What sets digital banking in 2025 apart is how it turns banking into a fully interconnected, tech-driven environment. With the rise of fintech startups and non-bank actors, traditional banks now share the stage, creating a fundamental transformation across payments, investments, and daily financial decisions. For financial professionals and investors, navigating this rapid evolution means staying alert to new business models, regulatory shifts, and innovative services that can reshape wealth strategies from New York to Singapore.

Table of Contents

- What Defines Digital Banking in 2025

- Emerging Technologies Driving Banking Innovation

- Types of Digital Banking Models and Services

- Regulatory Changes and Data Privacy Impacts

- Risks, Costs, and Competitive Challenges Ahead

Key Takeaways

| Point | Details |

|---|---|

| Technology Convergence | Digital banking in 2025 hinges on the integration of various technologies like AI and blockchain, reshaping the financial service landscape. |

| Enhanced Customer Engagement | Financial institutions now focus on personalized customer interactions through various digital platforms, enhancing overall service experience. |

| Emerging Risks | As digital banking evolves, it faces increased risks related to cybersecurity, operational failures, and regulatory compliance, necessitating vigilance from users. |

| Regulatory Changes | Stricter regulations in data privacy and AI governance will impact how banks operate, affecting costs and customer service. |

What Defines Digital Banking in 2025

Digital banking in 2025 is no longer just about online accounts or mobile check deposits. It represents a fundamental shift in how financial institutions operate, compete, and serve customers globally.

The core driver is technology convergence—smartphones, tablets, artificial intelligence, and blockchain are merging into integrated financial ecosystems. Banks no longer control the entire customer experience alone. Fintech startups, payment processors, and non-bank actors shape the landscape alongside traditional institutions.

The Five Pillars of Modern Digital Banking

Understanding digital banking today requires looking at how institutions function across multiple dimensions:

- Customer engagement: Direct, personalized interactions across mobile, web, and voice channels

- Operating models: Automation and AI handling routine processes while humans focus on complex decisions

- Data utilization: Real-time analytics driving risk assessment, fraud detection, and financial recommendations

- Platform architecture: Open APIs enabling third-party integrations and ecosystem partnerships

- Revenue innovation: New income streams from digital payments, embedded finance, and alternative investments

Emerging IT across financial services has created what researchers call “holistic transformation”—affecting customer experience, company operations, banking institutions, regulatory bodies, and society itself.

What makes 2025 different from previous years? The speed of adoption. You’re no longer watching digital banking emerge. You’re living within it.

How Digital Banking Reshapes Wealth Strategy

For individual investors and financial professionals, this matters directly. Digital banking transformation creates both opportunities and competitive pressures.

You now have access to investment platforms previously unavailable to retail investors. Portfolio management tools that cost $10,000 annually five years ago are now bundled into free accounts. Fractional shares, algorithmic rebalancing, and tax-loss harvesting are standard features, not premium add-ons.

But this abundance creates a different challenge: data overload. More information doesn’t guarantee better decisions without a clear strategy.

What This Means for Your Decisions

Digital banking isn’t just about convenience. It’s about how financial institutions now collect, process, and act on your financial data in real time.

- Real-time transaction data enables instant fraud detection and spending insights

- AI algorithms personalize investment recommendations based on your behavior

- Open banking standards let you aggregate accounts across multiple institutions

- Regulatory oversight, particularly regarding how banking rules evolved in 2025, shapes what platforms can and cannot do with your information

Think of it this way: A bank in 2015 knew what you deposited and withdrew. A digital bank in 2025 knows why you spent money, when you’re likely to need it, and what financial products align with your actual behavior patterns.

Digital banking transforms financial institutions from transaction processors into data-driven wealth partners. This shift requires you to be intentional about what information you share and how institutions use it.

Pro tip: Audit which financial platforms access your data and what permissions you’ve granted. Most investors forget about permissions granted years ago, letting dormant apps track activity they no longer use.

Emerging Technologies Driving Banking Innovation

Four technologies dominate banking transformation in 2025. Each one reshapes how institutions operate and how you manage money.

Artificial Intelligence Leads the Way

Artificial intelligence powers nearly every banking function today. Machine learning algorithms detect fraud faster than humans ever could, sometimes catching suspicious activity within milliseconds of a transaction.

AI also personalizes your financial experience. Banks now use AI to analyze spending patterns, predict cash flow needs, and recommend investment adjustments tailored to your specific situation. What took a financial advisor hours now happens automatically.

However, AI risks are growing alongside the technology. Financial institutions are increasingly exposed to concentrated technology risk as they rely heavily on AI systems.

Blockchain and Distributed Systems

Blockchain technology enables faster, cheaper cross-border payments and settlement. Traditional international transfers took 3-5 business days and cost 5-10% in fees. Blockchain-based systems complete in hours for a fraction of the cost.

Beyond payments, blockchain creates transparent audit trails for regulatory compliance. Banks can prove transaction legitimacy without intermediaries.

- Faster international money movement

- Lower transaction costs

- Transparent record-keeping

- Reduced settlement risk

Mobile-First Banking Platforms

Mobile applications are no longer secondary to desktop banking. They’re now the primary interface for most users. Advanced mobile platforms offer portfolio management, loan applications, and investment trades from your phone.

The shift matters for wealth strategies. You can respond to market movements instantly without being tethered to a computer.

Open Banking and API Integration

Open Banking APIs connect your accounts across institutions. Instead of logging into five different banks, you aggregate everything in one dashboard. Third-party apps access your transaction data with your permission, enabling better financial insights.

This creates new opportunities but also new security considerations. You control what data flows where, but you must actively manage these permissions.

Emerging technologies in banking reduce friction, lower costs, and increase transparency. They also create new security vulnerabilities and concentration risks that require your attention.

Pro tip: Review which fintech apps have access to your bank accounts and remove permissions you no longer use. Most investors grant access once and never revoke it, creating unnecessary security exposure.

Types of Digital Banking Models and Services

Digital banking isn’t one-size-fits-all. Different models serve different customer needs, and understanding which type matches your financial situation matters for your wealth strategy.

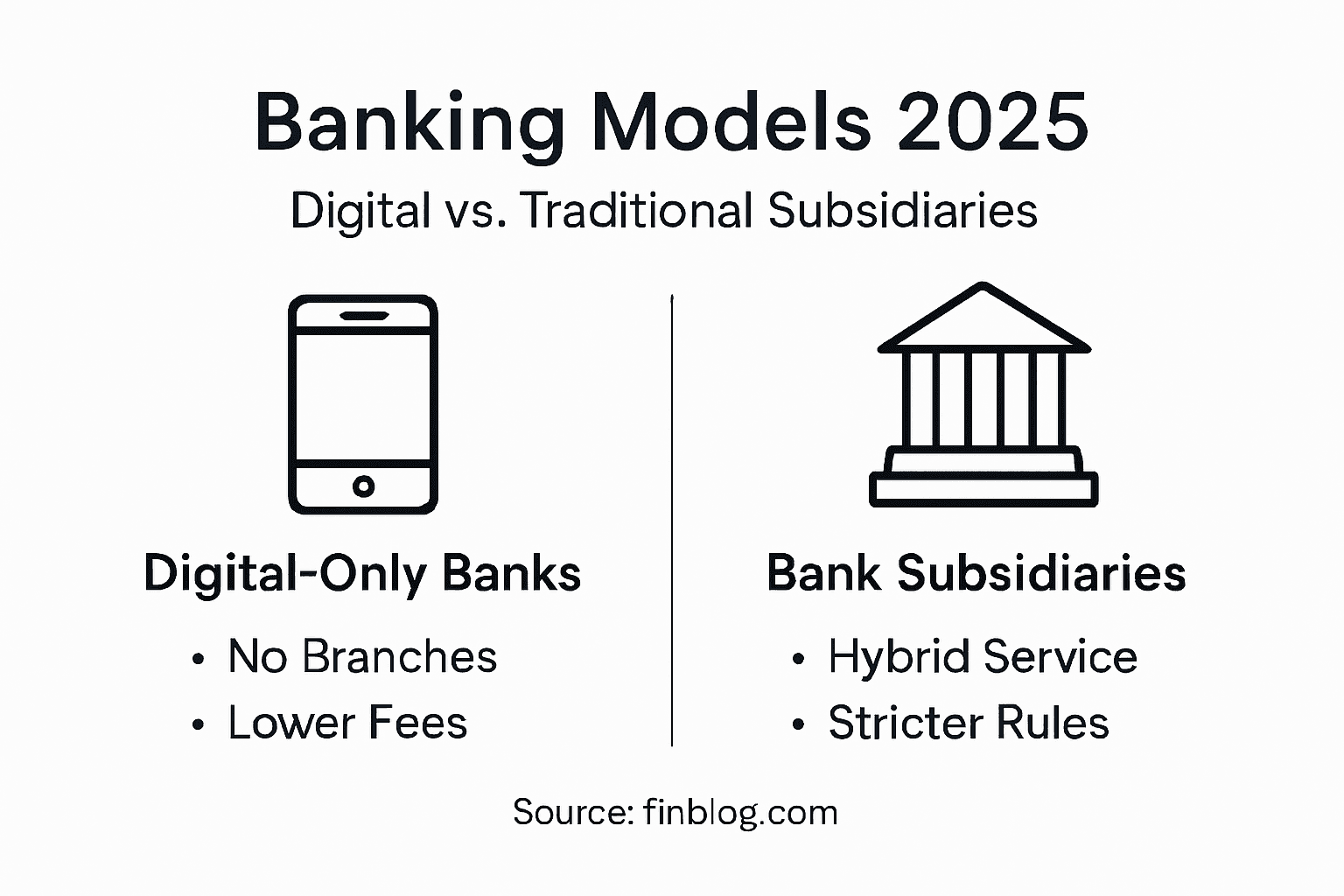

Digital-Only Banks vs. Traditional Bank Subsidiaries

The banking ecosystem splits into two main structures. Digital-only banks (also called neobanks) operate exclusively online with no physical branches. They keep costs low and pass savings to customers through higher interest rates on deposits and lower fees on loans.

Digital subsidiaries are when traditional banks create online-only divisions. These combine the security and regulatory backing of an established institution with the agility of digital operations.

Both models rely heavily on retail deposits to fund lending and investment activities. Digital banking business models increasingly focus on either lending conversion (turning deposits into loans) or money market fund strategies (investing deposits in liquid assets).

Here is a comparison of digital-only banks and traditional bank subsidiaries in the modern banking ecosystem:

| Aspect | Digital-Only Banks (Neobanks) | Traditional Bank Subsidiaries |

|---|---|---|

| Physical Branches | None; fully online | Backed by physical branches |

| Cost Structure | Lower operational expenses | Benefit from legacy systems |

| Regulatory Support | Limited regulatory history | Strong compliance frameworks |

| Interest Rates | Often higher for deposits | Competitive but less flexible |

| Risk Profile | Agile but higher closure risk | Stable with broader safeguards |

Core Service Delivery Platforms

Digital banking services reach you through multiple channels, each with distinct advantages:

- Internet banking: Full account access and investment management from a web browser

- Mobile banking apps: Everything your account offers, optimized for your phone

- Challenger banks: Hyper-personalized services using AI and machine learning

- ATM networks: Traditional cash access integrated into digital ecosystems

- Telephony services: Account support and transactions through phone systems

The delivery method you choose affects your ability to manage money on your schedule. Mobile apps dominate for speed; web platforms work better for complex portfolio decisions.

Lending-Focused vs. Investment-Focused Models

Understand the business model behind your bank—it shapes your experience and risk exposure.

Lending-focused models convert your deposits into mortgages, auto loans, and personal credit lines. Your money funds other customers’ borrowing. These models generate revenue from interest spreads and rely on loan quality for stability.

Investment-focused models place deposits into money market funds and liquid securities instead. Your money earns returns from financial markets rather than loan interest. These models require higher liquidity buffers and expose you to market volatility.

Neither approach is inherently superior. Lending models offer stability; investment models offer flexibility.

Different digital banking models create different risk profiles. A lending-focused bank’s stability depends on loan quality; an investment-focused model depends on market conditions and liquidity.

What This Means for Cross-Border Banking

Digital banks operate globally without physical limitations. You can open accounts in multiple countries from your home. This creates opportunities but also complexity around currency, taxation, and regulatory oversight.

Many types of savings accounts now operate across borders, but deposit insurance and liability protections vary by jurisdiction.

Pro tip: Before opening an account with a digital-only bank, verify deposit insurance coverage in your country. Not all digital banks offer the same protection as traditional institutions, and some limits may be lower than you expect.

Regulatory Changes and Data Privacy Impacts

Regulation in digital banking is tightening. Governments worldwide are implementing stricter rules around artificial intelligence, data protection, and cross-border payments. These changes reshape how banks operate and directly affect your financial security.

The Regulatory Shift in 2025

Global regulators are moving away from a “wait and see” approach. Digital finance policies now prioritize artificial intelligence governance, central bank digital currency deployment, and simplified cross-border payment frameworks.

Three regulatory priorities dominate the landscape:

- Artificial intelligence oversight: Banks must explain how AI makes lending and investment decisions

- Data privacy enforcement: Stricter rules on what financial institutions collect and share about you

- Cross-border payments: New frameworks using distributed ledger technology to speed international transfers

For investors, this means more transparency but also more complexity in compliance costs that banks eventually pass to customers.

Data Privacy as Your Personal Shield

Data privacy regulations are your first line of defense against unauthorized access to financial information. Banks now face substantial penalties for breaches, incentivizing stronger security investments.

Regulations require institutions to:

- Notify you immediately if your data is compromised

- Obtain explicit consent before sharing information with third parties

- Allow you to access, correct, and delete your personal data

- Implement encryption and security protocols meeting government standards

However, more regulation also means more forms to fill out and more permissions to manage.

How Compliance Costs Affect Your Fees

Regulatory compliance is expensive. Banks spend billions annually on compliance infrastructure, audits, and personnel. These costs appear in your account fees, interest rates, and service charges.

Smaller digital banks sometimes struggle more with compliance costs than established institutions. This creates a tradeoff: you might get better rates from a struggling neobank, but you accept higher risk if regulatory pressure forces closure.

Artificial Intelligence Governance Requirements

Banks using AI for lending decisions, investment recommendations, or fraud detection must now disclose how these systems work. AI governance rules require institutions to:

- Document algorithmic decision-making processes

- Test for bias in automated decisions

- Allow appeals when AI denies credit or services

- Maintain human oversight of critical decisions

This transparency protects you from discriminatory lending but also slows down loan approvals and investment recommendations.

Regulatory changes in 2025 balance innovation with protection. Stronger rules increase security but also increase costs and complexity. Understanding what regulations apply to your bank helps you evaluate the tradeoffs.

Central Bank Digital Currencies (CBDCs)

Governments are launching digital versions of their national currencies. The United States, European Union, and Asian countries are all testing CBDCs. These government-backed digital currencies could eventually replace some traditional banking functions.

For wealth strategies, CBDCs create new considerations around currency diversification and deposit safety across different currency zones.

Pro tip: Monitor your bank’s regulatory status by checking government financial authority websites quarterly. Banks facing regulatory enforcement actions may be riskier places to hold your money, and early warning signs often appear in official filings.

Risks, Costs, and Competitive Challenges Ahead

Digital banking’s rapid expansion creates opportunities, but it also introduces real dangers. Understanding these risks helps you protect your wealth and make smarter banking decisions.

Fraud and Cybersecurity Threats

Digital banks operate entirely online, making them attractive targets for cybercriminals. Fraud vulnerability increases when institutions prioritize speed over security checks.

Common threats include:

- Account takeover through stolen credentials

- Phishing attacks targeting login information

- Synthetic identity fraud using fabricated personal data

- API exploits accessing third-party integrations

- Insider threats from employees with system access

Increased fraud vulnerability stems from dependence on interconnected systems and third-party infrastructure. A breach at one service provider can expose customer data across multiple banks.

Operational Complexity and System Failures

Digital banks depend on technology that occasionally fails. Server outages, software bugs, and network disruptions can lock you out of your accounts during critical moments.

When systems fail during market volatility, you cannot execute trades or access funds. This operational risk creates real financial losses, especially for active investors managing time-sensitive positions.

Credit Risk in Underserved Markets

Digital banks often target underserved borrowers—people traditional banks rejected. These borrowers carry higher default risk. When a digital bank focuses heavily on lending to risky borrowers, deposit holders absorb losses if loan defaults spike.

Understanding your bank’s lending focus matters. Ask whether your bank emphasizes prime borrowers or riskier markets.

Competitive Pressure and Rising Costs

Strategic competition from fintech and neobanks forces traditional banks to spend heavily on technology modernization. Banks face increased costs for compliance, technology investments, and meeting evolving customer expectations.

These costs eventually reach you through:

- Higher account maintenance fees

- Lower interest rates on deposits

- Reduced withdrawal limits

- Minimum balance requirements

Smaller digital banks struggle most with cost pressures. A bank offering exceptional rates today might struggle financially tomorrow, creating deposit safety concerns.

Regulatory Risk and Compliance Failures

Compliance failures lead to substantial financial penalties, which banks pass to customers. Regulatory enforcement actions also damage institutional trust, sometimes triggering customer withdrawals that force closures.

Banks operating in multiple countries face compounded regulatory complexity. A violation in one jurisdiction can trigger investigations elsewhere, escalating costs and operational disruptions.

AI Dependence and Algorithmic Risk

Digital banking relies on AI systems making critical decisions about lending, fraud detection, and investment recommendations. When these systems fail, fail biased, or get hacked, the consequences affect thousands of customers simultaneously.

You have limited recourse when an algorithm denies your loan or flags your legitimate transactions as fraud. Appeals processes are often opaque and slow.

Digital banking’s risks are real and growing. Fraud, system failures, and competitive pressures create dangers that traditional banking mitigates through physical infrastructure and established risk management.

Geopolitical and Cross-Border Risks

Geopolitical risks affect digital banks operating globally. Trade tensions, sanctions, or currency controls can freeze international accounts or disrupt payment systems without warning.

Digital banks with deposits across multiple countries face currency and jurisdiction risks you must consider when choosing where to hold funds.

Pro tip: Diversify your digital banking across multiple institutions rather than concentrating deposits at one bank. If one bank experiences a breach, system failure, or regulatory closure, your funds in other institutions remain accessible.

The following table highlights the primary risks and mitigation strategies in digital banking for 2025:

| Risk Area | Typical Threats | Mitigation Strategy |

|---|---|---|

| Cybersecurity | Account takeover, phishing, API exploits | Use MFA, monitor app permissions |

| Operational | Server outages, transaction delays | Diversify accounts, maintain backups |

| Regulatory | Compliance failures, changing laws | Monitor regulatory filings, choose trusted institutions |

| Credit | Lending to higher-risk borrowers | Evaluate bank’s loan portfolio focus |

Navigate Digital Banking Risks and Opportunities with Expert Guidance

As digital banking reshapes wealth strategies in 2025, managing challenges like data overload, AI risks, and regulatory complexity is essential for protecting your financial future. The article highlights important pain points such as fraud vulnerability, regulatory compliance costs, and the need to audit app permissions. Understanding these trends empowers you to make informed decisions amid fast-paced technological change.

At finblog.com, we specialize in helping serious investors and professionals decode these complex digital banking transformations. Discover actionable insights on managing digital finance policies, controlling data privacy risks, and optimizing your banking relationships for both security and growth. Act now to stay ahead of rapidly evolving risks by visiting finblog.com and exploring our expert resources tailored to your wealth strategy. Take control of your financial future today.

Frequently Asked Questions

What is digital banking and how has it evolved by 2025?

Digital banking has evolved to represent a comprehensive integration of technology, including AI and blockchain, reshaping how financial institutions operate and serve customers. By 2025, it encompasses personalized customer engagement and automated operations that rely on real-time data analysis.

How do emerging technologies like AI and blockchain impact digital banking in 2025?

Emerging technologies such as AI lead to faster fraud detection and personalized services, while blockchain enables cost-effective and swift cross-border payments with transparent record-keeping, significantly enhancing the banking experience.

What are the key differences between digital-only banks and traditional bank subsidiaries?

Digital-only banks operate exclusively online with lower operational costs, often providing better interest rates and lower fees. In contrast, traditional bank subsidiaries combine the security of well-established institutions with the efficiencies of digital banking, offering a broader range of resources and compliance support.

What should I consider regarding data privacy and regulatory changes in digital banking?

As regulations tighten, banks must adhere to strict data privacy rules that protect your information. You should actively manage permissions for financial apps and stay informed about your bank’s regulatory compliance status to ensure your data remains secure.

Recommended

- Understanding Personal Finance Trends 2025 for Better Decisions – Finblog

- US Banking Rules Shifted in 2025. Here’s What Banks Are Bracing for in 2026

- How to Pick Investments: Build Your Wealth Wisely in 2025 – Finblog

- Wealth Protection Strategies for Secure Financial Future – Finblog

- Finance Recruitment Trends in Birmingham (2026) | IBACO Recruitment