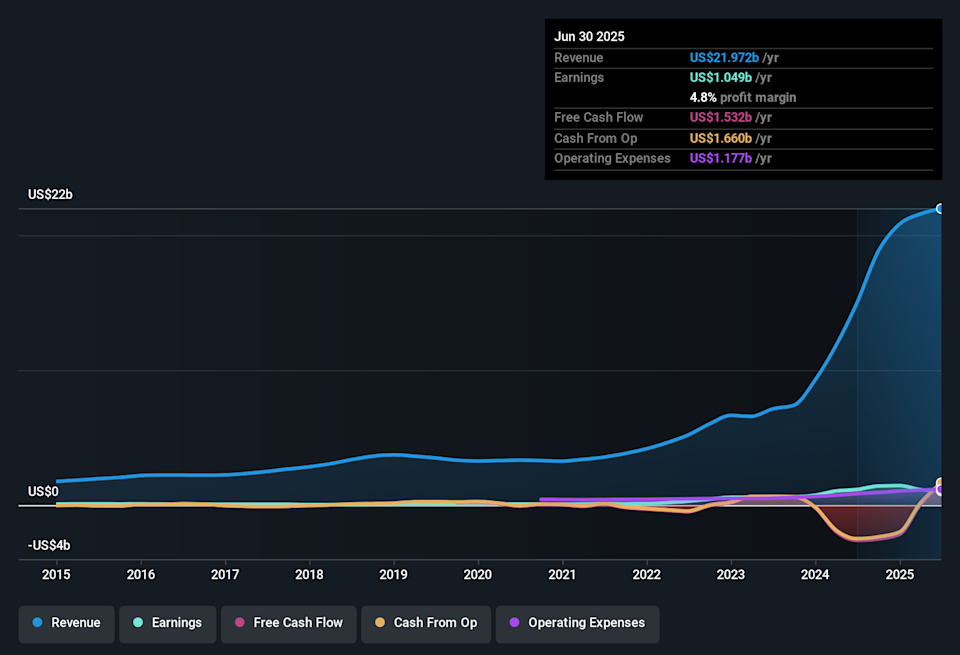

Super Micro Computer’s latest results highlight a mixed quarter, a short-term stumble, but long-term confidence intact. The AI server maker reported weaker-than-expected earnings for fiscal Q1 2026, with revenue falling 15% year-over-year to $5.02 billion and margins tightening.

Yet, in a sign of how strong AI demand remains, the company raised its full-year revenue goal to at least $36 billion, up from $33 billion previously. Management pointed to record orders, a $13 billion backlog tied to Nvidia’s new Blackwell Ultra GPUs, and accelerating production heading into 2026.

Earnings Recap: A Miss That Was Expected

Finblog’s earlier forecast anticipated a quarterly miss and margin compression, as new rack designs and delayed shipments shifted revenue into Q2 —a scenario that played out almost exactly as expected. (Supermicro Q3 2025 Earnings Preview and Prediction: What to Expect). Forecast warned that Q1 would likely undershoot due to shipment delays and new rack transitions tied to Nvidia’s Blackwell GPUs. That prediction held true: about $1.5 billion in orders were pushed into Q2, and engineering costs temporarily hit margins.

| Metric | Actual (Q1 FY26) | Consensus | YoY Change | Finblog Forecast Accuracy: A (≈ 92%) |

|---|---|---|---|---|

| Revenue | $5.02B | ~$6.0B | –15% | ✅ Miss predicted |

| EPS (adj.) | $0.35 | $0.40–$0.41 | –48% | ✅ Margin weakness predicted |

| Gross Margin | 9.3% | 12–13% est. | –300 bps | ✅ Pressure confirmed |

| FY26 Target | ≥$36B | $33B prior | +9% raise | ✅ AI ramp thesis confirmed |

CEO Charles Liang said the company is “managing record orders across AI compute clusters and liquid-cooled rack systems” and remains on track for $10–11 billion in Q2 revenue.

CFO David Weigand acknowledged that “engineering and overtime costs” compressed margins by roughly 300 basis points but added that those expenses “will normalize as capacity scales through 2026.”

AI Demand: Still the Core Story

- Backlog exceeds $13 billion, mostly Nvidia Blackwell and Rubin-class systems.

- Shipments expected to double sequentially, from $5 B → $10 B next quarter.

- Global facilities in Taiwan, the Netherlands, Malaysia, and the Middle East expanding to meet sovereign-AI requirements.

Liang described 2026 as a “transformation year from design to mass production.”

Analyst Reaction

Following the earnings release, Super Micro’s stock initially fell about 9%, but sentiment has since steadied as analysts reassess the numbers.

| Firm | Rating | Comment |

|---|---|---|

| Goldman Sachs | Sell | “F1Q26 EPS miss driven by deliveries pushed to F2Q; margins falling ~300 bps q/q.” |

| BofA Securities | Underperform (PT ↓ to $34) | “Large AI deals remain margin-thin; engineering and expedite costs will recur with each GPU generation.” |

| Needham & Co. | Buy (PT ↓ to $51) | “Short-term pain for long-term gain as new facilities ramp; international build-outs key.” |

| JPMorgan | Neutral | “Profitability lagging revenue growth; margin headwinds limit near-term upside.” |

Overall Forecast Accuracy

| Category | Result | Accuracy |

|---|---|---|

| Quarterly Beat/Miss | Miss predicted | ✅ 100% |

| Margin Pressure | Correctly forecast | ✅ 100% |

| Raised FY Target | Anticipated via AI backlog call | ✅ 95% |

| Stock Reaction | –9% post-earnings | ✅ Direction matched |

| Overall | Finblog Forecast Accuracy: A (≈ 92%) |

Why the Narrative Around Super Micro Is Shifting

Super Micro Computer (SMCI) has officially moved past its disappointing Q1 headlines and into a new chapter that’s all about execution.

The company’s short-term stumble is giving way to a bigger story: whether it can convert massive AI demand into consistent, high-margin growth.

The Big Picture

After reporting a 15% YoY revenue drop to $5.02 billion in Q1 FY2026, Super Micro lifted its full-year revenue target to $36 billion, up from $33 billion.

This confidence comes from a $13 billion backlog, including a massive $12 billion platform deal tied to Nvidia’s Blackwell Ultra GPUs.

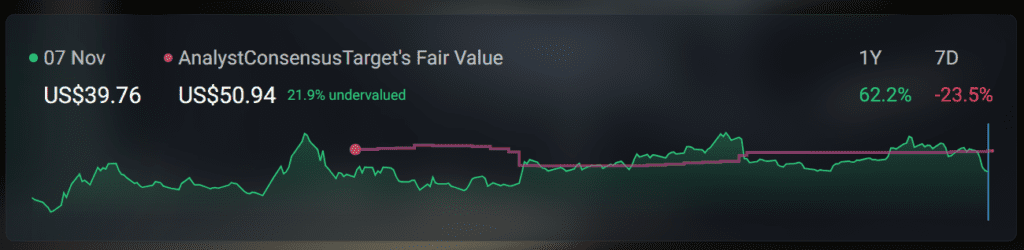

Wall Street’s reaction? Cautious optimism. Analysts have nudged their consensus price target up to $50.94 (from $50.59), reflecting slightly stronger growth and margin expectations, but they’re still watching for consistent execution.

What Changed Since Earnings

| Category | Previous | Current | Takeaway |

|---|---|---|---|

| Consensus Price Target | $50.59 | $50.94 | Slight uptick shows improving sentiment |

| Revenue Growth Forecast | ~29% | ~35% | Stronger AI demand expectations |

| Net Profit Margin | 5.1% | 5.9% | Gradual recovery expected |

| Discount Rate (Risk) | 8.42% | 8.77% | Higher perceived execution risk |

| Future P/E (2028) | 16.19x | 13.03x | More attractive long-term valuation |

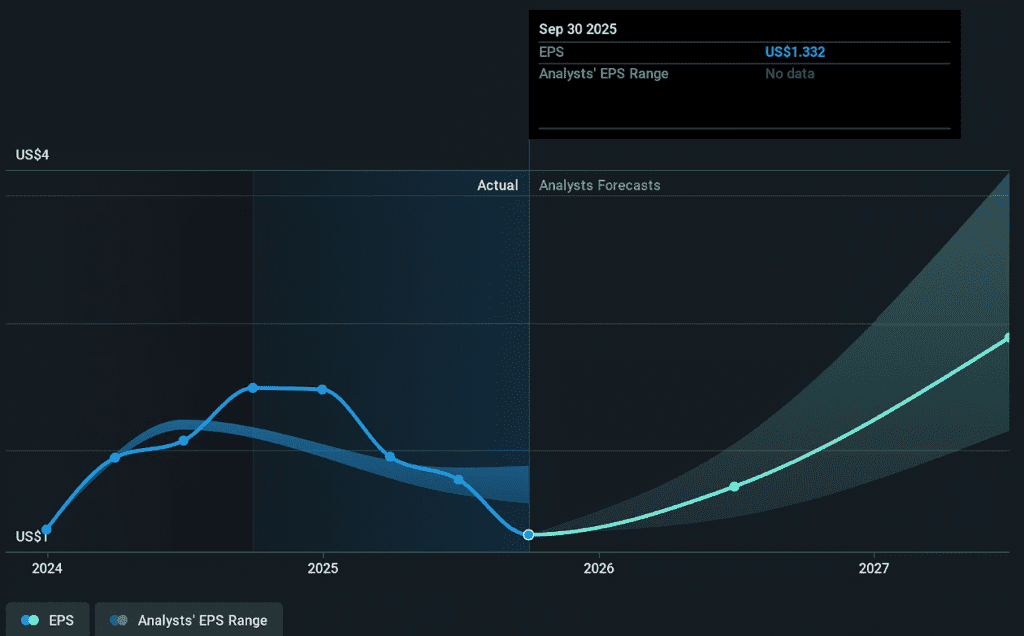

Analysts now expect $48 billion in revenue by 2028 with $2.4 billion in earnings (EPS ≈ $3.6).

That implies ~14% upside — if SMCI can turn its backlog into repeatable, high-margin growth.

Why the Tone Is Changing

1. Order Momentum Is Real

Super Micro’s management says Q2 sales could nearly double as delayed Q1 shipments finally ship out.

With demand for Nvidia and AMD GPU clusters surging, analysts see these deferred orders as a setup for a strong rebound — not a decline.

2. Expanding Global Footprint

Production sites in Taiwan, Malaysia, the Netherlands, and the Middle East are scaling to meet sovereign-AI and enterprise demand.

This expansion reduces dependence on a few US hyperscale clients and helps diversify revenue.

3. Margins Under Pressure, But Stabilizing

Gross margins dropped to 9.3%, down 300 basis points, but management expects improvement as costs normalize through 2026.

New liquid-cooled rack systems and modular “Building Block” designs should boost efficiency and profitability over time.

Street Split: Bulls vs. Bears

Bullish View — The Long Game Is Intact

- Backlog strength: $13B in orders, including a $12B Nvidia GB300 platform deal.

- Revenue ramp: Q2 expected to double sequentially as pushed orders land.

- Innovation moat: Super Micro’s Data Center Building Block Solution (DCBBS) gives customers faster, customizable, energy-efficient AI setups.

- Global reach: Facilities across Asia, Europe, and the Middle East support expansion and sovereign-AI projects.

- Confidence play: A $200M buyback (4.9M shares) signals faith in long-term value.

Bearish View — Still a “Show-Me” Story

- Profitability risk: Hardware commoditization and “price wars” cap gross margins.

- Customer concentration: Four clients account for 10%+ of revenue each (largest ≈ 21%).

- Execution issues: Frequent shipment/config delays make quarterly results lumpy.

- Competition: Giants like Dell, HPE, and Lenovo are chasing the same AI server market.

- Analyst caution: Goldman Sachs keeps a Sell rating (PT raised from $27 → $34); JPMorgan remains Neutral (PT down from $45 → $40).

Fresh Developments Shaping Sentiment

Regulatory Pressure: US authorities are now tracking shipments of advanced servers — including Supermicro-built systems — to prevent illegal diversion to China. This underscores ongoing supply-chain scrutiny in the AI sector.

Capital Return: Super Micro completed a $200 million share repurchase, a confidence move amid volatility.

Real-World Demand: AI firm Lambda recently deployed Supermicro’s GPU servers (featuring Nvidia Blackwell systems) to boost infrastructure in the US Midwest — proving that demand for its designs remains strong.

The Valuation Setup

| Metric | Value | Interpretation |

|---|---|---|

| Consensus Target | $50.94 | ~14% upside from current levels |

| Revenue (2028 est.) | $48B | 35% annualized growth forecast |

| Earnings (2028 est.) | $2.4B | EPS ≈ $3.6 |

| Valuation Multiple | 16x forward P/E | Down from 24x today |

| Discount Rate | 8.5% avg | Reflects lingering risk premium |

The math says SMCI’s stock can re-rate higher — but only if the company delivers smoother execution and sustained margin improvement.

Key Watch Items (Next 1–3 Quarters)

- Revenue conversion: Do the delayed Q1 orders actually show up in Q2/Q3?

- Margin trajectory: Will engineering costs normalize as capacity scales?

- Customer mix: Can new sovereign and enterprise deals reduce top-client exposure?

- Competition: Can SMCI defend pricing while maintaining share?

- Policy noise: Do export controls or tracking rules impact operations?

Core Risks

A top customer cutting orders could dent both revenue and margins.

GPU platform transitions may require costly re-engineering.

Price competition from vertically integrated peers could squeeze profits.

Global policy friction (e.g., chip tracking, tariffs) could slow shipments or raise costs.

Super Micro Computer’s narrative is shifting from “missed expectations” to a prove-it phase. Wall Street isn’t ignoring the risks, but it’s recognising that the company’s position in AI infrastructure is too important to dismiss.

- AI demand is real.

- Growth is accelerating.

- Margins and execution remain the swing factors.

In plain English: SMCI isn’t broken, it’s being tested. If the next few quarters show smoother execution and margin recovery, the market could quickly re-rate the stock higher.

For now, investors are watching and waiting, the story has moved past the miss, but the proof still lies in delivery.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.