Over 70 percent of american households with substantial assets now seek professional guidance to manage their growing wealth. Managing finances at this level involves much more than picking investments or tracking expenses. Without a solid strategy, opportunities can slip through the cracks and risks may go unchecked. By understanding what true wealth management covers and how it works, readers gain the tools to make better decisions for long-term financial security and peace of mind.

Table of Contents

- Defining Wealth Management Explained

- Types and Models In Wealth Management

- How Wealth Management Functions

- Legal Framework and Fiduciary Duty

- Risks, Costs, and Implications

- Alternatives and Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Comprehensive Wealth Management | Wealth management integrates various financial disciplines to create personalized strategies that align with individual goals and risk tolerance. |

| Fiduciary Duty | Wealth managers are legally obligated to act in their clients’ best interests, ensuring transparency and ethical conduct in financial decision-making. |

| Dynamic Strategies | Continuous monitoring and adaptation of wealth management strategies are essential to respond to changing circumstances and market conditions. |

| Alternatives and Risks | Individuals should be aware of alternatives to traditional wealth management and the potential risks associated with self-directed investing and automated services. |

Defining Wealth Management Explained

Wealth management represents a comprehensive financial strategy that goes far beyond simple investment advice. At its core, wealth management is a professional service designed to help individuals and families optimize their financial resources, protect assets, and achieve long-term financial goals. This holistic approach integrates multiple financial disciplines, including investment planning, tax strategies, retirement planning, estate management, and risk mitigation.

The primary objective of wealth management is to create a personalized financial roadmap tailored to an individual’s unique circumstances, risk tolerance, and aspirational objectives. Financial professionals who specialize in wealth management work closely with clients to develop sophisticated strategies that maximize wealth accumulation while minimizing potential risks. These strategies often involve complex wealth preservation techniques that consider an individual’s entire financial ecosystem.

Wealth management differs significantly from basic financial planning by offering a more integrated and proactive approach. While traditional financial planning might focus on individual aspects like retirement savings or investment selection, wealth management takes a 360-degree view of a client’s financial health. This comprehensive approach means addressing interconnected financial elements such as investment portfolio diversification, tax efficiency, insurance protection, and generational wealth transfer strategies.

Key components of effective wealth management include strategic asset allocation, continuous portfolio monitoring, tax-efficient investing, and adaptive financial planning. Successful wealth management requires ongoing collaboration between financial professionals and clients, ensuring that strategies evolve alongside changing personal circumstances, market conditions, and broader economic trends. By providing personalized guidance and sophisticated financial insights, wealth management empowers individuals to make informed decisions that support their long-term financial prosperity.

Types and Models In Wealth Management

Wealth management encompasses diverse models that cater to different financial needs and client profiles. Comprehensive wealth management typically falls into several distinct categories, each designed to address specific financial objectives and complexity levels. These models range from basic advisory services to highly sophisticated, personalized wealth strategies that integrate multiple financial disciplines.

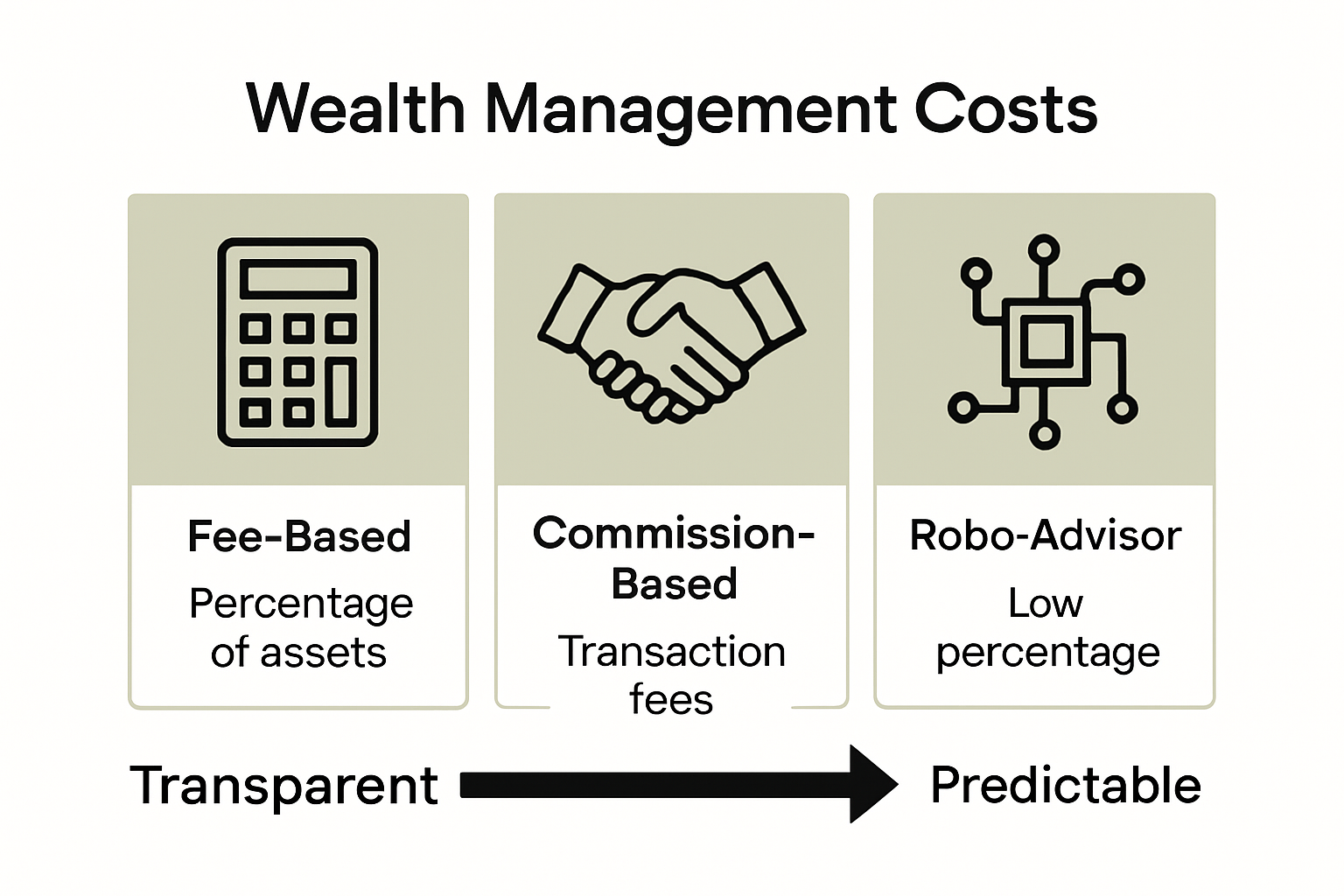

The first primary model is the fee-based advisory approach, where financial professionals provide comprehensive guidance for a structured fee. These professionals typically offer strategic investment portfolio management that goes beyond traditional investment recommendations. Another prominent model is the asset-based wealth management model, which calculates fees as a percentage of total assets under management, incentivizing advisors to grow and protect client wealth effectively.

For high-net-worth individuals, private wealth management represents a more exclusive model characterized by highly personalized services. This approach includes advanced strategies like sophisticated tax planning, estate management, philanthropic advisory, and intergenerational wealth transfer. These models often involve dedicated financial teams working exclusively with clients to develop complex, multifaceted financial strategies that address intricate wealth preservation and growth objectives.

Additional wealth management models include robo-advisory platforms, which leverage algorithmic technology to provide automated investment management, and hybrid models that combine digital platforms with human expertise. Each model offers unique advantages, and the most appropriate approach depends on an individual’s financial complexity, net worth, risk tolerance, and specific long-term financial goals. The key is selecting a wealth management model that provides the right balance of personalized guidance, technological efficiency, and comprehensive financial strategy.

How Wealth Management Functions

Wealth management operates through a sophisticated, multi-step process designed to create a comprehensive financial strategy tailored to individual client needs. The fundamental mechanism begins with an extensive initial consultation where financial professionals conduct a thorough assessment of a client’s current financial landscape, including income, assets, liabilities, risk tolerance, and long-term financial objectives.

The core functional process involves several critical stages of financial planning and execution. After the initial assessment, wealth managers develop a customized strategy that typically includes strategic wealth transfer approaches to optimize asset preservation and generational financial planning. This involves creating a detailed financial roadmap that integrates multiple disciplines such as investment management, tax planning, retirement strategies, estate planning, and risk mitigation.

Continuous monitoring and adaptive management represent another crucial functional aspect of wealth management. Financial professionals regularly review and rebalance investment portfolios, track market conditions, and proactively adjust strategies to align with changing personal circumstances, economic shifts, and evolving financial goals. This dynamic approach ensures that the wealth management strategy remains responsive and optimized, addressing potential risks and capitalizing on emerging financial opportunities.

Technology plays an increasingly significant role in how wealth management functions, enabling more sophisticated analysis, real-time portfolio tracking, and enhanced communication between clients and financial advisors. Modern wealth management integrates advanced analytics, predictive modeling, and digital platforms to provide more precise, personalized financial guidance. The ultimate function of wealth management is to transform complex financial information into actionable strategies that help clients build, protect, and transfer wealth across generations, creating a comprehensive approach to financial success.

Legal Framework and Fiduciary Duty

The legal framework surrounding wealth management is built upon the fundamental principle of fiduciary responsibility, which establishes a legally binding obligation for financial professionals to act in their clients’ best financial interests. This critical legal standard requires wealth managers to prioritize client welfare above their personal or institutional financial gains, creating a relationship of trust, transparency, and absolute ethical commitment.

Fiduciary duty encompasses several key legal requirements that wealth managers must consistently meet. These include the duty of loyalty, which mandates that financial advisors avoid conflicts of interest, and the duty of care, which demands that professionals exercise reasonable expertise and diligence when managing client assets. Wealth transfer strategies must be executed with meticulous attention to legal compliance, ensuring that all financial recommendations align with the client’s expressed goals and risk tolerance.

Regulatory bodies such as the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) provide comprehensive oversight of wealth management practices. These organizations establish stringent guidelines that mandate transparency, require detailed disclosure of potential risks, and enforce strict standards for professional conduct. Wealth managers must maintain comprehensive documentation, provide clear and accurate information about investment strategies, and continuously demonstrate their commitment to acting in their clients’ best financial interests.

The legal framework also protects clients through mandatory licensing, ongoing professional education requirements, and potential legal recourse if a wealth manager breaches their fiduciary responsibilities. This multilayered approach ensures that financial professionals are held to the highest standards of professional conduct, providing clients with confidence that their financial futures are being managed with the utmost integrity, expertise, and legal protection. The combination of ethical obligations and robust regulatory oversight creates a comprehensive system designed to safeguard individual financial interests and maintain the highest levels of professional accountability in wealth management.

Risks, Costs, and Implications

Wealth management involves a complex landscape of financial risks that require careful navigation and strategic planning. Market volatility represents one of the most significant potential risks, with investment portfolios constantly exposed to economic fluctuations, geopolitical events, and unexpected market shifts that can dramatically impact financial performance. Understanding and mitigating these risks becomes a critical component of effective wealth management strategies.

The cost structure of wealth management services varies widely, typically involving multiple fee components that clients must carefully evaluate. Wealth transfer strategies often include management fees ranging from 0.5% to 1.5% of total assets annually, with additional transaction costs, performance fees, and potential advisory charges. These expenses can significantly impact long-term investment returns, making it essential for clients to understand the full financial implications of professional wealth management services.

Beyond direct financial risks, wealth management carries potential implications related to personal financial autonomy and decision-making. Clients must carefully balance the expertise of financial professionals with their personal financial goals, understanding that delegating financial management does not eliminate personal responsibility. The most successful wealth management relationships emerge from collaborative partnerships that maintain transparency, open communication, and aligned financial objectives.

Technological advancements and regulatory changes continuously reshape the risk landscape of wealth management. Cybersecurity threats, regulatory compliance challenges, and evolving market dynamics create an environment of constant adaptation. Sophisticated wealth management approaches now integrate advanced risk assessment technologies, predictive modeling, and comprehensive scenario planning to provide clients with more robust, resilient financial strategies that can withstand complex economic uncertainties.

Alternatives and Common Pitfalls

Wealth management is not a one-size-fits-all solution, and individuals have multiple alternatives to consider based on their financial complexity, resources, and personal preferences. Self-directed investing represents one primary alternative, where individuals take complete control of their investment decisions, utilizing online platforms and personal research to manage their financial portfolios without professional intervention.

Another significant alternative involves robo-advisory services, which leverage algorithmic technology to provide automated investment management at lower costs. These digital platforms offer strategic wealth transfer approaches that can be particularly attractive for younger investors or those with smaller asset bases. However, these alternatives come with their own set of potential pitfalls, including limited personalization, reduced human interaction, and potential gaps in comprehensive financial planning.

Common pitfalls in wealth management frequently stem from unrealistic expectations, poor communication, and fundamental misunderstandings about investment strategies. Investors often make critical mistakes such as attempting to time the market, failing to diversify their investment portfolios, or becoming emotionally reactive to short-term market fluctuations. These errors can significantly undermine long-term financial growth and stability, highlighting the importance of disciplined, strategic financial management.

Technology and financial innovation continue to expand alternatives to traditional wealth management, including peer-to-peer investment platforms, cryptocurrency investments, and decentralized finance options. While these emerging alternatives offer exciting possibilities, they also introduce complex risk factors that require sophisticated understanding. The most successful financial strategies often involve a balanced approach, potentially combining professional wealth management services with selective self-directed investments, always maintaining a clear understanding of individual financial goals and risk tolerance.

Take Control of Your Financial Future with Expert Wealth Management Guidance

Understanding the complexities of wealth management can feel overwhelming. This article highlighted key challenges like market volatility, tax-efficient investing, and managing intergenerational wealth transfer. If you are seeking to protect your assets and build a personalized financial roadmap that adapts to your goals and risks you are not alone. Many investors struggle with maintaining clear communication with advisors and selecting the right management approach for their unique situation.

At finblog.com, we provide you with expert insights and tailored solutions designed to simplify these complex concepts. Explore our resources on strategic investment portfolio management and proven wealth transfer strategies to gain confidence in securing your financial legacy. Take the first step toward making informed decisions that safeguard your prosperity. Visit our site now to start your journey toward smarter wealth management and experience a new level of financial clarity.

Frequently Asked Questions

What is wealth management?

Wealth management is a comprehensive financial service aimed at helping individuals and families optimize their financial resources, protect assets, and achieve long-term financial goals through personalized strategies that encompass various financial disciplines.

How does wealth management differ from traditional financial planning?

Wealth management takes a holistic approach by integrating multiple areas such as investment management, tax planning, estate management, and risk mitigation, while traditional financial planning typically focuses on single aspects like retirement savings or investment selection.

What are the types of wealth management models available?

Wealth management includes various models such as fee-based advisory, asset-based management, private wealth management for high-net-worth individuals, robo-advisory platforms, and hybrid models that combine digital and human expertise. The choice depends on an individual’s financial complexity and goals.

What are the key risks associated with wealth management?

Key risks in wealth management include market volatility, potential cost structures impacting returns, and maintaining personal financial autonomy. Effective strategies should account for these risks through diversification and continuous monitoring.