable control over how your wealth transfers across generations. You set the rules for when beneficiaries receive assets, under what conditions, and how trustees should invest and protect the funds. For families with significant wealth, this framework becomes indispensable for organized, intentional legacy planning.

Trusts operate independently of your personal ownership, which creates powerful planning opportunities. Once properly funded, trust assets follow the trust’s rules rather than standard inheritance laws. This separation forms the foundation for many advanced wealth preservation strategies.

Why use trust funds for wealth preservation?

Trust funds deliver several strategic advantages that directly benefit high-net-worth families seeking to preserve and transfer wealth efficiently. These benefits extend far beyond simple asset holding.

Trust funds can help protect assets from creditors, reduce estate taxes, avoid probate, and control asset distribution to beneficiaries. Asset protection ranks among the most valuable features. Properly structured trusts shield family wealth from creditors, lawsuits, and claims against individual family members. This legal barrier preserves your legacy even when beneficiaries face financial or legal challenges.

Tax minimization represents another major advantage. Strategic trust planning can significantly reduce or eliminate estate taxes, potentially saving millions for wealthy families. By removing assets from your taxable estate through irrevocable trusts, you preserve more wealth for future generations rather than government coffers.

Probate avoidance saves both time and money while maintaining privacy. Assets held in trust transfer directly to beneficiaries without court involvement, avoiding months or years of delays. Your estate details remain private rather than becoming public court records.

Key benefits include:

- Complete control over distribution timing and conditions for beneficiaries

- Protection against beneficiary mismanagement or poor financial decisions

- Continuity of professional management if you become incapacitated

- Flexibility to adapt to changing family circumstances within trust terms

- Coordination with other wealth preservation strategies for comprehensive planning

Pro Tip: Combining trusts with life insurance policies and business succession plans creates a comprehensive wealth protection strategy that addresses multiple risk scenarios simultaneously.

The privacy advantage cannot be overstated. Unlike wills, which become public during probate, trusts keep your wealth transfer plans confidential. This discretion protects family harmony and shields beneficiaries from unwanted attention or solicitation.

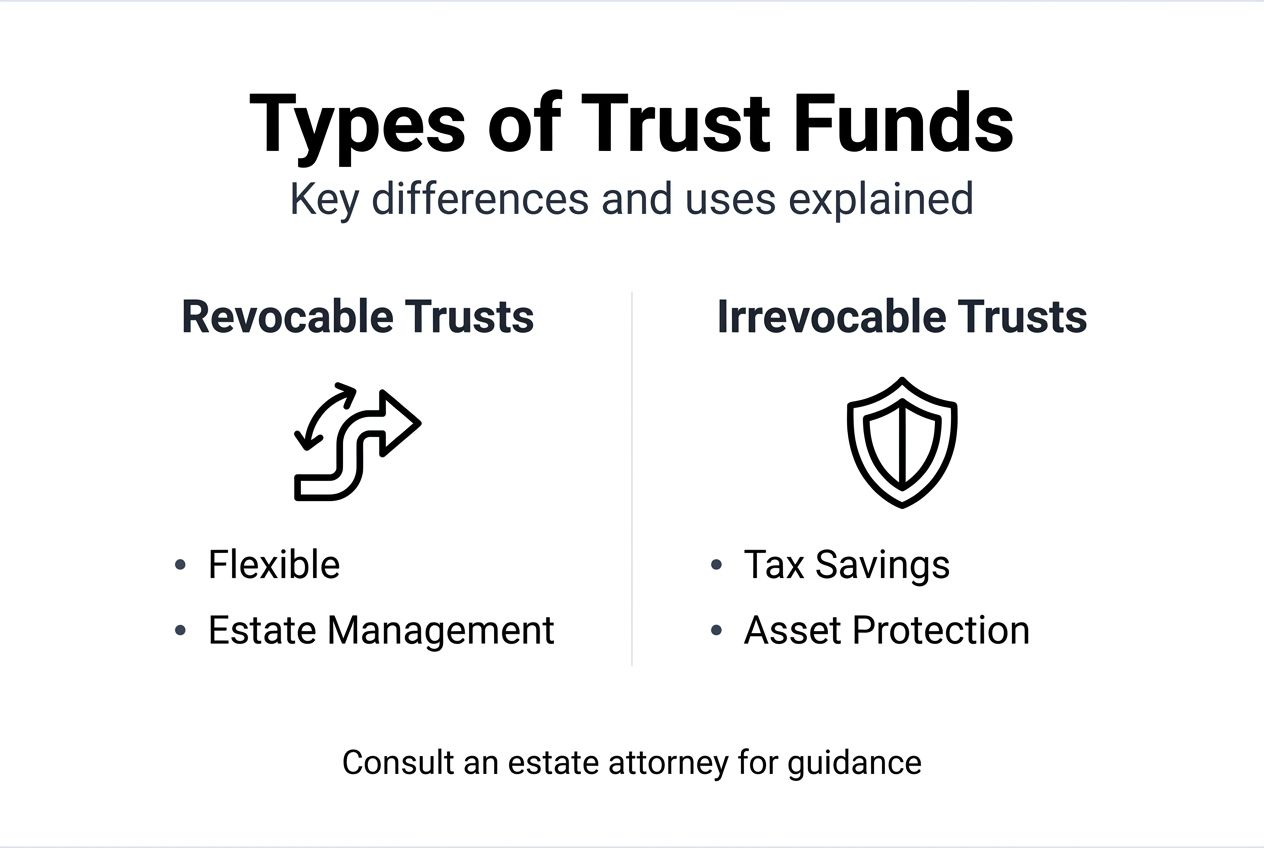

Types of trust funds: revocable vs. irrevocable

Understanding the fundamental distinction between revocable and irrevocable trusts is essential for making informed estate planning decisions. These two categories offer dramatically different features and benefits.

Revocable trusts allow amendment or revocation during the grantor’s lifetime but do not avoid estate taxes; irrevocable trusts provide estate tax benefits and asset protection by relinquishing grantor control. This tradeoff between control and tax benefits defines the choice between them.

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Grantor control | Full control to modify or revoke | Control permanently transferred to trustee |

| Estate tax treatment | Assets included in taxable estate | Assets removed from taxable estate |

| Creditor protection | No protection for grantor | Strong asset protection |

| Flexibility | Complete flexibility | Generally permanent |

| Primary benefit | Probate avoidance and privacy | Tax savings and asset protection |

Revocable trusts serve as excellent estate management tools. You maintain complete control, changing beneficiaries, trustees, or terms whenever circumstances change. These trusts become irrevocable automatically upon your death, at which point assets distribute according to your final instructions. They work particularly well for managing assets during potential incapacity and avoiding probate delays.

Irrevocable trusts sacrifice flexibility for powerful benefits. Once you transfer assets into an irrevocable trust, they leave your estate permanently. This removal triggers significant estate tax advantages and creates a legal barrier protecting assets from your creditors.

Key considerations for choosing between them:

- Current estate value relative to federal and state exemption limits

- Asset protection needs based on professional liability or lawsuit risk

- Desired control level over assets during your lifetime

- Tax planning priorities and potential estate tax exposure

- Family circumstances requiring either flexibility or firm boundaries

Pro Tip: Many wealthy families use both types strategically, placing liquid assets in revocable trusts for flexibility while moving appreciating assets into irrevocable trusts to freeze estate values and capture future growth tax-free.

The permanence of irrevocable trusts demands careful planning. Work closely with experienced estate attorneys to ensure trust terms align perfectly with your long-term goals before signing. Once established, modifying irrevocable trusts typically requires court approval or beneficiary consent, making initial planning critical.

Types of specialized trusts for estate planning

Beyond basic revocable and irrevocable structures, specialized trusts address specific estate planning goals for high-net-worth individuals. These sophisticated tools require expert guidance but deliver targeted benefits.

Credit shelter trusts, also called bypass trusts, maximize estate tax exemptions for married couples. When the first spouse dies, assets up to the exemption amount fund the credit shelter trust. This preserves the first spouse’s exemption while providing income to the surviving spouse. The trust principal stays outside the surviving spouse’s estate, preventing double taxation and preserving wealth for heirs.

Charitable remainder trusts combine philanthropy with financial benefits. You transfer assets into the trust, which pays you or designated beneficiaries income for a specified period or lifetime. When the trust term ends, remaining assets go to your chosen charity. You receive an immediate income tax deduction, remove assets from your taxable estate, and support causes you value while maintaining income flow.

Special needs trusts protect beneficiaries with disabilities without jeopardizing government benefits. These trusts supplement Medicaid, Supplemental Security Income, and other programs by paying for expenses those programs don’t cover. The trust holds assets outside the beneficiary’s name, preserving benefit eligibility while enhancing quality of life.

Additional specialized trust types include:

- Qualified personal residence trusts for transferring homes with reduced gift tax

- Grantor retained annuity trusts for passing appreciating assets to heirs efficiently

- Dynasty trusts for creating multi-generational wealth transfer spanning decades

- Life insurance trusts for removing policy proceeds from taxable estates

- Spendthrift trusts for protecting beneficiaries from their own poor financial decisions

Each specialized trust serves specific situations and goals. Credit shelter trusts make sense for couples with combined estates exceeding exemption amounts. Charitable remainder trusts benefit individuals with highly appreciated assets who want income plus charitable impact. Special needs trusts are essential for families with disabled members requiring long-term care.

Selecting appropriate specialized trusts requires detailed analysis of your family situation, asset composition, tax exposure, and legacy goals. Coordinate with legal and tax professionals specializing in wealth transfer strategies to design solutions matching your specific needs. These complex instruments deliver powerful results when properly structured and maintained.

Common misconceptions about trust funds

Several persistent myths about trusts lead to confusion and poor planning decisions. Clearing these misconceptions helps you approach trust planning with realistic expectations.

The most damaging myth claims all trusts avoid estate taxes. This is false. Revocable trusts offer no estate tax benefits whatsoever because you retain control over assets. They remain in your taxable estate exactly as if held in your personal name. Only irrevocable trusts that genuinely transfer control away from you remove assets from estate tax calculations.

Another common belief suggests all trusts are permanent and unchangeable. In reality, revocable trusts can be modified or dissolved anytime during your lifetime. Even some irrevocable trusts include provisions allowing modifications under specific circumstances. Modern trust drafting often incorporates flexibility mechanisms like trust protectors or powers of appointment.

Many people assume trusts are prohibitively expensive or complex. While sophisticated trusts for large estates involve substantial legal fees, simple revocable trusts cost far less and require minimal ongoing maintenance. The cost scales with complexity, not the mere existence of a trust structure.

Additional misconceptions include:

- Believing trusts eliminate all taxes when they only address estate taxes, not income taxes during your lifetime

- Assuming trusts automatically protect assets when only certain irrevocable structures provide creditor protection

- Thinking trust creation alone accomplishes goals when proper funding by retitling assets is equally critical

- Expecting trusts to operate without oversight when trustees need ongoing management and compliance

- Presuming trusts replace wills entirely when both documents serve complementary roles

Understanding these realities prevents costly mistakes. A revocable trust provides excellent probate avoidance and incapacity planning but offers zero tax savings. If reducing estate taxes drives your planning, you need irrevocable structures or specialized trusts designed specifically for tax efficiency.

Similarly, establishing a trust but failing to transfer assets into it accomplishes nothing. The trust remains an empty shell without the crucial funding step. Work with advisors who emphasize proper implementation, not just document creation.

Clearing confusion about wealth protection strategies ensures you select trust structures that actually deliver your desired outcomes rather than paying for features you don’t need or missing benefits you do need.

How to select and manage trust funds effectively

Successful trust planning requires matching trust structures to your specific estate goals and implementing them properly. Follow this systematic approach to maximize trust effectiveness.

-

Define clear objectives before selecting trust types. Identify whether you prioritize estate tax reduction, asset protection, probate avoidance, control over distributions, or some combination. Your goals determine which trust structures make sense.

-

Engage qualified professionals with deep trust and estate expertise. General practitioners lack the specialized knowledge required for complex trust planning. Seek attorneys who focus specifically on estate law and tax advisors familiar with trust taxation.

-

Select trust types matching your control preferences and tax strategy. Balance your desire for flexibility against the benefits of irrevocable structures. Consider using multiple trusts for different asset categories or goals.

-

Properly fund trusts by retitling assets into trust ownership. This critical step transfers legal title from your personal name to the trust. Real estate requires new deeds. Investment accounts need beneficiary or ownership changes. Business interests require formal assignment documents.

-

Establish trustee arrangements ensuring competent, trustworthy management. Individual trustees should have financial sophistication and understand your family dynamics. Corporate trustees bring professional management but cost more. Consider co-trustees combining family involvement with professional oversight.

-

Maintain ongoing trust management through regular reviews and updates. Tax laws change. Family circumstances evolve. Review trusts every three to five years to ensure continued alignment with goals and compliance with current regulations.

Pro Tip: Integrate trust planning with your overall investment strategy by coordinating with advisors managing your retirement accounts and other investments to ensure asset allocation remains appropriate across all holdings.

Key management practices include:

- Keeping detailed records of all trust transactions and distributions

- Filing required tax returns for trusts that generate income

- Communicating clearly with beneficiaries about trust terms and expectations

- Documenting trustee decisions and the reasoning behind them

- Reviewing investment performance and adjusting strategies as needed

Proper funding cannot be overemphasized. Many families create trusts but forget to transfer assets into them. The trust provides no benefits for assets still held in your personal name. Work systematically through your asset inventory, transferring each item appropriately.

Consider how trust planning integrates with your broader financial strategy. Coordinate with advisors handling ETF investing or creating your investment plan to ensure trust assets receive appropriate investment management. Trusts are not set-and-forget vehicles. They require active management to deliver sustained benefits.

Regular communication with trustees, beneficiaries, and advisors keeps everyone aligned. Annual meetings review trust performance, discuss any needed adjustments, and address questions or concerns. This proactive approach prevents misunderstandings and ensures trusts operate as intended.

Developing an investment strategy specifically for trust assets requires balancing current beneficiary income needs against preserving principal for future generations. Trustees must navigate these competing interests while meeting fiduciary standards.

Conclusion: Leveraging trust funds for legacy planning

Trust funds represent powerful wealth preservation tools when properly understood and implemented. They offer unmatched flexibility for controlling asset distribution, significant tax advantages through strategic structures, and robust protection for family wealth across generations.

The key to successful trust planning lies in matching trust types to your specific estate goals. Revocable trusts provide management convenience and probate avoidance. Irrevocable and specialized trusts deliver tax savings and asset protection. No single trust structure fits every situation.

Expert guidance remains essential throughout the trust planning process. Estate law complexity and the permanent nature of many trust decisions make professional advice invaluable. Experienced attorneys and tax advisors help you navigate options, avoid costly mistakes, and implement solutions that genuinely protect your legacy.

Taking action sooner rather than later maximizes trust benefits. Estate planning is not something to postpone until retirement or declining health forces decisions. The families who preserve wealth most effectively start planning early, review regularly, and adapt to changing circumstances.

Explore expert resources for trust fund planning

Finblog provides comprehensive resources helping high-net-worth individuals navigate complex estate planning and wealth preservation decisions. Our expert insights clarify sophisticated strategies, making them accessible and actionable.

Explore detailed guides on wealth preservation strategies that complement trust planning with additional protective measures. Learn how to coordinate trusts with insurance, business succession planning, and investment management for comprehensive legacy protection.

Discover proven wealth transfer strategies that minimize taxes while maximizing the wealth passing to your heirs. Our resources help you understand complex regulations and identify opportunities others miss.

Visit Finblog regularly for updated guidance on trust fund selection, estate tax planning, and wealth management best practices. Access the expertise you need to make informed decisions protecting your financial legacy for generations to come.

FAQ

What is a trust fund and how does it work?

A trust fund is a legal arrangement where a trustee holds and manages assets for beneficiaries according to the grantor’s written instructions. The trustee has legal ownership but must use assets solely for beneficiary benefit. This separation of control from beneficial ownership creates powerful planning opportunities.

What are the main differences between revocable and irrevocable trusts?

Revocable trusts let you modify or cancel them anytime during your lifetime but provide no estate tax benefits or asset protection. Irrevocable trusts permanently transfer control to trustees, removing assets from your taxable estate and shielding them from creditors. The choice involves trading flexibility for tax and protection advantages.

How do trust funds help with estate tax minimization?

Irrevocable trusts and specialized structures remove assets from your taxable estate by transferring ownership and control away from you. This reduction in estate value lowers or eliminates estate taxes owed when you die. Properly designed trusts can save millions in taxes for high-net-worth families, preserving significantly more wealth for heirs.

Can a trust fund be changed after it is created?

Revocable trusts can be amended or completely revoked anytime before your death or incapacity. Irrevocable trusts generally cannot be changed without court approval or consent from all beneficiaries. Some modern irrevocable trusts include limited modification provisions, but permanence remains their defining characteristic.

What should I consider when selecting a trustee?

Choose trustees with proven financial management skills, absolute trustworthiness, and clear understanding of your family dynamics and estate goals. Consider whether individual family members, professional corporate trustees, or a combination best serves your situation. Establish clear communication channels and oversight mechanisms to ensure ongoing compliance and effective management.