Planning for retirement brings a mix of anticipation and uncertainty, especially when rumors about Social Security’s future cloud important decisions. For many American professionals, understanding the real scope of Social Security matters because it is more than just a monthly payment in your later years. With more than 70 million Americans receiving benefits each month for retirement, disability, and family security, this system offers crucial support—ensuring your family’s financial well-being when life takes unexpected turns.

Table of Contents

- What Social Security Is And Common Myths

- Types Of Social Security Benefits In 2026

- How Eligibility And Benefit Amounts Are Determined

- New Rules, Taxes, And Cost-Of-Living Changes For 2026

- Risks, Shortfalls, And Planning Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Social Security Covers Multiple Situations | Social Security is not just for retirement; it also provides disability insurance and survivor benefits. This comprehensive safety net protects individuals and families in various life situations. |

| Myth-Busting Social Security | Common myths like Social Security going broke or contributions disappearing upon death are false. The program has a surplus until 2034 and offers survivor benefits for families. |

| Understanding Benefit Types Is Crucial | Social Security includes retirement benefits, SSDI, survivors benefits, and SSI, each serving different needs. Knowing which types apply to you can shape your retirement strategy. |

| Claiming Strategy Can Significantly Impact Benefits | Delaying benefits until full retirement age or age 70 can increase monthly payouts substantially. Many workers make costly mistakes by opting for early claims without considering long-term implications. |

What Social Security Is and Common Myths

Social Security isn’t just a retirement program—it’s a safety net that covers multiple life situations. Over 70 million Americans receive benefits every month for retirement, disability, survivor benefits, or a combination of these.

The program operates on a pay-as-you-go system. Your payroll taxes (FICA and SECA) fund current retirees’ benefits, while future workers will fund yours. This interlocking system has worked for nearly 90 years.

What Social Security Actually Does

Most people think of Social Security as just retirement income. That’s incomplete. The program provides three essential protections:

- Retirement benefits for workers age 62 and older

- Disability insurance if you become unable to work

- Life insurance protecting your family if you die (survivor benefits for spouses and children)

This breadth matters. Life insurance and disability protection through Social Security means you’re getting more than a pension—you’re getting comprehensive protection for your household.

The Biggest Myths Holding You Back

Myth 1: Social Security is going broke.

Not true. The program maintains a surplus lasting until 2034 under current financing. Even if the trust fund depletes, incoming payroll taxes will continue funding roughly 80% of scheduled benefits. That’s a significant reduction, not a total collapse.

Myth 2: Your contributions disappear if you die young.

Wrong. Your family receives survivor benefits. A spouse and minor children can collect based on your earnings record, even if you pass away before retirement.

Myth 3: Social Security isn’t “real” money because it’s not yours.

You earned these benefits. Your payroll taxes funded the program specifically to provide you income later. You’ve already paid into the system.

Myth 4: Everyone gets the same benefit.

Benefits are progressive, meaning lower earners receive a higher percentage of their previous income replaced. A person earning $30,000 yearly gets a larger replacement rate than someone earning $120,000. This protects lower-income workers from poverty.

Social Security replaced 67 million workers’ earnings and protected families from poverty in 2024 alone—it’s doing its job right now, not someday.

Pro tip: Pull your free Social Security statement at ssa.gov to see your actual projected benefits based on your real earnings history—not myths or guesses.

Types of Social Security Benefits in 2026

Social Security offers four distinct benefit types, each serving different life situations. As a mid-career professional, understanding which ones apply to you—and your family—shapes your entire retirement strategy.

Retirement Benefits

Retirement benefits are what most people picture when they think Social Security. You can claim starting at age 62, but your monthly payment increases significantly if you wait until your full retirement age (typically 66-67) or even age 70.

In 2026, the average monthly retirement benefit is projected to rise to $2,071, a modest increase from 2025. That jump reflects the annual 2.8% cost-of-living adjustment beneficiaries receive.

The longer you wait, the higher your benefit. Someone born in 1960 waiting from 62 to 70 increases their monthly payment by roughly 76%. For mid-career professionals, this choice matters enormously.

Disability Insurance (SSDI)

Social Security Disability Insurance provides income if you become unable to work before retirement age due to a serious medical condition. You don’t need to reach retirement age—disability can strike at any point.

SSDI requires that your condition is expected to last at least 12 months or result in death. Once approved, benefits continue until you reach full retirement age, when they convert to retirement benefits automatically.

Many mid-career workers overlook SSDI while healthy. That’s a mistake. The protection matters most when you’re young, earning peak income, and supporting dependents.

Survivors Benefits

If you die, your family receives income based on your earnings record. This isn’t charity—it’s life insurance you’ve already paid for.

Survivors benefits reach:

- Your spouse at any age (caring for children under 16)

- Your spouse at full retirement age or older

- Your unmarried children under 19 (up to 23 if in school)

- Your dependent parents age 62 or older

For a family of four, survivors benefits can total 150-180% of your own retirement benefit. That’s substantial protection.

Supplemental Security Income (SSI)

SSI helps low-income individuals who are age 65 or older, blind, or disabled. Unlike retirement benefits (based on your work history), SSI depends on current income and assets, not earnings history.

SSI recipients receive the same 2.8% cost-of-living adjustment in 2026. Most mid-career professionals won’t qualify unless circumstances change dramatically.

Here’s a quick summary of the four main types of Social Security benefits for 2026:

| Benefit Type | Who Qualifies | Typical Payouts/Impact | Key Eligibility Criteria |

|---|---|---|---|

| Retirement | Workers age 62+ | $2,071/month in 2026 | Based on 35-year earnings history |

| Disability (SSDI) | Disabled workers any age | Varies by earnings | Medical condition; 40 credits |

| Survivors | Families of deceased workers | 150-180% of worker’s benefit | Family relationship to worker |

| Supplemental Income (SSI) | Low-income, age 65+, disabled | Modest benefit, varies | Income/assets; not work history |

Mid-career means you have 15-35 years to build your Social Security record—understanding these four benefit types now shapes decisions that impact hundreds of thousands of dollars later.

Pro tip: Visit ssa.gov to estimate your specific benefit amount under different claiming ages—the difference between age 62 and 70 is often $500+ monthly, so run the numbers for your situation.

How Eligibility and Benefit Amounts Are Determined

Your Social Security benefit isn’t random. It’s calculated using a specific formula based on your earnings history and when you claim. Understanding this process removes the mystery and helps you make smarter decisions.

The 35-Year Earnings Foundation

Social Security looks at your highest 35 years of earnings. If you worked fewer than 35 years, zeros fill in the gaps, which reduces your benefit. This matters for career changers or those with unpaid time off.

Your earnings get indexed to wage growth. This means older earnings are adjusted upward to reflect how wages have grown nationwide. You’re not penalized for retiring into an economy that pays more.

The Social Security Administration averages these 35 years and divides by 420 months to create your Average Indexed Monthly Earnings (AIME). This single number drives everything that follows.

The Progressive Bend Points Formula

Here’s where Social Security protects lower earners. The benefit formula uses progressive bend points that give you a higher replacement rate if you earned less.

For 2026, the bend points are set at $1,286 and $7,749. Your AIME gets divided into segments, with different percentages applied to each:

- First segment: 90% of AIME up to $1,286

- Second segment: 32% of AIME between $1,286 and $7,749

- Third segment: 15% of AIME above $7,749

This progressive calculation means someone earning $30,000 yearly gets roughly 40% of previous income replaced, while someone earning $150,000 gets closer to 20%. The lower earner receives more relative protection.

Your Primary Insurance Amount (PIA)

The formula produces your Primary Insurance Amount (PIA)—your benefit at full retirement age. This is your baseline; everything else adjusts from here.

If you claim before full retirement age, your PIA reduces. Claiming at 62 cuts your benefit by roughly 30%. Delaying past full retirement age increases it by approximately 8% per year, reaching maximum at age 70.

Eligibility Thresholds

Retirement benefits begin at age 62. Disability benefits have no age requirement—you need 40 credits (roughly 10 years of work) and a serious medical condition.

Earnings above the taxable maximum ($184,500 in 2026) don’t count toward benefits. High earners hit this ceiling and stop paying into the system mid-year.

Your AIME is calculated once annually, but claiming age determines your actual monthly payment—a 35% difference between 62 and 70 is substantial over decades.

Pro tip: Request your Social Security statement at ssa.gov to verify your 35-year earnings record is accurate—errors compound and reduce your lifetime benefit by thousands.

New Rules, Taxes, and Cost-of-Living Changes for 2026

Every year brings adjustments to Social Security. 2026 is no exception. Understanding these changes now prevents surprises when your benefits shift or your tax situation changes.

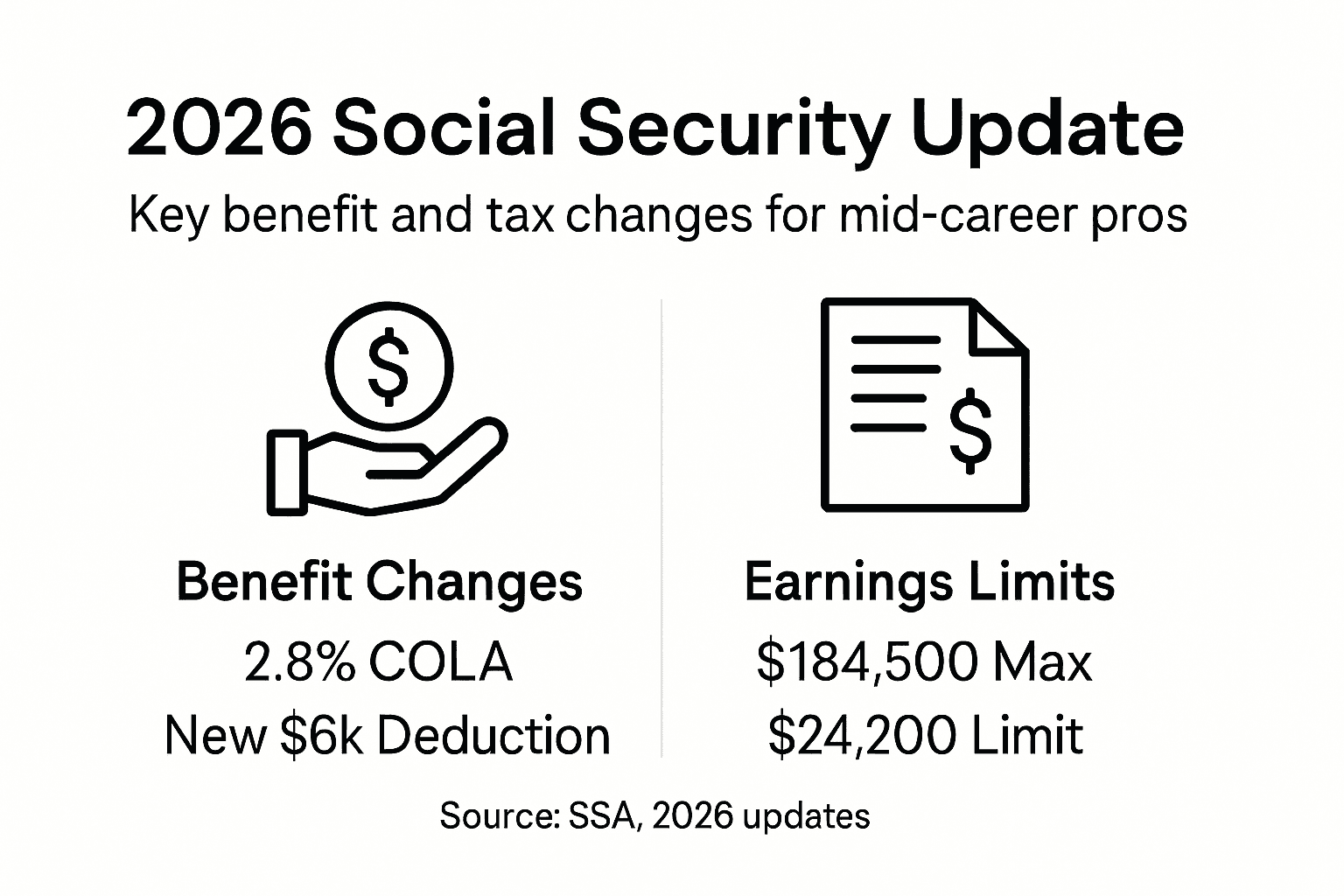

The 2.8% Cost-of-Living Adjustment (COLA)

Nearly 71 million beneficiaries will receive a 2.8% COLA increase in 2026. For the average retiree, this means roughly $56 additional monthly income, raising the typical retirement benefit to $2,071.

That sounds good until you account for Medicare. Part B premiums increase annually, eating into your COLA gain. Many retirees find their net benefit bump is smaller than the headline percentage suggests.

The COLA affects all benefit types: retirement, disability, survivors, and SSI. Everyone receiving Social Security gets the same adjustment.

Taxable Earnings Maximum Rises to $184,500

The maximum taxable earnings threshold increased to $184,500 for 2026. This affects two groups of people differently.

For high earners, it means paying more into Social Security. Once you hit $184,500 in annual income, you stop contributing to the system. If you earn $200,000, you pay taxes on $184,500 only.

For self-employed individuals (SECA), this threshold determines how much income gets taxed at the 15.3% combined rate. Earnings above it still face the Medicare portion (2.9%) but not the Social Security portion (12.4%).

Earnings Limits for Early Claimers

Claim before full retirement age and your benefits reduce if you earn too much. The 2026 earnings limit increases to $24,480 annually for workers under full retirement age.

Exceed this threshold, and Social Security reduces your benefit by 50 cents per dollar over the limit. Earn $25,480, lose $500 in benefits that month.

This rule matters for mid-career professionals considering early retirement. Working part-time while collecting early benefits can eliminate those benefits entirely.

The New $6,000 Tax Deduction

Starting in 2026, taxpayers age 65 and older gain a $6,000 above-the-line tax deduction. This reduces federal income tax on Social Security benefits directly.

This differs from the standard deduction increase. You get this $6,000 extra simply for being 65+, regardless of how much Social Security you receive. When combined with higher standard deductions overall, tax liability on benefits drops substantially.

Medicare Part B Premium Increases

Medicare Part B premiums rise annually, and 2026 is no exception. These increases partially offset your COLA gain. Check your specific premium—high-income earners pay more through Income-Related Monthly Adjustment Amounts (IRMAA).

A 2.8% benefit increase sounds significant until Medicare premiums rise and tax deductions change—the net gain depends on your individual situation, not just the headline number.

What Changes Affect Your Situation

Different rules apply depending on when you claim:

- Claiming at 62: Earnings limits matter; work too much and benefits vanish

- Claiming at full retirement age: Earnings limits don’t apply

- Claiming after 67: No earnings limits; maximize annual income plus growing benefits

- High income: New tax deduction helps; IRMAA may increase Medicare costs

- Low income: COLA boost matters most; tax planning strategies may reduce overall tax burden

Pro tip: Run your 2026 scenario through ssa.gov’s benefit calculator now—plug in different claiming ages and earnings amounts to see exact net impact after taxes and Medicare adjustments.

Risks, Shortfalls, and Planning Mistakes to Avoid

Social Security planning isn’t optional—it’s essential. Most people make preventable mistakes that cost tens of thousands in lost lifetime benefits. Knowing what to avoid puts you ahead of 90% of mid-career professionals.

The “Claim Early” Trap

Fear drives bad decisions. Many workers claim at 62 because they worry Social Security will disappear. This mistake costs roughly $200,000+ over a 30-year retirement.

Claiming at 62 versus 70 reduces your monthly benefit by 35-40%. That reduction never goes away—it sticks with you forever. Even if Social Security faces funding challenges, your reduced benefit remains locked in.

This table compares the financial impact of claiming Social Security at different ages:

| Claiming Age | Benefit Reduction/Increase | Potential Lifetime Impact | Strategy Considerations |

|---|---|---|---|

| Age 62 | 30-35% reduction | $200,000+ lost over decades | Early access, lower monthly amount |

| Full Retirement | Baseline benefit | Standard payout | Balances age and payout |

| Age 70 | 76% higher than age 62 | Maximized monthly and lifetime | Requires delaying to age 70 |

The math favors waiting if you live past 80. For most mid-career professionals with above-average health and family longevity, delaying is financially smarter.

Spousal Benefit Coordination Failures

Many couples ignore spousal and survivor benefits entirely. This is costly. A spouse can claim benefits based on your earnings record, even if they never worked.

Optimization requires strategy. If one spouse has higher lifetime earnings, coordinating when each claims can increase household benefits by $50,000 or more. Few people understand these rules exist.

Ignoring Life Expectancy and Health

You can’t claim Social Security intelligently without considering how long you’ll live. Someone with a family history of longevity should delay. Someone with serious health issues might claim earlier.

Common planning mistakes include making this decision based on rules of thumb rather than personal circumstances. Your situation is unique.

Working While Claiming Early

Claim benefits before full retirement age and work part-time? Your benefits shrink by 50 cents per dollar over the earnings limit ($24,480 in 2026).

Worse, you’re paying full payroll taxes on that income while receiving reduced benefits. You’re simultaneously funding someone else’s retirement and receiving less yourself. That’s a double penalty.

Neglecting Professional Guidance

Social Security decisions are too important for guesswork. The claiming decision alone impacts 30+ years of retirement. Yet most people decide alone, without running scenarios.

A financial advisor or Social Security specialist can model your specific situation—different claiming ages, spousal strategies, tax implications. The cost of guidance (often $500-2,000) pays back in months through optimized claiming.

Underestimating COLA Impact

Many mid-career professionals focus only on current benefit amounts. They ignore how cost-of-living adjustments compound over decades.

A 2.8% annual increase seems small. Over 30 years, it nearly doubles your benefit’s purchasing power. This matters more for those who delay claiming—higher benefits grow faster with COLA adjustments.

The biggest planning mistake isn’t claiming too early or too late—it’s claiming without a strategy that accounts for your health, longevity, spouse’s situation, and tax picture.

Mistakes to Watch For

- Claiming before understanding spousal benefits—costs thousands

- Not coordinating with spouse—leaves household benefits on table

- Ignoring your health and family history—leads to suboptimal timing

- Working early and collecting—triggers earnings limits and penalties

- Filing alone without professional review—misses optimization opportunities

Pro tip: Before claiming, run three scenarios at ssa.gov (age 62, full retirement age, age 70), then consult a fee-only financial advisor—the $1,000 investment prevents six-figure lifetime mistakes.

Take Control of Your Social Security Future Today

Navigating Social Security benefits can feel overwhelming with complex terms like Primary Insurance Amount and the impact of claiming age on your lifetime income. Mid-career professionals face critical decisions now that will define the financial security of their retirement and their family’s future. The article highlights common pitfalls such as claiming early without understanding spousal benefits and the effect of the 2.8% cost-of-living adjustment. If you want to avoid costly mistakes and maximize your benefits, you need clear, personalized guidance.

Don’t leave your financial future to chance. Visit finblog.com for expert insights and tailored strategies to help you optimize when and how to claim Social Security. Explore tools and professional advice that can help you run benefit scenarios and understand how new 2026 rules affect you. Take action now to strengthen your retirement plan with confidence—start shaping your Social Security strategy today at finblog.com.

Frequently Asked Questions

What are the different types of benefits provided by Social Security?

Social Security offers four main types of benefits: retirement benefits for workers aged 62 and older, disability insurance for those unable to work due to medical conditions, survivors benefits for the family of deceased workers, and supplemental security income (SSI) for low-income individuals who are aged 65 or older, blind, or disabled.

How is my Social Security benefit amount calculated?

Your Social Security benefit is calculated based on your highest 35 years of earnings, which are indexed to account for wage growth. This average is divided by 420 months to determine your Average Indexed Monthly Earnings (AIME), which is then used in a formula with progressive bend points to calculate your Primary Insurance Amount (PIA), your benefit at full retirement age.

When can I start claiming Social Security benefits?

You can start claiming retirement benefits as early as age 62. However, your monthly benefit will increase significantly if you wait until your full retirement age (typically 66-67) or until age 70, where you can maximize your benefit amount.

What should I consider if I plan to work while claiming Social Security early?

If you claim Social Security benefits before reaching full retirement age and earn above the annual threshold (which is $24,480 in 2026), your benefits will be reduced by 50 cents for every dollar earned over the limit. It’s essential to evaluate your work income and understand how it affects your benefits before making a decision.

Recommended

- Master Retirement Healthcare Planning for a Secure Future – Finblog

- Social Security – Finblog

- How to Save on Taxes: Proven Strategies for Professionals – Finblog

- COLA – Finblog

- Ο «οδικός χάρτης» για τα υποχρεωτικά self-tests εργαζομένων στον ιδιωτικό τομέα – Χρήστος Καβαλλάρης – Λογιστής

- Роль рынка труда 2025: почему это важно IT‑компаниям