The FED still talks about cutting rates, but rising inflation risks and the oil shock are quietly shifting the conversation, and a rate hike is now a real possibility.

Officially, the Federal Reserve remains in easing mode. Policymakers continue to signal that rates could come down later this year, as long as inflation keeps falling. But as The Wall Street Journal points out, the mood in markets and among economists has clearly changed.

Investors are no longer confident that cuts are coming. Instead, they are starting to ask a different question: what if the Fed has to raise rates again?

The Shift in One Sentence

The story used to be simple: inflation is falling, so rates will go down.

Now it looks more like this:

- Inflation is stuck above target

- Oil prices are rising again

- Policy is already less restrictive than before

That combination is what’s changing expectations.

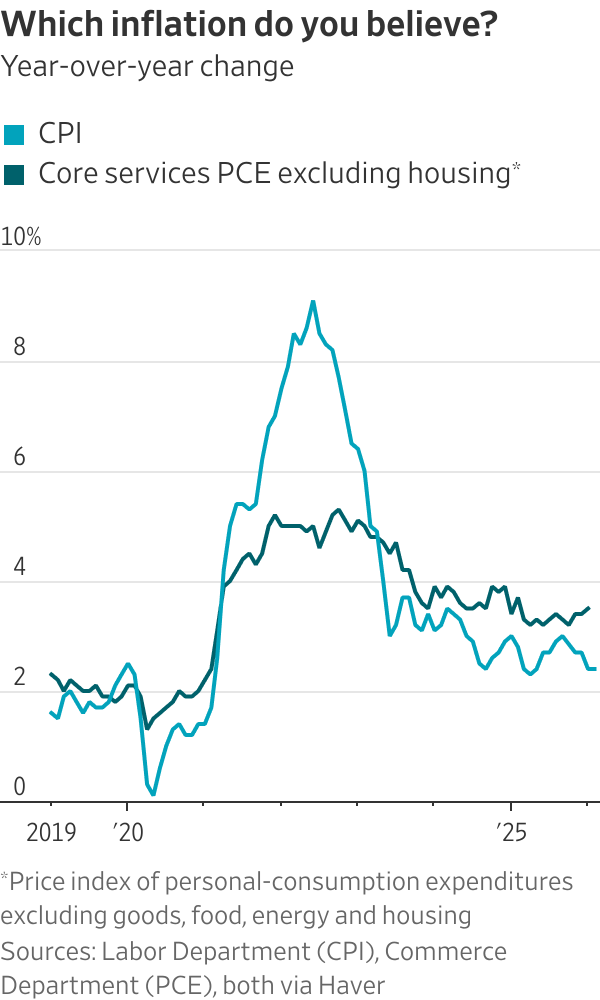

Inflation Is Still the Core Problem

At first glance, inflation doesn’t look alarming. But the deeper data tells a more stubborn story.

- Headline inflation is around 2.4%

- The Fed’s preferred measure is closer to 2.8%

- Core inflation is still above 3%

More importantly, key underlying categories haven’t improved much in the past year. That’s what worries policymakers.

As noted in the The Wall Street Journal analysis, the Fed had been relying on the idea that inflation would gradually cool on its own. But that process has stalled, raising doubts about whether current policy is tight enough.

Then Came the Oil Shock

Just as inflation was proving sticky, the Iran war added a new layer of risk.

Higher oil prices matter because they:

- Push up costs across the economy

- Feed into transport, food, and services

- Make it harder for inflation to fall

Normally, the Fed might ignore a temporary energy spike. But this time, the economy is still holding up, which means inflation pressure could last longer than expected.

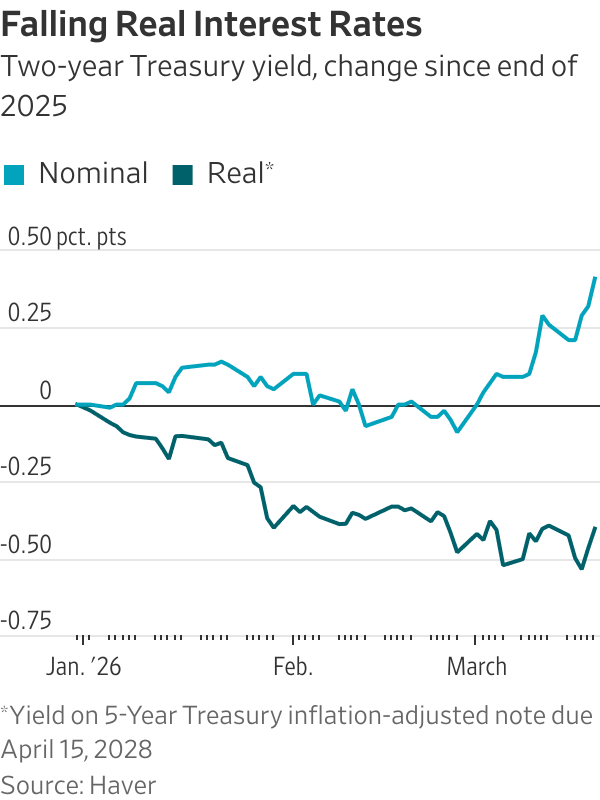

Policy Might Not Be Tight Enough

Another important piece of the puzzle is where rates stand today.

The Fed has already cut rates significantly since 2024. Now, they are only slightly above what economists call the “neutral” level, meaning they are no longer strongly restraining the economy.

There is also a subtle but important dynamic at play:

- If inflation rises while rates stay the same → real rates fall

- Lower real rates → easier financial conditions

So even without cutting, policy may already be loosening in real terms. That’s one reason some economists think a hike could eventually be needed.

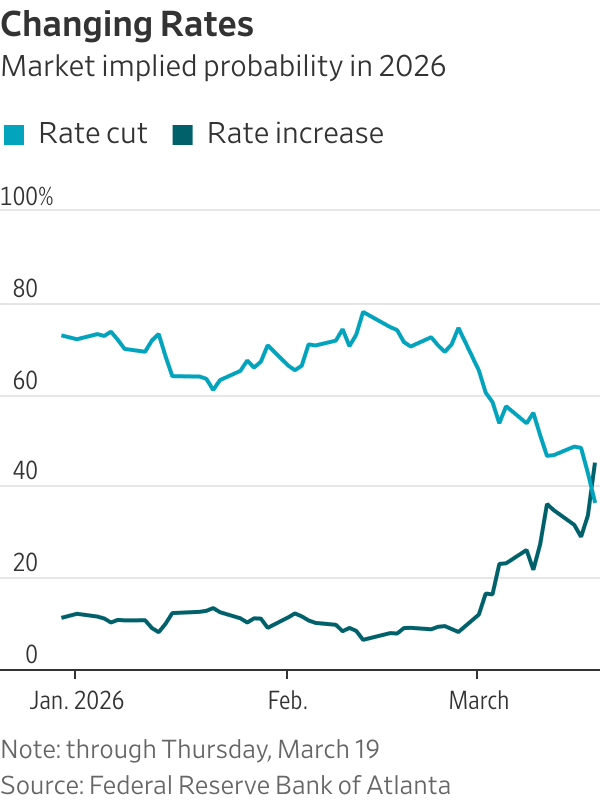

Markets Are Starting to Reflect This

You can see the shift clearly in expectations:

- Probability of a rate cut has fallen sharply

- Probability of a rate hike has risen significantly

This doesn’t mean a hike is coming soon. But it shows that investors are no longer fully convinced by the Fed’s easing narrative.

Why the Fed Is Still Waiting

Despite all this, a rate hike is not the main scenario right now.

There are still reasons for caution:

- Inflation could resume falling as temporary factors fade

- The labor market is stable, not overheating

- A prolonged war could eventually slow the economy

In other words, the Fed is not ready to react aggressively yet.

The Fed is caught in a difficult position. It wants to cut rates, but: Inflation isn’t falling fast enough, Oil prices are rising, Financial conditions are already easing

As the The Wall Street Journal highlights, the conversation is no longer just about when rate cuts will happen.

For the first time in months, the risk is that the next move might not be a cut at all.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related: Fed’s Best Move Now? Do Nothing