Debt can sneak into almost every part of modern life and for many, it is just part of growing up. But one fact stands out. The average American household carries over $101,000 in debt. That might sound overwhelming at first and yet the true surprise is how manageable debt can become with the right steps in place. Some of the smartest strategies are also the simplest and they can lead to genuine financial freedom.

Table of Contents

- Understanding Different Types of Debt

- Setting Up A Realistic Repayment Plan

- Smart Habits To Control Spending

- Leveraging Professional Help And Resources

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand types of debt | Familiarize yourself with secured and unsecured debts to make informed financial choices. |

| Create a detailed repayment plan | Assess all debts and develop a plan using the SMART method to track your progress. |

| Differentiate needs and wants | Distinguish essential expenses from discretionary spending to avoid unnecessary debt accumulation. |

| Leverage professional resources | Utilize credit counseling and financial advice to create effective debt management strategies. |

| Build an emergency fund | Save 3-6 months of living expenses to protect against unexpected financial challenges. |

Understanding Different Types of Debt

Debt is a financial reality that most people encounter throughout their lives. While debt often carries a negative connotation, understanding its various forms can help you make more informed financial decisions. Consumer.gov defines debt as money owed to another party, which can take multiple shapes and serve different purposes in personal and professional financial landscapes.

Secured vs Unsecured Debt

Two primary categories of debt differentiate how financial obligations are structured. Secured debt is backed by collateral – an asset that the lender can claim if you fail to repay the loan. Mortgages and auto loans are classic examples of secured debt. When you take out a mortgage, your home serves as collateral, meaning the lender can foreclose on the property if you default on payments.

Here is a comparison table outlining the key characteristics of secured and unsecured debt to give you a clear understanding of how each type differs.

| Type of Debt | Requires Collateral? | Common Examples | Typical Interest Rates |

|---|---|---|---|

| Secured Debt | Yes | Mortgages, Auto Loans | Usually lower |

| Unsecured Debt | No | Credit Cards, Personal Loans | Usually higher |

Unsecured debt, by contrast, does not require collateral. Credit cards and personal loans typically fall into this category. Because these debts are riskier for lenders, they often come with higher interest rates. Finance in the Classroom notes that unsecured debt relies primarily on the borrower’s creditworthiness and promise to repay.

Common Types of Debt

Understanding the landscape of debt helps individuals make strategic financial choices. According to GuideStonе, there are several prevalent debt types:

Below is a summary table of the most common types of debt, including their main purpose and typical use as described in the article.

| Debt Type | Main Purpose | Typical Use |

|---|---|---|

| Mortgage Loans | Finance home purchase | Buying a house/real estate |

| Auto Loans | Purchase vehicles | Buying a car or other vehicles |

| Student Loans | Fund education | Tuition, books, education-related expenses |

| Credit Card Debt | Everyday purchases | Groceries, entertainment, routine expenses |

| Personal Loans | Flexible personal needs | Home improvements, emergencies, other needs |

- Mortgage Loans: Used to finance home purchases, typically representing the largest long-term financial commitment for many individuals.

- Auto Loans: Specifically designed for vehicle purchases through banks or dealerships.

- Student Loans: Financial instruments enabling educational pursuits by covering tuition, books, and related expenses.

- Credit Card Debt: A revolving form of credit used for everyday purchases and transactions.

- Personal Loans: Flexible financial tools used for various personal needs like home improvements or unexpected expenses.

Each debt type carries unique characteristics, interest rates, and repayment structures. The key is understanding how these different forms of debt can impact your overall financial health. While debt isn’t inherently negative, mismanagement can lead to significant financial strain.

When considering taking on debt, carefully evaluate the purpose, terms, interest rates, and your ability to make consistent repayments. A strategic approach to debt management involves understanding not just the immediate financial need, but also the long-term implications of your borrowing decisions.

Setting Up a Realistic Repayment Plan

Creating a realistic debt repayment plan requires strategic thinking and disciplined financial management. The goal is not just to eliminate debt but to do so in a way that maintains your financial stability and prevents future financial stress.

Assess Your Current Financial Landscape

National Credit Union Administration recommends starting by conducting a comprehensive financial audit. This involves listing all outstanding debts, including their interest rates, minimum payments, and total balances. Understanding the full scope of your financial obligations provides a clear starting point for your repayment strategy.

Begin by gathering all debt-related documents. Create a detailed spreadsheet that includes:

- Creditor names

- Current balance

- Interest rates

- Minimum monthly payments

- Payment due dates

Implementing the SMART Debt Repayment Strategy

University of Florida’s Institute of Food and Agricultural Sciences suggests using the SMART framework for debt management. This approach transforms debt repayment from an overwhelming challenge into a structured, achievable goal:

- Specific: Clearly define exact debt amounts you want to pay off

- Measurable: Track your progress with concrete metrics

- Achievable: Set realistic goals based on your current financial situation

- Relevant: Ensure the plan aligns with your broader financial objectives

- Time-bound: Assign specific target dates for debt elimination

Two popular debt repayment methods can help you stay motivated and make consistent progress:

The table below outlines the main differences between the Debt Snowball and Debt Avalanche methods to help you choose a repayment strategy that aligns with your financial goals.

| Method | Primary Focus | Motivation Strategy | Main Advantage |

|---|---|---|---|

| Debt Snowball | Smallest balance first | Quick wins build momentum | Increases motivation |

| Debt Avalanche | Highest interest rate first | Saves more on overall interest | Pays off debt faster financially |

- Debt Snowball Method: Focus on paying off the smallest debt first, creating psychological momentum.

- Debt Avalanche Method: Prioritize debts with the highest interest rates to minimize overall interest payments.

Consider exploring additional income sources or reducing expenses to accelerate your debt repayment. Every extra dollar you can put toward debt brings you closer to financial freedom. Cut unnecessary subscriptions, negotiate bills, and look for ways to increase your income through side gigs or freelance work.

Remember that a realistic repayment plan is flexible. Life happens, and unexpected expenses can derail even the most carefully crafted strategy. Build some buffer into your plan and be prepared to adjust as your financial situation changes. The key is consistency and commitment to your long-term financial health.

Smart Habits to Control Spending

Controlling spending is a critical skill in managing personal finances and preventing unnecessary debt accumulation. MyMoney.gov emphasizes that effective spending management starts with understanding your financial behaviors and creating intentional strategies to guide your financial decisions.

Budgeting and Expense Tracking

The foundation of controlling spending lies in creating a comprehensive budget. Consumer Financial Protection Bureau recommends developing SMART financial goals that are Specific, Measurable, Achievable, Relevant, and Time-bound. Start by tracking every single expense for a month to gain a clear picture of your spending patterns.

Consider using digital tools or apps that can automatically categorize your expenses. Look for recurring patterns such as:

- Unnecessary subscription services

- Frequent impulse purchases

- High dining out or entertainment expenses

- Recurring small purchases that add up quickly

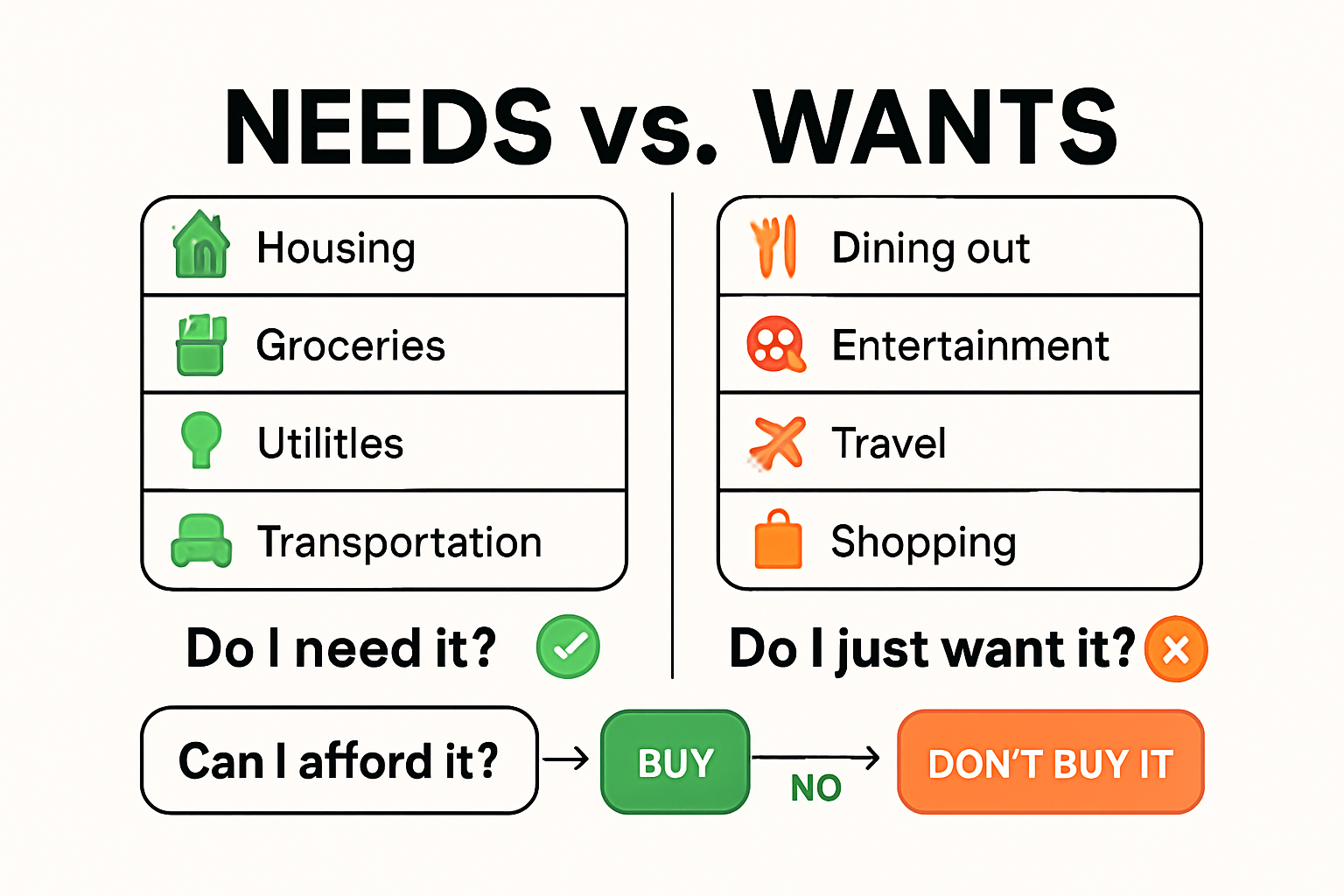

Distinguishing Needs from Wants

University of Central Florida highlights the importance of understanding the critical difference between needs and wants. Needs are essential expenses required for basic living like housing, food, healthcare, and transportation. Wants are discretionary expenses that enhance comfort but are not strictly necessary.

Develop a strategic approach to managing wants:

- Implement a 24-hour rule for non-essential purchases

- Create a discretionary spending budget

- Use cash or prepaid cards for entertainment and extras

- Wait for sales and use price comparison tools

Practical strategies can significantly reduce unnecessary spending. Before making any purchase, ask yourself: Is this a need or a want? Can I delay this purchase? Are there more cost-effective alternatives?

Additionally, build financial resilience by creating an emergency fund. This buffer prevents you from accumulating debt when unexpected expenses arise. Aim to save 3-6 months of living expenses in an easily accessible account.

Remember that controlling spending is not about complete deprivation but about making intentional, informed financial choices. Small consistent changes in spending habits can lead to significant long-term financial improvements. Stay patient, track your progress, and celebrate financial milestones along your journey to better money management.

Leveraging Professional Help and Resources

Navigating complex financial challenges often requires more than individual effort. Professional resources can provide expert guidance, strategic insights, and structured approaches to managing debt effectively. Consumer Financial Protection Bureau emphasizes that professional financial assistance can be a critical tool in achieving long-term financial stability.

Credit Counseling Services

My Credit Union recommends credit counseling as a valuable resource for individuals struggling with debt management. These services, often provided by nonprofit organizations, offer comprehensive financial guidance designed to help you regain control of your financial situation.

Credit counselors can assist you by:

- Developing personalized budget strategies

- Providing money management workshops

- Negotiating with creditors on your behalf

- Creating detailed debt management plans

- Offering educational resources about financial health

Types of Professional Financial Assistance

California Department of Financial Protection and Innovation highlights several professional resources available to individuals seeking debt management support:

- Certified Credit Counselors: Professionals trained to provide comprehensive financial advice and develop strategic debt reduction plans.

- Debt Settlement Services: Organizations that negotiate with creditors to reduce the total amount of debt you owe.

- Financial Advisory Firms: Professional consultants who offer holistic financial planning and debt management strategies.

When selecting a professional service, conduct thorough research. Look for organizations with:

- Transparent fee structures

- Proven track records

- Positive client testimonials

- Accreditation from recognized financial institutions

- Clear communication about their services

Be cautious of services that promise instant debt elimination or charge excessive upfront fees. Legitimate financial professionals will provide realistic timelines and transparent guidance.

Remember that seeking professional help is not a sign of financial failure but a proactive step toward financial recovery. These resources are designed to empower you with knowledge, strategies, and support to overcome financial challenges and build a more stable financial future.

Most initial consultations are free, allowing you to explore options without additional financial strain. Take advantage of these opportunities to gain insights, understand your financial landscape, and develop a personalized strategy for debt management and financial growth.

Frequently Asked Questions

What are the different types of debt I should be aware of?

Understanding the two main types of debt—secured and unsecured—is crucial. Secured debt is backed by collateral, such as a house or car, while unsecured debt, like credit cards and personal loans, is not collateralized and typically has higher interest rates.

How can I create a realistic debt repayment plan?

Start by conducting a financial audit to assess all your debts, including balances and interest rates. Next, use the SMART framework to set specific, measurable, achievable, relevant, and time-bound goals for debt repayment. Choose a repayment strategy such as the Debt Snowball or Debt Avalanche method to stay motivated.

What are effective strategies to control spending?

To control spending, create a detailed budget and track all expenses for a month. Distinguish between needs and wants, implement a 24-hour rule before making non-essential purchases, and consider using cash for discretionary spending to limit expenses.

How can professional help assist in managing my debt?

Credit counseling services can provide personalized strategies, negotiate with creditors, and help develop a detailed debt management plan. Certified credit counselors and financial advisory firms offer insights that can empower you to regain control of your financial situation.

Ready to Break Free from Debt? Take the First Step Toward Financial Freedom

If you feel overwhelmed by high-interest balances or struggle to find a realistic repayment plan, you are not alone. Many readers of our guide on debt management want to transform their financial landscape but are unsure where to start. Building a SMART debt repayment strategy and learning to distinguish needs from wants are powerful first moves, but sometimes you need an expert by your side to achieve real progress.

Now is the perfect time to act. Let our team at finblog.com support you with personalized guidance, educational resources, and hands-on financial strategies. Explore proven solutions, receive professional insights, and access secure consultation opportunities directly on our main website. Take control of your finances and set yourself up for a debt-free future today. Fill out our streamlined, secure form to connect with a financial advisor who understands your journey and can help you achieve your goals.