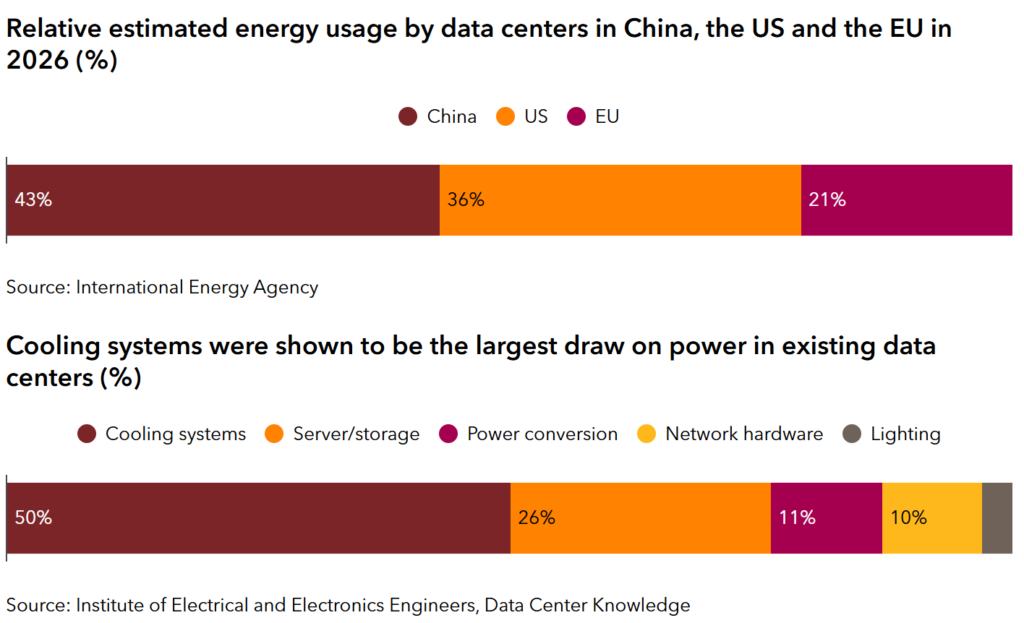

As AI hype roars across global markets, Europe’s version of the trade is not about “next-gen software” but the back-end infrastructure: data centres, power grids, and energy logistics. These are the real battlegrounds where AI’s scale and sustainability will be determined.

The Rally Behind the Scenes

A basket tracking 10 European data center and infrastructure names has soared 23% year-to-date, outperforming the Stoxx Europe 600’s 12% gain and even the Nasdaq 100.

That rally reflects investor bets that AI workloads will force compute-intensive operations to migrate closer to users — and that power delivery will become a constraint.

The AI boom in Europe is less about flashy models and more about who can supply the real estate, cooling, connectivity, and megawatts.

Power Infrastructure Is the Hidden Constraint

According to PERE, the data center boom is colliding with outdated grid infrastructure and permitting delays — especially in parts of Europe where expanding transmission lines requires years of regulatory work.

Engineers warn of a “power conundrum”: data centers demand constant, high-quality electricity, but many national grids are only lightly upgraded, with limited headroom for big new loads.

Some utility operators have begun balking at new data center load requests during peak hours, fearing disruptions to residential supply or grid instability.

Why Europe’s AI Trade Looks Different From the US

In the U.S., the AI stock boom is dominated by chipmakers (Nvidia, AMD) and cloud platforms. European exposure is thinner, so the premium is going to infrastructure plays.

European real estate and utility firms have large footprints and existing networks — making them poised to capture the AI “digital backbone” value.

But returns may take time; unlike startups, these are capital-intensive, regulated businesses with long ROI curves — and they are vulnerable to policy risk, grid constraints, and energy price volatility.

Risks on the Road

- Regulatory drag: Grid expansion needs permits, environmental review, and cross-border coordination. Delays can stall projects long before they begin.

- Energy costs: Rising electricity prices or carbon charges could erode margins for data centers and colocation providers.

- Stranded assets: If AI demand shifts fast or becomes more efficient, excess capacity in power or cooling could turn into underutilized investments.

- Competition from the U.S. and Asia: Regions with more flexible power markets or aggressive incentives may outpace Europe’s infrastructure rollouts.

Europe’s AI narrative is being written not in algorithms, but in megawatts, fiber, and real estate development. While many eyes are on models and applications, the true alpha may lie in who controls the power and plumbing behind AI. If the infrastructure builds fast enough, Europe may punch above its weight in the AI era — but grid bottlenecks, regulation, and capital risk could cap the upside.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related:

OpenAI Surges to $500 Billion Valuation, Overtakes Musk’s SpaceX

Trump’s $100,000 H-1B Visa Fee: What It Means for Tech, Talent, and Markets

Fed Divide Widens as Policymakers Clash Over Pace of Rate Cut