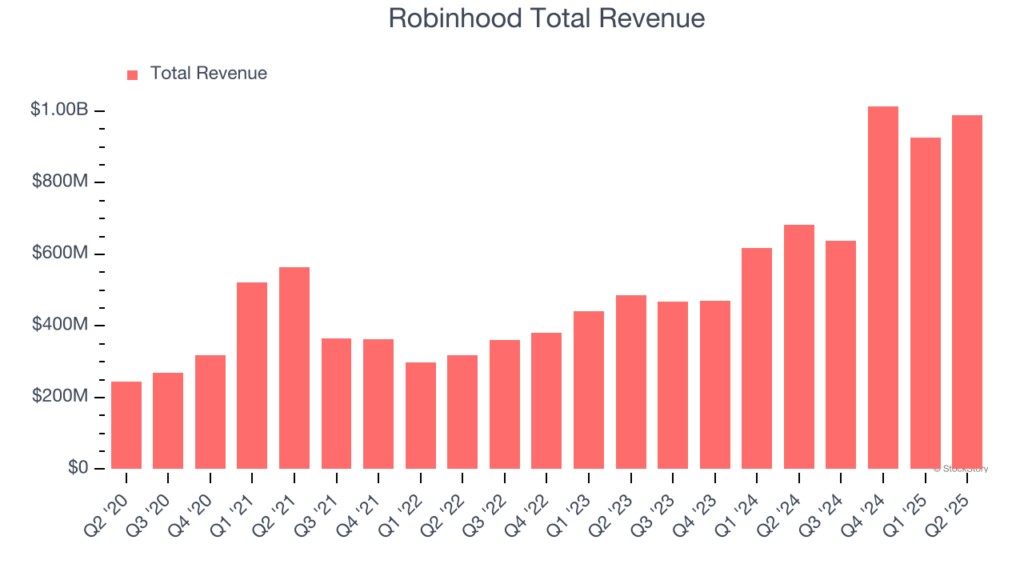

Robinhood (HOOD) is set to report Q3 2025 earnings after the market closes today, following a blockbuster year that’s seen the stock surge over 250% year-to-date. The catalyst? A massive rebound in retail trading activity, surging crypto volumes, and soaring net interest income. With both equities and digital assets roaring back to life, Wall Street is looking to see if Robinhood’s trading platform and financial superapp strategy can continue translating into top-line growth and profitability.

Yet the bar is high. Analysts have raised their estimates sharply in recent weeks, betting on crypto transaction revenue, growing assets under custody, and strong monetisation via Robinhood Gold. But with implied volatility suggesting a ±9–10% swing post-earnings, expectations are fully loaded.

Street Forecast: Explosive Growth, But a High Bar

| Metric | Q3 2025 Consensus Estimate | YoY Growth (vs Q3 2024) |

|---|---|---|

| Revenue (Net) | ~$1.21 B | +~90% |

| GAAP EPS | ~$0.51-$0.53 | +200% |

| Adjusted EBITDA | ~$570 M | +113% |

| Monthly Active Users | ~13.3 M | +21% |

| ARPU (Revenue/MAU) | ~$181 | +72% |

Sources: Nasdaq, Zacks, Robinhood IR, and FactSet consensus estimates.

Prediction: Robinhood beats on both revenue and EPS, driven by crypto, options, and interest income. Guidance commentary and regulatory updates will determine the stock’s post-earnings direction.

Trading Revenue: Options and Crypto in Overdrive

Robinhood’s core business has roared back to life:

- Options trading revenue is expected to exceed $300M this quarter (+49% YoY), making it the largest single contributor. Elevated volatility, increased contracts per trader, and product innovation (e.g., index options) have supported growth.

- Equities trading revenue is forecast at ~$82M (+123% YoY), helped by higher volumes from returning retail traders. The recent spike in meme stocks and small-cap speculation further supports this rebound.

Prediction: Transaction-based revenue beats forecasts, led by record crypto and options activity.

Crypto: From Rebound to Rocketship

Robinhood is emerging as one of the biggest crypto brokers in the U.S.:

- Q3 crypto transaction revenue is expected around $314M, a staggering +415% YoY surge.

- The rollout of crypto staking, expanded coin offerings, and wallet functionality has deepened user engagement.

- The acquisition of Bitstamp earlier this year is expected to enhance institutional crypto execution and staking income.

Prediction: Crypto revenue surprises to the upside, driving more than 25% of total revenue. Look for guidance on future expansion and regulatory stance.

Net Interest Income: Quiet Powerhouse

Robinhood’s interest income has become a consistent cash engine, thanks to:

- Margin loan balances, which are up significantly as risk appetite returns.

- Cash sweep income, which has risen with assets under custody now exceeding $300B.

- Analysts expect over $385M in Q3 interest income (+40% YoY), driven by both higher balances and favorable yields.

Prediction: Solid NII performance provides margin stability. Fed rate expectations will color commentary.

Robinhood Gold and Subscriptions: Premium ARPU Gains

- Robinhood Gold continues to grow, with ~2.2M subscribers as of Q2.

- Analysts expect over $68M in “other revenue,” including Gold and crypto-related services.

Prediction: Recurring revenue shows stable growth, though still small relative to trading and interest.

Users, MAUs, and Engagement

- Monthly active users (MAUs) are expected at 13.3M, up from 11.0M last year.

- Funded accounts are ~26.9M, with net deposits trending positively.

- ARPU has risen to ~$181/quarter, up sharply from ~$105 a year ago.

Prediction: Solid engagement trends continue, though user growth likely moderates as comparisons get tougher.

Regulatory Risk: PFOF in the Spotlight

- Robinhood paid $45M earlier this year to settle past SEC issues, but more scrutiny is possible.

- The payment-for-order-flow (PFOF) model remains vulnerable to regulatory overhaul, which could challenge Robinhood’s commission-free model.

- Crypto-related regulation is another wild card, especially with staking and custody rules still evolving.

Prediction: No new enforcement announced, but management will likely reaffirm commitment to evolving within regulatory bounds.

Profitability and Margins: Leverage at Work

- Operating leverage is accelerating: each $1 in revenue adds significantly to bottom-line growth.

- GAAP EPS of ~$0.51 would represent triple-digit YoY gains.

- SBC (stock-based compensation) is being managed tightly, despite higher stock prices.

Prediction: Adjusted EBITDA margins remain near 50%, with solid cash generation.

Analyst Sentiment and Valuation

- Robinhood is rated a Moderate Buy, with a $144 average price target.

- Some analysts have raised targets above $160, citing crypto tailwinds and institutional expansion.

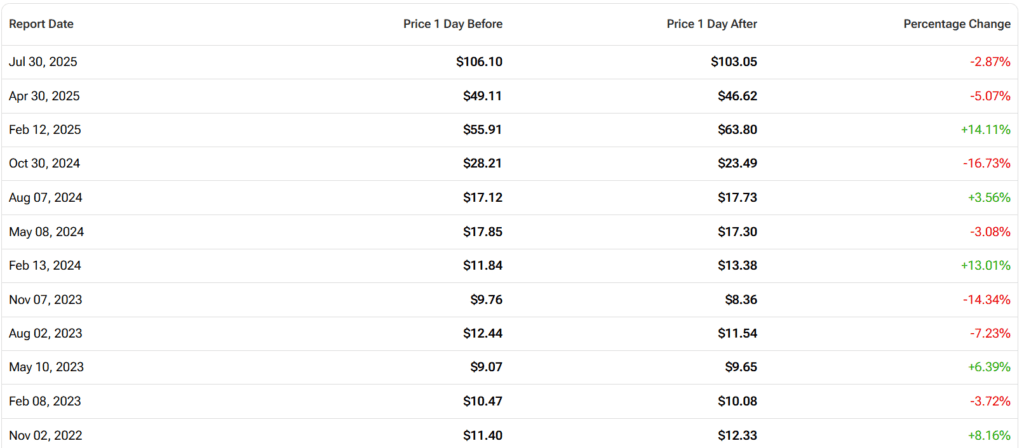

- Options markets imply a ±9.5% move post-earnings, suggesting high expectations.

Prediction: Beat could lead to a 5–10% upside; any miss or regulatory surprise may cause a sharper pullback.

Will Robinhood Keep Surging?

Robinhood enters Q3 earnings with high expectations — and good reason. Its exposure to crypto, options, and retail momentum positions it to outperform, but investors have priced in much of the upside. The focus will be on continued monetization, user stickiness, and regulatory clarity.

Our Call: Robinhood delivers a clean beat on both revenue and EPS. Unless guidance disappoints or regulation takes centre stage, the stock likely trades higher, potentially retesting 2025 highs.

Disclosure: All predictions and insights shared in this article are based on a comprehensive review of publicly available analyst reports, media coverage, and market consensus. These views are for informational purposes only and do not constitute investment advice. Please conduct your own research or consult a licensed financial advisor before making any investment decisions.