Everyone wants to grow their money, but knowing where to start with investing feels overwhelming for most people. Nearly 60% of Americans admit they do not have a clear investment strategy or even know their risk tolerance. Most think investing is about picking hot stocks or timing the market. That is where the real secret hides—successful investing actually begins with getting to know yourself and building a plan that fits your financial goals, not someone else’s.

Table of Contents

- Step 1: Analyze Your Financial Goals And Risk Tolerance

- Step 2: Research Different Investment Options And Sectors

- Step 3: Create A Diversified Investment Plan

- Step 4: Monitor Market Trends And Adjust Your Portfolio

- Step 5: Review Your Investment Performance Regularly

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess financial goals and risk tolerance | Understand your personal financial situation to tailor your investment strategy effectively. |

| 2. Diversify investment options and sectors | Combine various types of assets to mitigate risks and enhance potential returns across your portfolio. |

| 3. Regularly monitor market trends | Stay informed on market changes to make strategic adjustments, ensuring alignment with your financial goals. |

| 4. Conduct periodic performance reviews | Evaluate your investment outcomes against benchmarks to learn and adapt your strategy for continual growth. |

| 5. Adjust investments based on changing life circumstances | Update your portfolio and strategy regularly to reflect your evolving financial situation and goals. |

Step 1: Analyze Your Financial Goals and Risk Tolerance

Before diving into investment strategies, understanding your financial landscape is crucial. Think of this step as creating a personal financial roadmap that will guide your entire investment journey. Your financial goals and risk tolerance are the foundation of a successful investment strategy.

Begin by taking a comprehensive look at your current financial situation. What are you hoping to achieve? Are you saving for retirement, planning to buy a home, funding your children’s education, or building a general wealth portfolio? Each goal requires a different approach. Retirement might allow for more aggressive investments with a longer time horizon, while a down payment fund needs a more conservative strategy to protect your capital.

Risk tolerance is equally critical in how to pick investments. This isn’t just about numbers it’s about your emotional and financial comfort with potential market fluctuations. Some investors can handle significant market swings without losing sleep, while others become anxious with even minor portfolio changes. According to FINRA, your risk tolerance is influenced by several key factors:

- Your current age and years until you need the invested money

- Your overall financial stability and income

- Your emotional capacity to withstand potential investment losses

- Your existing financial obligations and emergency savings

To accurately assess your risk tolerance, consider creating a detailed financial snapshot. Calculate your monthly income, essential expenses, existing savings, and future financial obligations. This exercise helps you understand how much investment risk you can realistically accommodate without compromising your financial security.

A practical approach involves categorizing your financial goals into short-term (1-3 years), medium-term (3-10 years), and long-term (10+ years) objectives. Each category will have a different risk profile. Short-term goals require more conservative investments to preserve capital, while long-term goals can incorporate more aggressive growth strategies that can weather market volatility.

Use this checklist to ensure you have thoroughly analyzed your financial situation before making any investment decisions. Checking off each item will help clarify your goals and risk tolerance as recommended in Step 1.

| Checklist Item | Completion Status |

|---|---|

| Calculate monthly income and list essential expenses | [ ] |

| Identify existing savings and emergency funds | [ ] |

| List current and future financial obligations | [ ] |

| Define short-, medium-, and long-term financial goals | [ ] |

| Estimate time horizon for each goal | [ ] |

| Reflect on emotional comfort with investment risk | [ ] |

| Assign a personalized risk tolerance profile (low/medium/high) | [ ] |

Remember, risk tolerance is not static. As your life circumstances change your investment strategy should adapt. A young professional might have a higher risk tolerance compared to someone nearing retirement. Regularly reassessing your financial goals and risk comfort ensures your investment strategy remains aligned with your evolving life situation.

By the end of this step, you should have a clear understanding of your financial objectives, a realistic assessment of your risk tolerance, and a preliminary framework for how you will approach investment selections. This foundational work will make subsequent investment decisions more strategic and personally tailored.

Step 2: Research Different Investment Options and Sectors

Now that you understand your financial goals and risk tolerance, it’s time to explore the vast world of investment opportunities. Researching different investment options is like building a diversified toolkit for your financial future. You want a mix of tools that work together to help you achieve your objectives while managing potential risks.

Start by understanding the primary investment categories. Stocks represent ownership in a company, offering potential growth and sometimes dividends. Bonds are essentially loans to governments or corporations that provide steady interest payments. Mutual funds and exchange-traded funds (ETFs) allow you to invest in a collection of stocks or bonds, spreading your risk across multiple assets. Real estate investment trusts (REITs) provide exposure to property markets without directly owning physical property.

According to the U.S. Securities and Exchange Commission, each investment type comes with unique characteristics and risk levels. Stocks typically offer higher potential returns but also higher volatility. Bonds tend to be more stable but usually provide lower returns. Understanding these dynamics helps you create a balanced investment strategy.

Develop a systematic approach to research. Begin by reading financial news from reputable sources like The Wall Street Journal, Bloomberg, or Financial Times. These publications offer insights into market trends, economic conditions, and sector performance. Online platforms like Morningstar, Yahoo Finance, and Google Finance provide free tools for comparing investment performance, analyzing sector trends, and tracking market movements.

Consider exploring different investment sectors. Technology, healthcare, energy, finance, and consumer goods are major sectors with distinct growth patterns. Some sectors perform better during economic expansions, while others are more resilient during downturns. Diversification across sectors can help mitigate risk and optimize potential returns.

Here is a table comparing common types of investment options discussed in this guide. Use it to quickly understand their features, risk levels, and typical roles in a balanced portfolio.

| Investment Type | Description | Typical Risk Level | Role in Portfolio |

|---|---|---|---|

| Stocks | Ownership in a company; potential growth, dividends | High | Growth, long-term wealth |

| Bonds | Loan to government or corporation; pays interest | Low to Medium | Income, stability |

| Mutual Funds/ETFs | Pool of various stocks or bonds; instant diversification | Varies | Diversification, cost efficiency |

| REITs | Investment in property markets without direct ownership | Medium | Income, diversification |

| Cash Equivalents | Examples include money market funds, CDs | Low | Liquidity, safety |

Key research tools and resources to leverage include:

- Financial websites with comprehensive market data

- Investment research platforms with analyst reports

- Economic indicators and government financial publications

- Podcasts and webinars from financial experts

- Company annual reports and financial statements

As you research, pay attention to historical performance, but remember that past performance doesn’t guarantee future results. Look for consistent performers with strong fundamentals. Consider factors like company leadership, innovation potential, market share, and competitive advantages.

By the end of this step, you should have a comprehensive understanding of various investment options, their characteristics, and potential roles in your portfolio. You’ll be equipped with the knowledge to make informed decisions that align with your financial goals and risk tolerance.

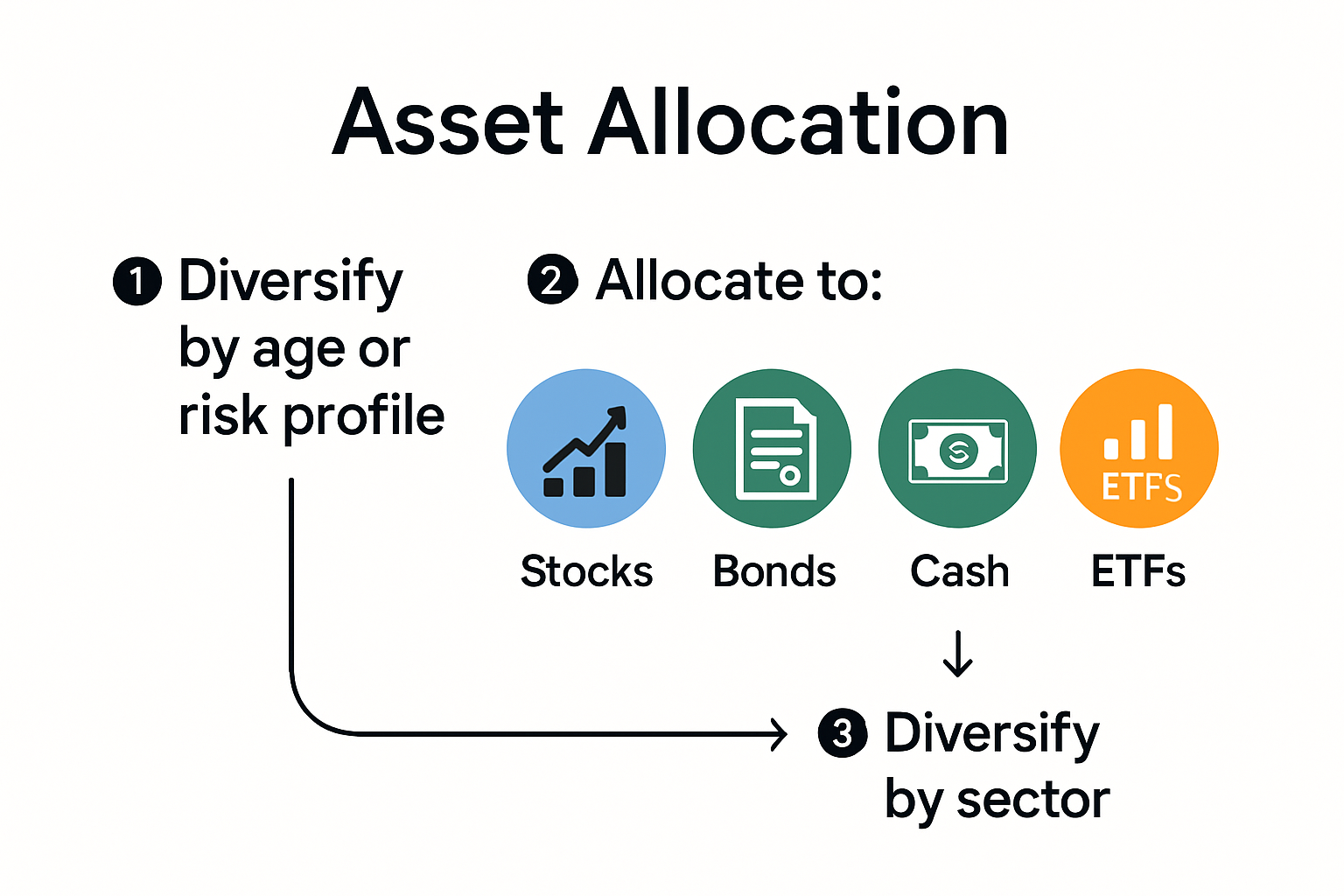

Step 3: Create a Diversified Investment Plan

Diversification is your financial safety net, transforming your investment strategy from a high-risk gamble to a calculated approach that balances potential growth with risk management. Think of your investment portfolio like a well-designed garden where different plants support and protect each other against environmental challenges.

Begin by allocating your investments across multiple asset classes. The traditional approach involves spreading your money among stocks, bonds, and cash equivalents. Younger investors might lean towards a more stock-heavy portfolio, while those closer to retirement typically shift towards more conservative bond and cash investments. Your asset allocation should directly reflect your risk tolerance and financial goals.

According to FINRA, effective diversification means more than just owning different investments. It requires strategic selection across various sectors, market capitalizations, and geographic regions. Consider creating a mix that includes large-cap and small-cap stocks, domestic and international markets, and different industry sectors like technology, healthcare, finance, and consumer goods.

A practical strategy involves percentage-based allocation. A common starting point for younger investors might be 80% stocks and 20% bonds, while those nearing retirement might reverse that ratio. Within each category, further diversify. For stocks, this means investing across different sectors and company sizes. For bonds, consider a mix of government and corporate bonds with varying maturity dates.

Key considerations for building your diversified investment plan include:

- Matching asset allocation to your specific time horizon

- Balancing potential returns with your personal risk tolerance

- Regularly reviewing and rebalancing your portfolio

- Minimizing unnecessary investment fees

- Considering tax-efficient investment strategies

Utilize low-cost index funds and ETFs to achieve broad market exposure without the complexity of selecting individual stocks. These investment vehicles provide instant diversification by tracking entire market indexes. Robo-advisors and online investment platforms can also help automate the diversification process, offering algorithmic portfolio management based on your risk profile.

Remember that diversification is not a one-time event but an ongoing process. Economic conditions, personal circumstances, and market dynamics change. Plan to review your investment portfolio annually, rebalancing to maintain your target asset allocation. This might mean selling some investments that have grown beyond their target percentage and reinvesting in underrepresented areas.

By the end of this step, you’ll have a comprehensive, personalized investment plan that spreads risk across multiple assets, positioning you to potentially weather market fluctuations while working towards your financial objectives.

Step 4: Monitor Market Trends and Adjust Your Portfolio

Investment success is not about setting and forgetting your portfolio, but actively staying informed and adaptable. Monitoring market trends is like being a financial detective, constantly gathering intelligence that helps you make strategic investment decisions. Your portfolio is a living entity that requires regular check-ups and occasional adjustments to remain healthy and aligned with your financial goals.

Establish a consistent monitoring routine that balances detailed analysis with a measured approach. Set aside time monthly or quarterly to review your investment performance. Create a dashboard using financial tracking tools like Personal Capital, Mint, or your brokerage platform’s portfolio analysis features. These tools provide comprehensive views of your investment performance, asset allocation, and comparative market benchmarks.

According to the Government Finance Officers Association, effective portfolio management requires understanding market risk and developing robust tracking mechanisms. Pay attention to key economic indicators that signal potential market shifts, such as GDP growth, unemployment rates, inflation data, and federal reserve policies. These broader economic signals can help you anticipate potential investment landscape changes.

Learn to distinguish between short-term market noise and meaningful long-term trends. Not every market fluctuation requires an immediate portfolio adjustment. Develop a disciplined approach that focuses on substantial, sustained changes rather than reacting to daily market volatility. This might mean setting specific thresholds that would trigger a portfolio review, such as a 10-15% deviation from your target asset allocation.

Critical elements to track during your portfolio monitoring include:

- Overall portfolio performance against benchmark indexes

- Individual investment performance

- Changes in asset allocation percentages

- Emerging economic and sector-specific trends

- Personal financial goal progression

Consider using dollar-cost averaging as a strategy to manage market uncertainty. This approach involves consistently investing a fixed amount at regular intervals, which helps smooth out market price fluctuations and reduces the risk of making large investments at inopportune moments.

Diversification becomes even more critical during market volatility. If certain sectors or investments have significantly outperformed or underperformed, you might need to rebalance. This could involve selling portions of overperforming assets and reinvesting in underrepresented sectors to maintain your original asset allocation strategy.

Utilize technology to your advantage. Many investment platforms offer automated alerts for significant portfolio changes, performance milestones, or recommended rebalancing actions. Mobile apps and online dashboards can provide real-time insights, making portfolio monitoring more accessible and less time-consuming.

By the end of this step, you’ll have established a systematic approach to monitoring your investments, enabling you to make informed, strategic decisions that keep your portfolio aligned with your financial objectives.

Step 5: Review Your Investment Performance Regularly

Performance review is the compass that guides your investment journey, transforming raw financial data into actionable insights. Think of this step as a comprehensive health check for your investment portfolio, where you diagnose strengths, identify potential weaknesses, and chart a course for future financial growth.

Establish a structured review schedule that aligns with your investment goals. For most individual investors, a quarterly review provides the right balance between staying informed and avoiding overreaction to short-term market fluctuations. Some investors prefer an annual deep dive, supplemented by quarterly check-ins. Choose a frequency that matches your investment complexity and personal comfort level.

According to the U.S. Securities and Exchange Commission, evaluating investment performance goes beyond simply checking returns. Compare your portfolio’s performance against appropriate benchmark indexes that reflect your investment mix. For instance, if you have a balanced portfolio of stocks and bonds, compare your returns against a blended index that similarly represents those asset classes.

Develop a comprehensive performance evaluation framework that considers multiple dimensions. Look beyond pure returns and examine risk-adjusted performance metrics. Key indicators include your portfolio’s overall return, performance relative to benchmarks, volatility, and how well your investments align with your original financial objectives. Pay attention to the performance of individual investments, but avoid making impulsive decisions based on short-term fluctuations.

Critical elements to assess during your performance review include:

- Total portfolio return compared to relevant market indexes

- Performance of individual investment assets

- Changes in your asset allocation

- Tax efficiency of your investments

- Alignment with your original financial goals

Leverage technology to streamline your review process. Many investment platforms offer sophisticated performance tracking tools that generate detailed reports, visualize your portfolio’s performance, and provide comparative analytics. Robo-advisors and financial management apps can automate much of this analysis, offering insights that might be difficult to generate manually.

Maintain meticulous records of your investment decisions, transactions, and the reasoning behind them. This documentation serves as a valuable reference point, helping you understand your investment thought process and learn from both successful and unsuccessful strategies. Create a simple spreadsheet or use portfolio tracking software to log your investments, purchase dates, prices, and rationale.

Remember that performance review is not just about numbers it’s about continuous learning and adaptation. If your investments consistently underperform or no longer align with your financial goals, be prepared to make strategic adjustments. This might involve rebalancing your portfolio, changing your asset allocation, or exploring alternative investment strategies.

By the end of this step, you’ll have transformed raw investment data into a clear, actionable roadmap for your financial future, equipped with insights that can help you make more informed investment decisions.

Unlock Your Smartest Investment Decisions with Personalized Guidance

Are you feeling uncertain about how to match your investments to your real financial goals? Building wealth in 2025 demands clarity and confidence, especially when decisions like asset allocation, risk tolerance, and ongoing portfolio review shape your long-term security. This article showed how critical it is to create a tailored investment plan and continuously monitor your progress, but putting these insights into action often feels overwhelming when you are navigating alone.

That is where finblog.com steps in. Our expert guidance connects the dots between your current financial challenges and smart, realistic investment strategies. Ready to stop guessing and start growing? Visit finblog.com now to discover tools, expert tips, and secure lead forms designed for investors like you. Take charge of your wealth-building strategy and set yourself up for financial success today.

Frequently Asked Questions

What are the steps to analyze my financial goals and risk tolerance?

Start by evaluating your current financial situation, including your income, expenses, and savings. Define your financial goals, such as retirement or buying a home, and assess your comfort with market fluctuations. Consider factors like age, financial stability, and your emotional response to risks to understand your risk tolerance better.

How can I diversify my investment portfolio effectively?

To diversify your investment portfolio, allocate your assets across different classes such as stocks, bonds, and cash. Include various sectors (e.g., technology, healthcare) and market capitalizations. Regularly rebalance your portfolio to maintain your target asset allocation, which should align with your risk tolerance and financial goals.

How often should I review my investment performance?

It’s recommended to review your investment performance quarterly or at least annually. This balance allows you to respond to significant changes while avoiding impulsive reactions to short-term market fluctuations. Compare your portfolio’s performance against relevant benchmarks and adjust your strategy as needed.

What tools can I use to monitor market trends and my investment portfolio?

Utilize financial tracking tools like Personal Capital or Mint for monitoring your investments. Many brokerages also offer built-in analytics. Keep an eye on key economic indicators, financial news, and use mobile apps for real-time insights to stay updated on market conditions and effectively manage your portfolio.