Managing a portfolio often means balancing growth with risk, especially when leveraging borrowed capital. For mid-career finance professionals worldwide, mastering financial leverage is crucial for maximizing returns and improving asset utilization without exposing investments to unnecessary danger. This guide clarifies key leverage concepts, core ratios, and practical strategies so you can make smarter capital structure decisions and confidently align your approach with international standards.

Table of Contents

- Defining Financial Leverage And Key Concepts

- Main Types And Real Applications Explained

- How Financial Leverage Works In Practice

- Risks, Costs, And Common Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Financial Leverage | Financial leverage uses borrowed capital to amplify investment returns, requiring careful risk assessment. |

| Key Ratios for Monitoring | Track metrics such as debt-to-equity and interest coverage ratios to assess leverage sustainability. |

| Balancing Risks and Returns | Leverage increases both potential gains and losses, necessitating a balanced approach to avoid financial distress. |

| Avoiding Common Pitfalls | Assess stress scenarios realistically and diversify investments to mitigate risks associated with leverage. |

Defining Financial Leverage and Key Concepts

Financial leverage is the strategic use of borrowed money to amplify your investment returns. Instead of relying solely on your own capital, you borrow funds to increase the size of your investments, potentially magnifying profits. For mid-career professionals managing portfolios, understanding this concept separates those who simply invest from those who strategically grow wealth.

What Is Financial Leverage?

At its core, leverage means using debt to finance investments. When you borrow money at a lower interest rate than your investment generates, the spread between these rates amplifies your returns. Financial leverage arises from corporate financing decisions about how much borrowed capital funds your investments.

Consider this practical example: You have $100,000 to invest. Without leverage, you deploy that full amount. With 2:1 leverage, you borrow an additional $100,000, controlling $200,000 in assets. If your investment gains 10%, you earn $20,000 on your original $100,000—a 20% return on your actual capital.

The Core Components of Leverage

Three elements drive leverage decisions:

- Borrowed capital: The funds you acquire through loans, margin accounts, or other credit mechanisms

- Return on investment: The percentage gain your invested capital generates annually

- Cost of debt: The interest rate you pay on borrowed money

The mathematics work when your ROI exceeds your borrowing cost. A 12% annual return on borrowed funds costing 5% in interest creates a profitable 7% spread.

Key Leverage Ratios You Should Track

Professionals monitor specific metrics to assess leverage levels:

- Debt-to-equity ratio: Total debt divided by shareholder equity (higher ratios indicate greater leverage)

- Debt-to-assets ratio: Total debt divided by total assets (shows what percentage of assets are financed by borrowing)

- Interest coverage ratio: Operating income divided by interest expenses (measures ability to service debt)

These ratios reveal whether your leverage is sustainable or approaching dangerous territory.

The Risk-Return Tradeoff

Leverage cuts both ways. A 10% loss on a leveraged position hurts more than a 10% loss on unleveraged capital. Borrowed funds still require repayment regardless of market performance. When markets decline, margin calls force you to deposit additional capital or liquidate positions at unfavorable prices.

Leverage amplifies both gains and losses—the same borrowed dollar that doubles your profits during upswings can wipe out your equity during downturns.

Beyond investment returns, leverage affects your business operations, interest expenses, and overall financial obligations. Understanding your sector’s typical leverage levels helps you assess whether your strategy aligns with industry standards or if you’re taking excessive risk.

Pro tip: Calculate your personal leverage ratio monthly using total debt divided by total assets; track whether this ratio increases sustainably with your investment strategy or signals over-extension.

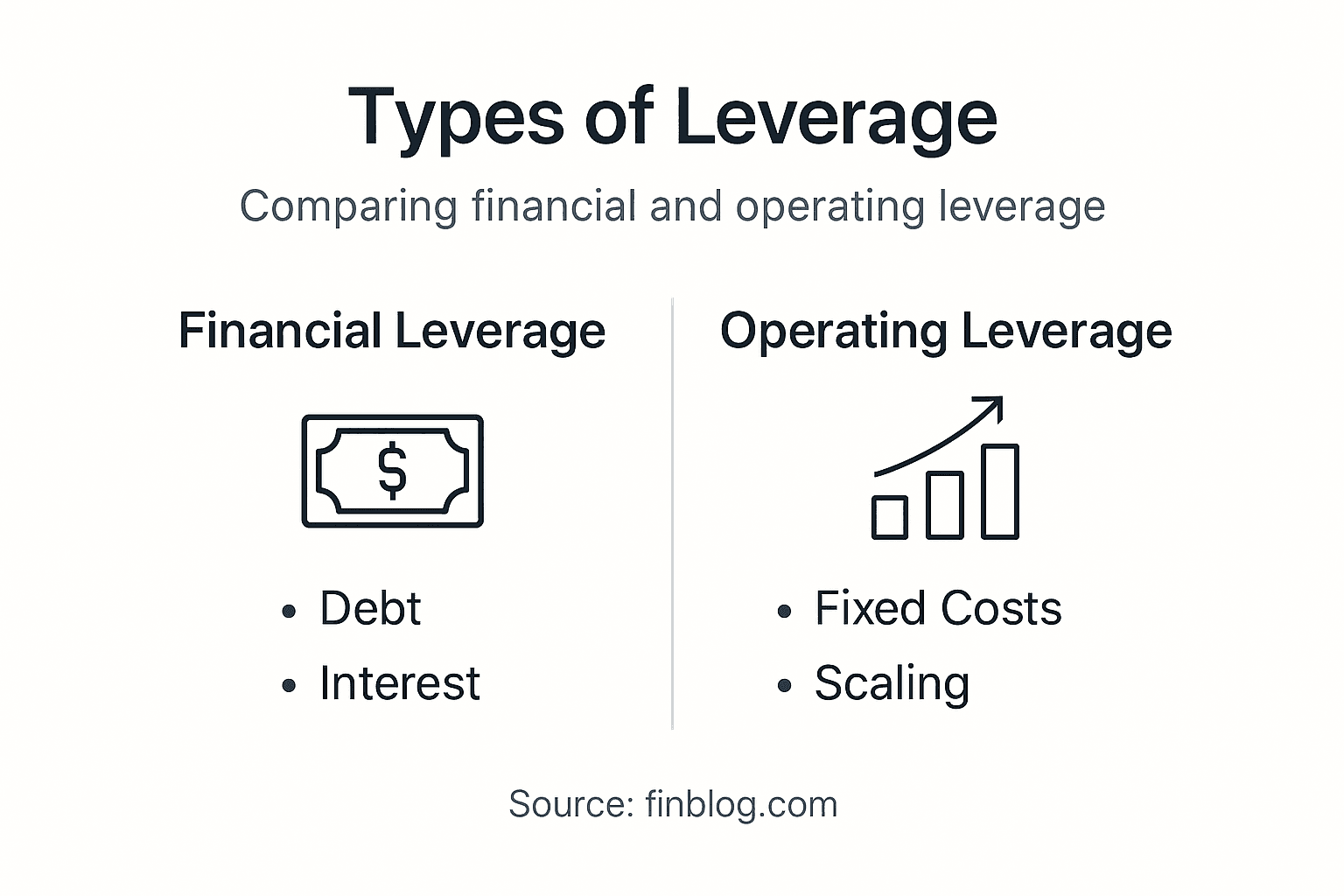

Main Types and Real Applications Explained

Leverage comes in different forms, and understanding each type helps you choose the right strategy for your portfolio. While the concept sounds complex, most professionals use one or more of these approaches regularly without always recognizing them as distinct leverage types.

Financial Leverage: The Direct Borrowing Approach

Financial leverage is the most straightforward type. You borrow money directly and invest it to amplify returns. This is what most investors think of when they hear “leverage”—taking a loan to buy real estate, using margin on your brokerage account, or financing equipment purchases.

Three main types of leverage exist in business: financial, operating, and combined. Financial leverage specifically involves borrowing funds to finance assets or operations, increasing your return on equity when investments perform well.

Example: A real estate developer borrows $5 million at 5% interest to purchase a property generating 8% annual returns. The 3% spread creates profit from leverage alone.

Operating Leverage: The Fixed Cost Strategy

Operating leverage amplifies profits through fixed costs in your business structure. Once you cover fixed expenses, each additional sale generates higher margins. This type applies less to individual investors but heavily impacts business-focused professionals.

Manufacturing operations exemplify this perfectly. A company with high equipment costs spreads those fixed expenses across more units as production increases, boosting profit margins significantly on incremental sales.

Combined Leverage: The Dual Effect

Combined leverage merges financial and operating leverage simultaneously. A company borrows money to purchase manufacturing equipment, creating both financial leverage (debt) and operating leverage (fixed costs). The combined impact amplifies profits but also magnifies losses during downturns.

Retail inventory financing demonstrates this in practice. A retailer borrows capital to stock inventory (financial leverage) while maintaining fixed store costs (operating leverage). Strong sales periods generate exceptional profits, but slow periods create painful losses.

Real-World Applications Across Sectors

Leverage appears throughout professional finance:

- Real estate development: Borrowing to purchase property and land

- Manufacturing: Financing equipment and machinery purchases

- Retail operations: Funding inventory expansion through credit

- Corporate acquisitions: Securing debt to acquire other companies

- Investment portfolios: Using margin accounts to buy securities

Each application requires different risk management approaches and monitoring frequencies.

Here’s a quick comparison of the three main types of leverage and how they impact business performance:

| Leverage Type | How It Works | Main Benefit | Common Example |

|---|---|---|---|

| Financial Leverage | Use debt to buy assets | Higher returns on equity | Real estate financing |

| Operating Leverage | Use fixed costs in operations | Increased profit per sale | Manufacturing plant machinery |

| Combined Leverage | Use both debt and fixed costs | Maximum profit amplification | Retailer with financed stock |

Understanding Capital Structure Decisions

Capital structure decisions combine debt and equity financing, with debt creating leverage that impacts your financial risk and tax benefits. The optimal mix depends on your industry, risk tolerance, and financial position.

Each type of leverage serves different purposes—choose the type matching your investment goals and risk capacity, not the type offering maximum returns.

Investors often focus only on financial leverage because it’s tangible and easy to track. Overlooking operating leverage leads to blind spots when analyzing your true leverage exposure across all your holdings.

Pro tip: Audit your portfolio for all three leverage types monthly—financial leverage from direct borrowing, operating leverage embedded in business holdings, and combined effects—to identify hidden leverage exposures.

How Financial Leverage Works in Practice

Leverage operates through a straightforward mechanism: you invest borrowed money alongside your own capital, amplifying both gains and losses. The mechanics remain consistent across real estate, stocks, and business acquisitions, though the execution varies by asset class.

The Basic Mechanics

Start with your equity—the money you actually own. Add borrowed funds at a fixed interest rate. Deploy the combined capital into an investment generating returns. If returns exceed borrowing costs, leverage creates profit. If returns fall below costs, leverage creates losses.

Consider this concrete scenario: You have $50,000. You borrow an additional $50,000 at 4% annual interest. You invest the full $100,000 in assets returning 8% annually. Your gross return is $8,000, but interest costs $2,000, leaving $6,000 net profit on your $50,000 equity—a 12% return instead of 8%.

The Two-Way Impact on Your Returns

Leverage magnifies your percentage gains when investments succeed. The same $50,000 equity controls twice the assets, so each percentage point of returns produces doubled profits. This upside attraction draws most professionals to leverage.

But leverage also magnifies losses. If your $100,000 investment drops 10%, you lose $10,000. On your $50,000 equity, that represents a 20% loss—twice the percentage decline in asset value.

Interest Obligations and Risk Vulnerability

Financial leverage combines equity and debt financing, where debt incurs fixed interest obligations increasing financial risk. Your lender demands payment regardless of investment performance. During economic downturns, this fixed obligation becomes crushing.

Companies with high leverage are more vulnerable to economic cycles. A manufacturing firm earning $100,000 annually can easily service $50,000 in debt. But if a recession cuts earnings to $40,000, that same debt burden becomes unbearable without asset sales or restructuring.

The Tax Benefit You Shouldn’t Ignore

Interest payments on debt are tax-deductible in most jurisdictions. This “interest tax shield” reduces your true cost of borrowing. If you borrow at 5% interest but deduct that interest at a 30% tax rate, your effective borrowing cost drops to 3.5%.

This tax advantage explains why corporations maintain leverage even when it increases risk. Tax efficiency improves leverage returns substantially.

Balancing Growth with Survival

The critical skill is balancing leverage to enhance earnings while managing risks. Too little leverage leaves potential returns unrealized. Too much leverage risks business survival during inevitable downturns.

Key considerations include:

- Your income stability: Stable income supports higher leverage; volatile income demands lower leverage

- Interest rate environment: Rising rates increase leverage costs; falling rates improve leverage returns

- Asset volatility: Stable assets support higher leverage; volatile assets demand conservative leverage

- Economic cycle stage: Early-cycle growth supports aggressive leverage; late-cycle peaks demand caution

Leverage amplifies returns during good times but demands unwavering discipline during downturns—the true cost reveals itself when markets decline.

Most professionals underestimate leverage risk because they calculate returns only in favorable scenarios. Stress-test your leverage by modeling returns if your investment drops 20%, 30%, or 40%. Can you survive?

Pro tip: Calculate your break-even interest rate monthly—divide your investment returns by your total borrowed capital to see the exact rate your assets must earn to justify leverage costs.

Risks, Costs, and Common Mistakes to Avoid

Leverage amplifies returns, but it also amplifies pain when investments underperform. The professionals who survive market cycles understand leverage’s dark side before deploying it aggressively. This section reveals the real costs and pitfalls most investors discover too late.

The Core Risk: Inability to Pay

Leverage increases financial risk, especially the risk of being unable to fulfill interest and principal payments. Your lender doesn’t care about market conditions. Interest payments and principal repayment demands arrive regardless of whether your investment gained or lost value.

This creates a critical vulnerability. A $50 million real estate deal financed with 80% leverage requires $4 million in annual debt service. If rental income drops 30% during a recession, you still owe $4 million. Many otherwise sound investments fail because leverage obligations become unsustainable.

Margin Calls: The Forced Liquidation Trap

Brokers lending money for stock purchases maintain minimum equity percentages. When your leveraged position declines, brokers issue margin calls demanding additional cash or forced asset sales. The timing couldn’t be worse—margin calls arrive during downturns when selling locks in losses.

Investors frequently panic during margin calls, selling quality assets to raise cash quickly. They recover later when prices rebound, but they’ve crystallized losses by selling at bottoms. Leverage forces you into emotional, reactive decisions.

Overestimating Your Risk Tolerance

Most professionals overestimate leverage capacity. You calculate returns assuming moderate market conditions. Reality includes 20% declines, 40% drawdowns, and multi-year bear markets. Your leverage level feels manageable until markets test it.

Common mistakes include:

- Ignoring stress scenarios: Modeling only 5% to 10% downside while ignoring 30% possibilities

- Assuming stable income: Overlooking job loss, contract non-renewal, or business disruption risks

- Underestimating duration: Planning for short-term leverage when market recoveries take years

- Concentrating leverage: Deploying leverage across correlated assets instead of diversifying

The Hidden Cost of Leverage

Beyond interest payments, leverage carries psychological costs. Managing leveraged positions creates stress and forces constant monitoring. You lose sleep during market volatility. Decision-making suffers from anxiety rather than rational analysis.

Additionally, excessive leverage can lead to financial distress and jeopardize survival. Companies and individuals pursue overly aggressive leverage to maximize short-term returns, then face bankruptcy when markets normalize. The two-year bull market that justified 5:1 leverage turns into a nightmare when markets correct.

The Timing Mistake: Using Leverage at Peaks

Retail investors typically increase leverage after strong returns, exactly when valuations peak. Professional traders do the opposite—they reduce leverage after extended rallies and increase it after crashes. Most professionals execute this backwards.

You feel confident deploying leverage after years of gains, but that’s precisely when leverage is most dangerous. Conversely, deploying leverage after 40% declines feels terrifying, but that’s when leverage offers the best risk-reward.

Excessive leverage creates fragility—the system survives normal conditions but shatters under stress that always eventually arrives.

Diversification becomes critical with leverage. Minimizing investment risk across uncorrelated assets reduces the chance that all your leveraged positions decline simultaneously.

Review this summary of common mistakes and how to avoid them when using leverage:

| Mistake | Potential Impact | How to Avoid |

|---|---|---|

| Ignoring market downturns | Forced asset sales, heavy losses | Stress test worst-case scenarios |

| Overestimating risk tolerance | Unsustainable debt repayments | Set conservative leverage limits |

| Poor timing with leverage | Losses at market peaks | Reduce leverage after bull runs |

| Lack of diversification | Simultaneous asset declines | Spread investments across sectors |

Pro tip: Set maximum leverage ratios based on your worst-case scenario, not your expected scenario—if you can’t survive a 40% portfolio decline, reduce leverage until you can.

Take Control of Your Financial Leverage Strategy Today

Understanding financial leverage is crucial for any professional looking to boost investment returns while managing risks effectively. This article highlights the delicate balance between amplifying profits and exposing yourself to amplified losses and financial obligations. If you want to avoid common pitfalls like margin calls, overestimating your risk tolerance, or poor timing you need expert guidance tailored to your unique financial situation.

At finblog.com we offer personalized financial consulting and educational resources designed specifically for serious investors and mid-career professionals. Our approach helps you master key concepts such as debt-to-equity ratios, interest coverage, and the cost of borrowing so you can confidently apply leverage without jeopardizing your financial health. Visit finblog.com now to access expert insights and take the first step toward smarter leverage decisions. Don’t wait to secure your financial future with strategies built to withstand market ups and downs.

Frequently Asked Questions

What is financial leverage?

Financial leverage refers to the use of borrowed money to increase the potential return on investment. It allows investors to control larger assets than they could with just their own capital.

How does financial leverage amplify returns?

Financial leverage amplifies returns by allowing investors to borrow funds at a lower interest rate than the returns generated by the investment. The profit gained from the investments exceeds the cost of borrowing, leading to greater overall returns.

What are the main types of leverage?

The three main types of leverage are financial leverage (using debt to finance investments), operating leverage (utilizing fixed costs to increase profit margins), and combined leverage (integrating both financial and operating leverage strategies).

What risks are associated with using financial leverage?

The primary risks include the inability to meet debt obligations, potential margin calls leading to forced sales of assets, overestimating one’s risk tolerance, and the psychological burden of managing leveraged investments.

Recommended

- Understanding Borrowing Basics for Financial Success – Finblog

- AI Boom and Private Credit Surge Push Corporate Bond Markets to New Records

- Credit Utilization Explained: Impacts, Types, and Strategy – Finblog

- Financial Risk Management Explained: Strategies and Practices – Finblog

- Machine Learning in Finance – Maximizing Trading Efficiency