Most American investors underestimate the complexity of personalized financial planning, even though more than 60% worry about outliving their savings. With higher stakes and uncertain markets, understanding what financial advisors really do becomes crucial for mid-career professionals hoping to secure their financial future. This article uncovers what expert guidance actually offers, clarifying how the right advisor can help you make smarter investment decisions and reach your long-term wealth goals.

Table of Contents

- What Financial Advisors Really Do

- Types of Financial Advisors Explained

- How Advisors Build Wealth and Security

- Costs, Fees, and Value Comparison

- Risks of DIY Investing vs. Professional Help

Key Takeaways

| Point | Details |

|---|---|

| Role of Financial Advisors | Financial advisors provide strategic guidance to help individuals achieve their financial goals through tailored investment strategies and comprehensive planning. |

| Types of Financial Advisors | Different types of financial advisors specialize in various services, including holistic planning, investment management, and wealth management for high-net-worth clients. |

| Cost Structures | Advisors typically charge either fee-only, fee-based, or commission-based fees, impacting the value of the services they provide. |

| Professional vs. DIY Investing | Working with professional advisors mitigates risks associated with emotional decision-making and poor asset allocation compared to DIY investing. |

What Financial Advisors Really Do

Financial advisors serve as professional strategists who help individuals navigate complex financial landscapes and achieve their monetary objectives. Professionals with specialized training play a critical role in translating personal financial goals into actionable investment strategies. Their primary mission involves analyzing an individual’s current financial situation, understanding long-term aspirations, and developing comprehensive plans to bridge the gap between current circumstances and future objectives.

The core responsibilities of financial advisors extend far beyond simple investment recommendations. They conduct thorough assessments of clients’ financial health, which includes evaluating income streams, existing assets, potential risks, and future goals. These professionals provide tailored advice on multiple financial domains, including retirement planning, tax optimization, insurance selection, and investment portfolio management. Their expertise allows them to craft nuanced strategies that align with an individual’s unique risk tolerance, financial constraints, and personal ambitions.

Financial advisors typically operate across several key service areas. Regulatory compliance and professional certifications ensure they maintain high standards of professional conduct. Their service spectrum includes portfolio construction, asset allocation, retirement planning, estate planning, and providing ongoing financial education. Some advisors specialize in specific niches like retirement strategies, wealth preservation for high-net-worth individuals, or targeted investment approaches for particular life stages.

Pro tip: Before selecting a financial advisor, request a comprehensive overview of their fee structure, professional credentials, and a sample financial plan to ensure alignment with your specific financial goals.

Types of Financial Advisors Explained

Financial advisors represent a diverse professional landscape with multiple specialized roles and expertise levels. Investment advisers and financial professionals operate across different service models, each designed to meet specific client needs and financial objectives. These professionals can be categorized based on their primary service offerings, regulatory registrations, and areas of specialization.

The primary categories of financial advisors include certified financial planners (CFPs), registered investment advisers (RIAs), wealth managers, and insurance agents. Certified financial planners typically provide comprehensive financial planning services, offering holistic guidance on retirement, investments, tax strategies, and estate planning. Registered investment advisers focus primarily on investment management, providing portfolio construction and asset allocation recommendations. Wealth managers cater to high-net-worth individuals, offering more personalized and complex financial strategies that often include tax planning, estate management, and intergenerational wealth transfer.

Financial advisors come in various specialized forms, ranging from those who work on commission by selling financial products to fee-based professionals who provide objective advice. Some advisors specialize in specific client demographics, such as retirement planning for teachers, investment strategies for small business owners, or financial guidance for young professionals. Their compensation structures vary widely, including fee-only models, commission-based approaches, or hybrid arrangements that combine both fee and commission income.

Here is a comparison of the main financial advisor types and their typical clients:

| Advisor Type | Primary Focus | Typical Clients |

|---|---|---|

| Certified Financial Planner (CFP) | Holistic planning and guidance | Individuals and families |

| Registered Investment Adviser (RIA) | Investment management and allocation | General investors |

| Wealth Manager | Complex wealth strategies | High-net-worth individuals |

| Insurance Agent | Insurance product solutions | Those seeking risk management |

Pro tip: Always verify a financial advisor’s credentials, ask about their specific areas of expertise, and understand their complete fee structure before establishing a professional relationship.

How Advisors Build Wealth and Security

Financial advisors employ sophisticated strategies to help clients systematically build and protect their wealth through comprehensive financial planning. These professionals go beyond simple investment recommendations, developing holistic approaches that address individual financial challenges, risk tolerance, and long-term objectives. By creating personalized roadmaps, advisors help clients navigate complex financial landscapes, transforming abstract financial goals into actionable strategies.

The wealth-building process involves multiple strategic components. Advisors conduct thorough financial assessments, identifying potential growth opportunities while simultaneously implementing risk mitigation techniques. They help clients diversify investment portfolios, optimize tax strategies, and create sustainable income streams. This multifaceted approach includes developing retirement plans, managing investment allocations, analyzing potential investment vehicles, and providing ongoing financial education that empowers clients to make informed decisions.

Technological advancements and evolving market dynamics have transformed how financial advisors approach wealth creation. Modern advisors leverage sophisticated analytical tools, data-driven insights, and predictive modeling to craft more precise and personalized financial strategies. They focus on understanding each client’s unique financial ecosystem, considering factors like career trajectory, family dynamics, risk appetite, and long-term aspirations. By combining deep financial expertise with cutting-edge technology, advisors can develop more nuanced and adaptive wealth-building approaches that respond dynamically to changing economic conditions.

Pro tip: Request a comprehensive financial diagnostic from your advisor that maps your current financial health against your future wealth objectives, ensuring a truly personalized strategic approach.

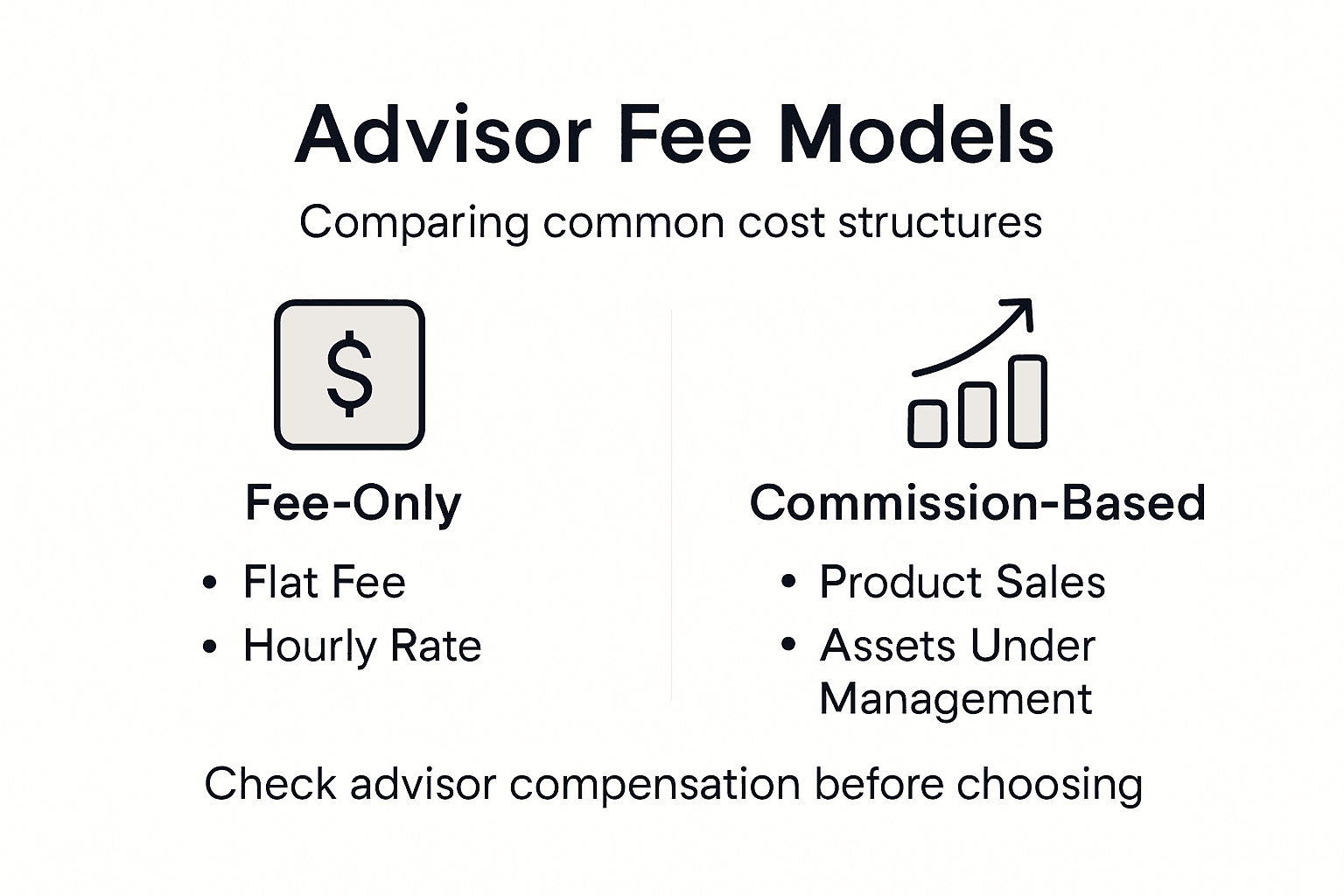

Costs, Fees, and Value Comparison

Financial advisory fee structures represent a complex landscape of compensation models that directly impact the value and transparency of financial guidance. Investors must understand the nuanced approaches advisors use to charge for their services, which typically include asset-based percentages, flat annual fees, hourly rates, and commission-based arrangements. Each model carries distinct advantages and potential conflicts of interest that can significantly influence the quality and objectivity of financial recommendations.

The primary compensation models for financial advisors include fee-only, fee-based, and commission-based structures. Fee-only advisors charge clients directly through transparent pricing mechanisms, typically calculating fees as a percentage of managed assets or through predetermined flat rates. These advisors operate as fiduciaries, legally obligated to prioritize client interests. Fee-only compensation models are often considered the most ethical, as they minimize potential conflicts of interest that might arise from product sales commissions. Commission-based advisors, conversely, earn money by selling specific financial products, which can potentially compromise the objectivity of their recommendations.

Investors should carefully evaluate the total cost of financial advice against the potential value generated. While advisory fees might seem substantial, a skilled financial advisor can potentially generate returns that substantially outweigh their costs through strategic investment selection, tax optimization, risk management, and comprehensive financial planning. Typical advisory fees range from 0.5% to 1.5% of managed assets annually, with more specialized or high-touch services potentially commanding higher rates. The key is to understand not just the cost, but the comprehensive value an advisor brings to your financial journey.

Pro tip: Always request a detailed breakdown of all potential fees and ask how your advisor’s compensation model might influence their recommendations.

Risks of DIY Investing vs. Professional Help

Common investor mistakes reveal the significant challenges individual investors face when managing their own portfolios. DIY investing might seem appealing, offering a sense of control and potential cost savings, but it often leads to costly errors that can dramatically undermine long-term financial performance. Inexperienced investors frequently struggle with complex market dynamics, emotional decision-making, and a lack of comprehensive financial strategy that professional advisors inherently provide.

The primary risks of DIY investing include emotional trading, poor asset allocation, insufficient diversification, and unrealistic return expectations. Without professional guidance, individual investors are more likely to make reactive decisions during market volatility, selling assets at precisely the wrong moment or failing to rebalance portfolios strategically. Investment professionals help mitigate these risks by providing disciplined, objective approaches that transcend individual emotional impulses. They offer systematic investment strategies grounded in comprehensive research, risk assessment, and long-term financial planning that most individual investors cannot consistently replicate.

Professional financial advisors bring specialized expertise that goes beyond simple investment selection. They help clients develop nuanced financial strategies tailored to individual goals, risk tolerances, and life circumstances. Advisors provide ongoing portfolio management, tax optimization strategies, and proactive adjustments that adapt to changing market conditions and personal financial landscapes. Their comprehensive approach helps investors avoid common pitfalls like under-diversification, speculative trading, and making investment decisions based on short-term market noise rather than long-term financial objectives.

This table summarizes key differences between DIY investing and working with a professional advisor:

| Aspect | DIY Investing | Professional Advisor |

|---|---|---|

| Decision-Making | Self-directed, may be emotional | Objective, research-driven |

| Risk Management | Limited understanding | Comprehensive strategies |

| Portfolio Diversification | Often insufficient | Regularly rebalanced |

| Long-term Planning | Sporadic, inconsistent | Structured, goal-based |

| Cost Structure | Lower fees, higher potential mistakes | Fees, but risk mitigation and expertise |

Pro tip: Before attempting DIY investing, honestly assess your financial knowledge, time availability, and emotional discipline to determine whether professional guidance might ultimately save you money and reduce investment stress.

Unlock Your Full Wealth Potential with Expert Financial Guidance

Navigating complex financial decisions alone can lead to costly mistakes like emotional trading and insufficient diversification as detailed in “Benefits of Financial Advisors: Maximizing Wealth Outcomes.” If you are seeking to build wealth with confidence while avoiding common investor pitfalls such as poor asset allocation or lack of long-term planning you need tailored strategies that adapt to your unique goals and risk tolerance. With professional advice rooted in comprehensive financial planning and transparent fee structures you gain disciplined insights that help bridge the gap between your current financial position and the secure future you envision.

Discover how partnering with seasoned financial experts transforms your investment approach through objective, research-driven methods. Take the first step towards maximizing your financial outcomes by visiting finblog.com where you can explore essential resources and access personalized consultations designed to empower your wealth journey. Get started today to protect your assets, optimize your portfolio, and craft a purpose-built strategy that grows with you.

Frequently Asked Questions

What are the primary benefits of hiring a financial advisor?

Hiring a financial advisor can maximize wealth outcomes through personalized investment strategies, comprehensive financial planning, risk management, and ongoing education that help you achieve your financial goals more effectively.

How do financial advisors build wealth for their clients?

Financial advisors build wealth by conducting thorough financial assessments, optimizing tax strategies, managing investments, and creating diversified portfolios tailored to individual risk tolerance and long-term objectives.

What types of financial advisors are there, and how do they differ?

There are various types of financial advisors, including certified financial planners (CFPs), registered investment advisers (RIAs), wealth managers, and insurance agents. They differ in focus areas, client types, and compensation structures, impacting the services they provide.

How can I evaluate the costs and fees associated with financial advisors?

To evaluate costs, request a detailed breakdown of fees, understand compensation models (fee-only, fee-based, commission-based), and assess how these fees relate to the potential value of the advice and services received.

Recommended

- Role of Financial Advisors – Impact on Your Wealth – Finblog

- Wealth Management Explained: Complete Guide – Finblog

- How to Build Wealth: Proven Steps for Lasting Financial Success – Finblog

- Master Building an Investment Portfolio for Profits – Finblog

- Top 5 Gold Companies 2025 | Best Gold IRA Companies