Most American investors discover that only a small set of portfolio metrics consistently separates top performers from the rest. With volatile market cycles and growing international exposure, understanding the right performance metrics is now more crucial than ever for both American and global finance professionals. This guide breaks down the sophisticated methods that drive smarter investment decisions, offering practical tools to translate complex data into meaningful, actionable insights.

Table of Contents

- Defining Portfolio Performance Metrics

- Types of Metrics and Their Applications

- Calculation Methods and Key Features

- Comparing Benchmarks and Industry Standards

- Risks and Limitations of Performance Analysis

Key Takeaways

| Point | Details |

|---|---|

| Understanding Metrics | Portfolio performance metrics are essential for assessing return generation, risk management, and market performance. Use them to make informed investment decisions. |

| Types of Metrics | Differentiate between conventional metrics and risk-adjusted metrics to gain a comprehensive view of portfolio performance. Each type serves a unique analytical purpose. |

| Benchmark Comparisons | Always compare portfolio performance against appropriate benchmarks for context, and use multiple metrics for a nuanced understanding of effectiveness. |

| Recognizing Limitations | Be aware that performance metrics have limitations, particularly with historical data. A comprehensive analysis includes multiple perspectives and mitigates methodological risks. |

Defining Portfolio Performance Metrics

Portfolio performance metrics represent sophisticated analytical tools investors use to evaluate investment strategy effectiveness. These metrics transform complex financial data into clear, actionable insights about portfolio health, measuring investment portfolio dynamics.

At their core, portfolio performance metrics track three fundamental dimensions: return generation, risk management, and comparative market performance. Investors rely on these metrics to understand how their investment selections perform against benchmarks, assess potential risks, and make data driven reallocation decisions. Key metrics include total return percentage, risk adjusted return ratios like Sharpe ratio, standard deviation of returns, and alpha performance indicators.

Traditional performance metrics go beyond simple return calculations. They incorporate sophisticated analysis techniques that consider multiple variables such as volatility, correlation between assets, and sector specific performance trends. Advanced investors often use comparative metrics like beta coefficient to understand how individual investments respond to broader market movements, enabling more nuanced portfolio management strategies.

Pro tip: Regularly review your portfolio performance metrics quarterly to detect emerging trends and make proactive investment adjustments before significant market shifts occur.

Types of Metrics and Their Applications

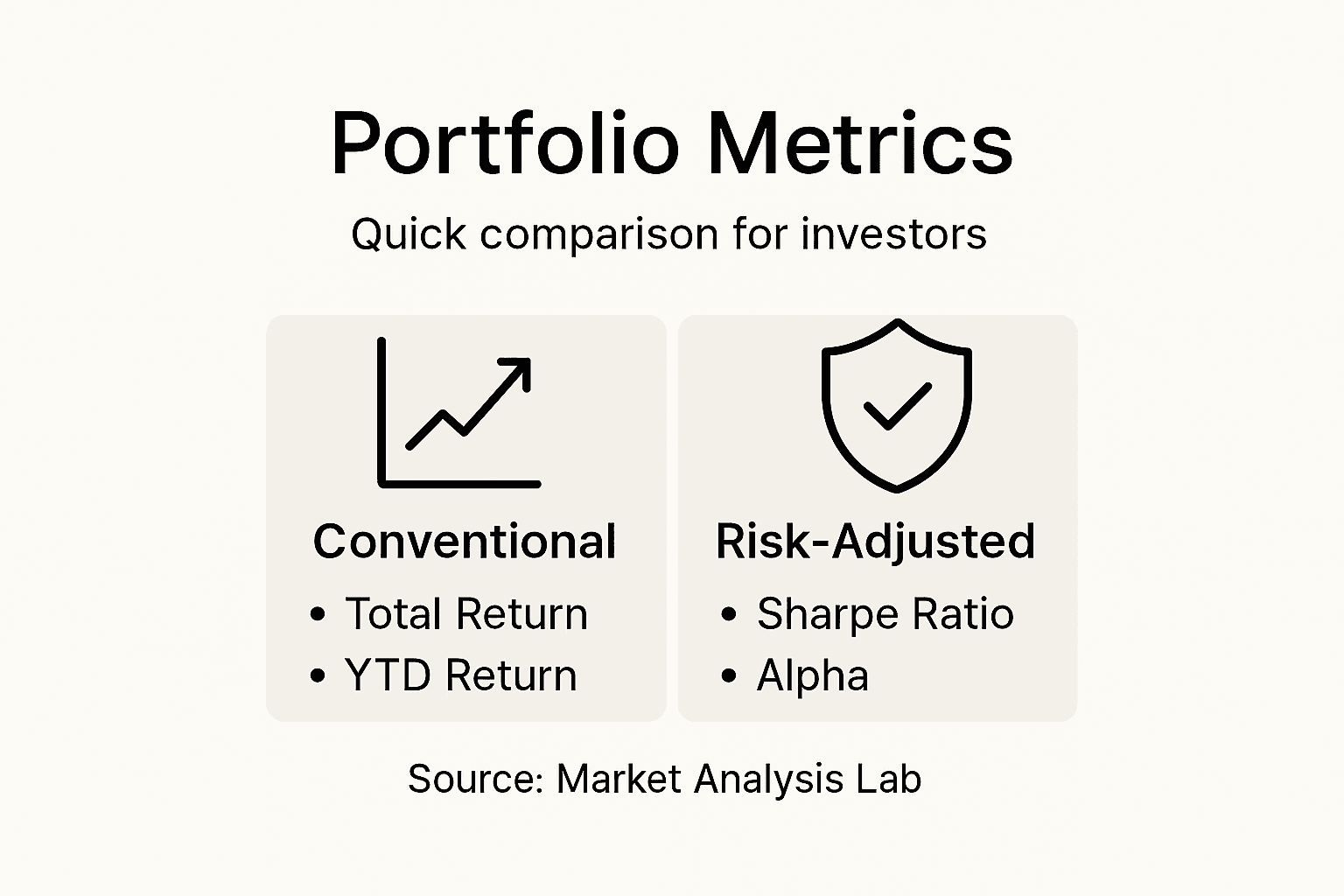

Portfolio performance metrics are systematically divided into two primary categories: conventional and risk-adjusted evaluation methods. Each category serves distinct analytical purposes, enabling investors to comprehensively assess investment performance from multiple perspectives.

Conventional metrics focus on raw financial performance, including total return, cumulative return, and year-to-date performance. These straightforward calculations provide a baseline understanding of portfolio growth. Risk-adjusted metrics, conversely, introduce sophisticated nuance by incorporating risk factors into performance assessment. Key risk-adjusted metrics include the Sharpe ratio, which measures return relative to volatility, the Treynor ratio that evaluates returns against systematic market risk, and Jensen’s alpha, which assesses portfolio manager skill in generating excess returns.

Advanced investors often employ a combination of these metrics to develop a holistic view of portfolio performance. For instance, the Sharpe ratio helps compare investment strategies with different risk profiles, while Jensen’s alpha reveals whether a portfolio manager consistently outperforms market benchmarks. Sophisticated performance evaluation requires understanding the strengths and limitations of each metric, recognizing that no single indicator provides a complete picture of investment performance.

Here’s how common portfolio performance metrics compare:

| Metric | Purpose | Key Strength | Main Limitation |

|---|---|---|---|

| Total Return | Measures overall gain/loss | Simple to calculate | Ignores risk and volatility |

| Sharpe Ratio | Assesses return per unit of risk | Compares risk-adjusted return | Assumes normal returns |

| Treynor Ratio | Evaluates return vs. market risk | Useful for diversified portfolios | Only considers systematic risk |

| Jensen’s Alpha | Measures excess return vs. benchmark | Highlights manager skill | Depends on accurate benchmark |

| Standard Deviation | Quantifies volatility | Reveals volatility magnitude | Reflects only past performance |

Pro tip: Cross-reference multiple performance metrics to develop a more comprehensive understanding of your investment strategy’s true effectiveness.

Calculation Methods and Key Features

Calculating portfolio performance metrics requires precise mathematical techniques that transform raw financial data into meaningful insights. While no single calculation method provides a complete performance picture, investors can leverage multiple approaches to gain comprehensive understanding.

The primary calculation methods include time-weighted return (TWR) and money-weighted return (MWR). Time-weighted return neutralizes the impact of external cash flows by segmenting portfolio performance into specific time periods, making it ideal for comparing investment manager performance. Money-weighted return, conversely, accounts for the specific timing and size of cash contributions and withdrawals, providing a more personalized performance perspective that reflects actual investor experience.

Key calculation features involve several critical mathematical components. Investors must consider factors like dividend reinvestment, transaction costs, and inflation adjustments when computing performance metrics. Advanced calculation techniques incorporate complex statistical methods such as standard deviation to measure return volatility, beta coefficients to assess market correlation, and regression analysis to understand systematic risk exposure. These sophisticated approaches transform raw numerical data into actionable investment intelligence, enabling more nuanced strategic decision making.

Pro tip: Use standardized financial calculators and spreadsheet tools to ensure consistent and accurate portfolio performance metric calculations.

Comparing Benchmarks and Industry Standards

Comparing portfolio performance against established benchmarks is a critical analytical process that provides context and meaningful evaluation. Benchmark comparison techniques enable investors to assess their investment strategies relative to market performance, providing a standardized framework for understanding portfolio effectiveness.

Traditional benchmarking involves selecting appropriate market indexes that closely match an investment portfolio’s composition and risk profile. For U.S. equity investments, the S&P 500 serves as a standard reference point, while international portfolios might utilize MSCI indexes or region-specific market benchmarks. Advanced investors recognize that simply comparing raw returns is insufficient, necessitating sophisticated risk-adjusted comparison methods that account for volatility, systematic risk, and market correlation.

Below is a summary of benchmark selection and its importance:

| Benchmark Type | Typical Use Case | When To Choose |

|---|---|---|

| S&P 500 Index | U.S. equity portfolios | Domestic large-cap allocations |

| MSCI EAFE Index | International equity exposure | Global or region-specific equities |

| Custom Composite | Mixed-asset portfolios | Unique asset blends or strategies |

| Risk-Free Rate (e.g., T-bill) | Comparing risk premium | Calculating ratios like Sharpe |

Industry standards recommend comprehensive benchmark evaluation using multiple metrics. Sophisticated investors employ tools like the Sharpe ratio, which compares portfolio returns against risk-free rates, and the Treynor ratio, which measures excess returns relative to systematic market risk. These advanced techniques transform benchmark comparisons from simple numerical comparisons into nuanced performance assessments that reveal true investment strategy effectiveness.

Pro tip: Select benchmarks that precisely match your portfolio’s asset allocation and investment strategy to ensure meaningful performance comparisons.

Risks and Limitations of Performance Analysis

Performance analysis metrics, while powerful, come with inherent limitations that investors must carefully navigate. Historical performance provides insights, but does not guarantee future results, creating a fundamental uncertainty in investment strategy evaluation.

Critical limitations emerge from several key factors. Performance metrics often rely on past data, which may not accurately predict future market conditions. Statistical measures like standard deviation and beta coefficients represent historical volatility, potentially misrepresenting future risk profiles. Additionally, benchmarking techniques can create misleading comparisons when portfolio compositions differ significantly from market indexes, leading investors to draw incorrect conclusions about investment performance.

Methodological challenges further complicate performance analysis. Complex metrics like the Sharpe ratio assume normal distribution of returns, which rarely occurs in real market conditions. Transaction costs, tax implications, and inflation are frequently overlooked in standard performance calculations. Investors must recognize that no single metric provides a comprehensive view of portfolio health. Sophisticated analysis requires integrating multiple perspectives, understanding contextual nuances, and acknowledging the probabilistic nature of investment returns.

Pro tip: Always consider multiple performance metrics and qualitative factors to develop a more holistic understanding of your investment strategy.

Unlock the True Power of Your Portfolio Performance Metrics

Struggling to interpret complex portfolio performance metrics like Sharpe ratio or Jensen’s alpha? You are not alone. Many investors face the challenge of translating these detailed analytics into confident investment decisions. If you want to move beyond simple return numbers and understand the real risk management and benchmark comparisons behind your portfolio’s success you need expert guidance tailored to these exact metrics.

Discover how to gain control over your investment strategy by mastering key performance indicators with personalized support from finblog.com. Our financial consulting solutions are designed to help serious investors analyze risk-adjusted returns and benchmark comparisons with clarity. Don’t let uncertainty hold back your portfolio growth. Take action now by visiting finblog.com and explore resources that will empower your investment decisions with data-driven confidence. Your next step toward smarter investing starts here.

Frequently Asked Questions

What are portfolio performance metrics?

Portfolio performance metrics are analytical tools that help investors evaluate the effectiveness of their investment strategies by tracking return generation, risk management, and comparative market performance.

Why should I use risk-adjusted performance metrics?

Risk-adjusted performance metrics, such as the Sharpe ratio and Treynor ratio, provide a more nuanced view of portfolio performance by considering the risk taken to achieve returns, helping investors evaluate investment strategies with different risk profiles.

How do I calculate my portfolio’s performance?

You can calculate portfolio performance using methods like time-weighted return (TWR) and money-weighted return (MWR), along with key features such as dividend reinvestment, transaction costs, and inflation adjustments to ensure your calculations reflect true performance.

How do benchmarks impact portfolio performance evaluation?

Comparing your portfolio performance against relevant benchmarks helps you understand how well your investment strategy is performing in relation to the market, guiding you to make informed decisions about reallocation and strategy adjustments.

Recommended

- Master Building an Investment Portfolio for Profits – Finblog

- 7 Safe Investment Options for Your Financial Future – Finblog

- Understanding Tax Efficient Investing: How It Works – Finblog

- Understanding the Tax Implications of Investing – Finblog

- AI Investment Management Platform for Automated Portfolio Management