The bond market is being pulled in two directions at once. Higher oil prices and war-related inflation are pushing yields up, while slowing economic momentum is raising fears that growth may weaken more sharply in the months ahead.

Inflation fears take control

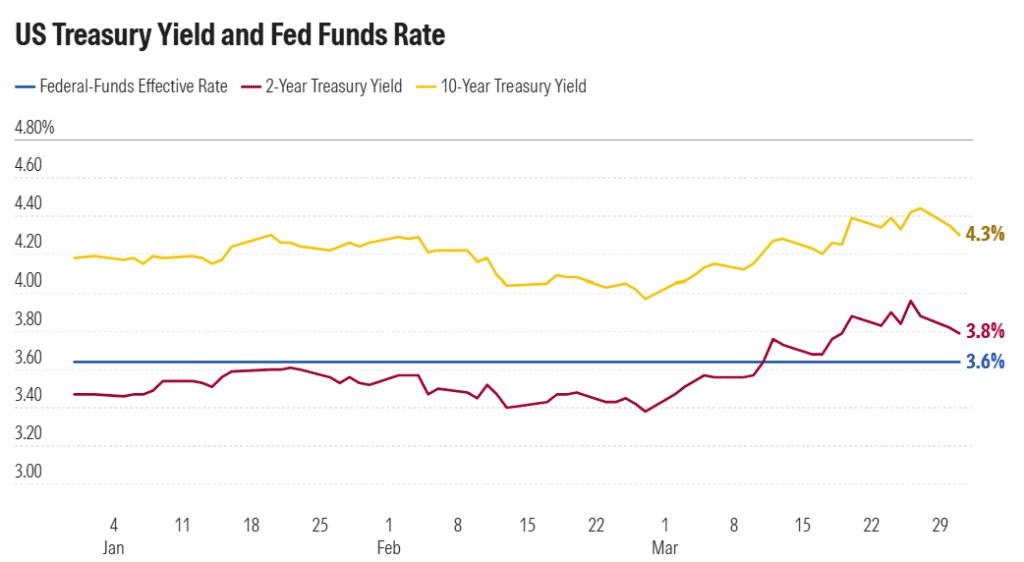

The first quarter was dominated by one clear theme: inflation is back in focus. The Iran conflict and the jump in oil prices forced investors to rethink earlier hopes for rate cuts, and bond yields moved higher across the market.

That shift was especially visible in Treasurys. The 10-year US Treasury yield ended the quarter around 4.3%, up from 4.2% at the start of the year, as markets began to price in the possibility that central banks may have to keep rates higher for longer

For bond markets, that matters immediately. When yields rise, prices fall. And that is exactly what happened.

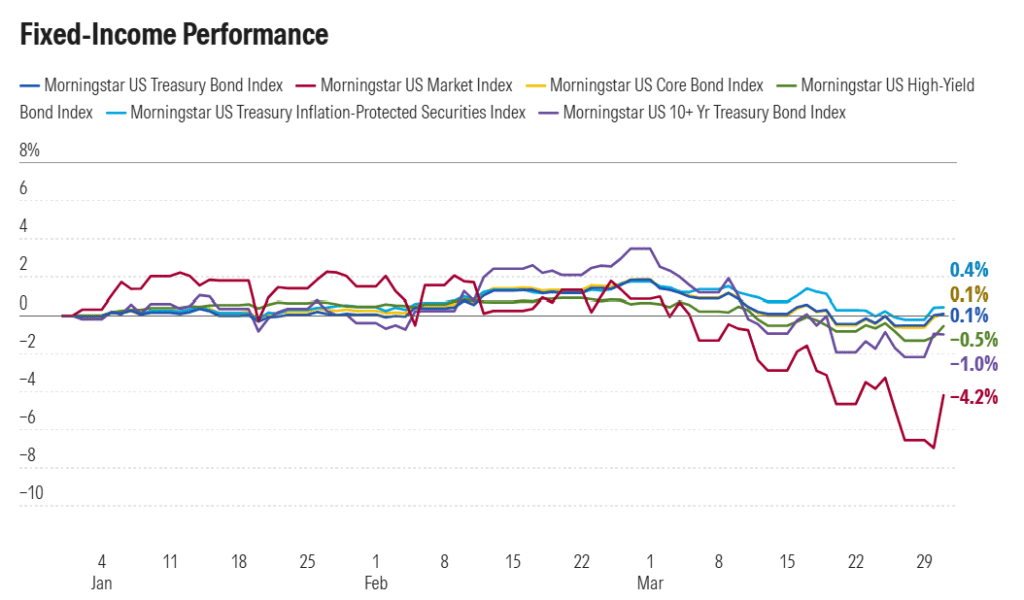

Most bond categories lost money

The pressure was broad, not isolated. Nearly every major US bond category ended the first quarter in negative territory, showing how difficult this environment has become for fixed-income investors.

The weakest areas included:

- Long-term core bonds

- High-yield bonds

- Corporate bonds

- Inflation-protected Treasurys

Even TIPS struggled, which is notable because they are designed to help in inflationary periods. But this time, rising rates were strong enough to outweigh the benefit of inflation adjustments

Growth worries are building underneath

Still, this is not just an inflation story. Beneath the rise in yields, there is a second concern growing more serious: the economy may be losing strength.

Higher energy prices are starting to act like a tax on households and businesses. Consumers face more expensive fuel and transportation costs, while companies must deal with uncertainty, supply disruptions, and weaker visibility on demand. If the conflict drags on, analysts warn it could start weighing much more heavily on growth.

That is why the bond market now looks so divided. Inflation points one way. Growth points the other.

The Fed is caught in the middle

This tension creates a difficult challenge for the Federal Reserve. If inflation keeps rising, policymakers may need to stay restrictive for longer or even consider tighter policy. But if growth weakens too much, the case for cuts returns.

For now, the Fed appears to be leaning toward patience. Rather than reacting aggressively to the latest oil shock, officials are signaling a more cautious, wait-and-see approach. That has left markets trying to guess whether inflation will prove temporary or whether it will become more persistent.

The result is a market that keeps changing its mind.

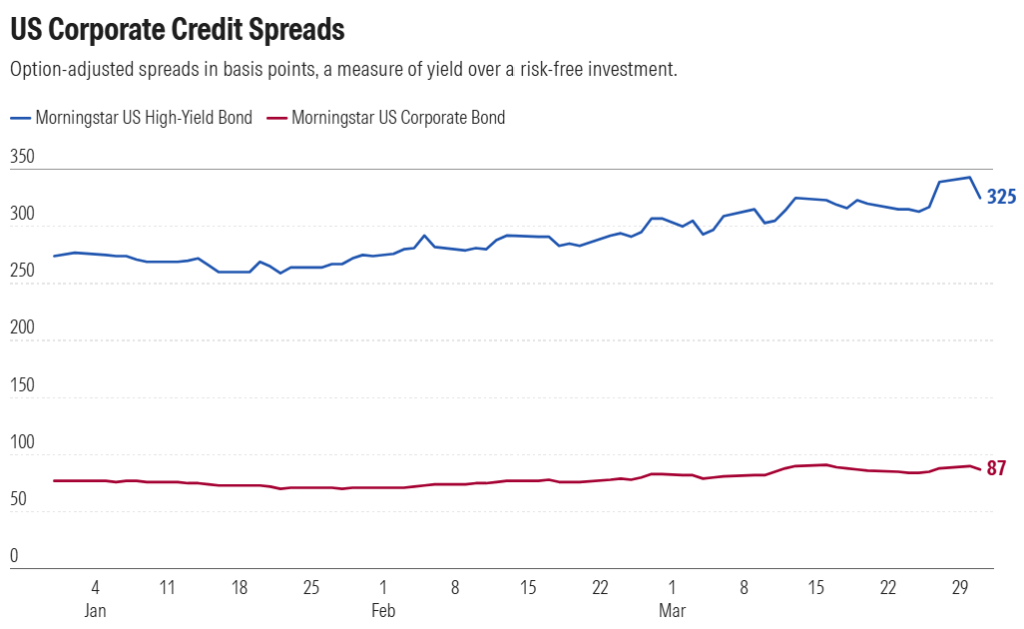

Credit markets are calmer than rates markets

One of the more interesting details is that credit markets have remained relatively stable, even while Treasury yields have moved sharply.

That means investors are showing more concern about inflation and interest rates than about corporate defaults. Credit spreads have widened only modestly so far, suggesting the market is not yet pricing in a severe recession or major stress in company balance sheets

In other words, investors are nervous, but they are not fully defensive.

Why bonds are no longer offering easy protection

Normally, bonds help protect portfolios when uncertainty rises. But this year, that relationship has been harder to rely on. Stocks have been volatile, and bonds have also struggled, especially when inflation expectations rise.

That is what makes the current setup so uncomfortable. Investors are facing a market where traditional safe havens are not performing as smoothly as usual.

What happens next

The next move in bonds will depend on which force becomes stronger. If inflation remains the bigger problem, yields could rise further and keep bond prices under pressure. But if growth slows more sharply, that could pull yields lower and bring bonds back into favor.

Right now, the market is stuck between those two outcomes. That is the real story in bonds today: not clarity, but conflict.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related: S&P 500 May Bottom Near 6,000 as Correction Plays Out