Nearly 60 percent of adults admit they feel unprepared when it comes to investing their money. Building a solid investment plan begins with understanding where you stand financially and setting clear, realistic goals that match your needs. If you want lasting financial growth, choosing the right investments and regularly reviewing your progress can make a real difference. This guide walks you through the essential steps to create a confident investment strategy from the ground up.

Table of Contents

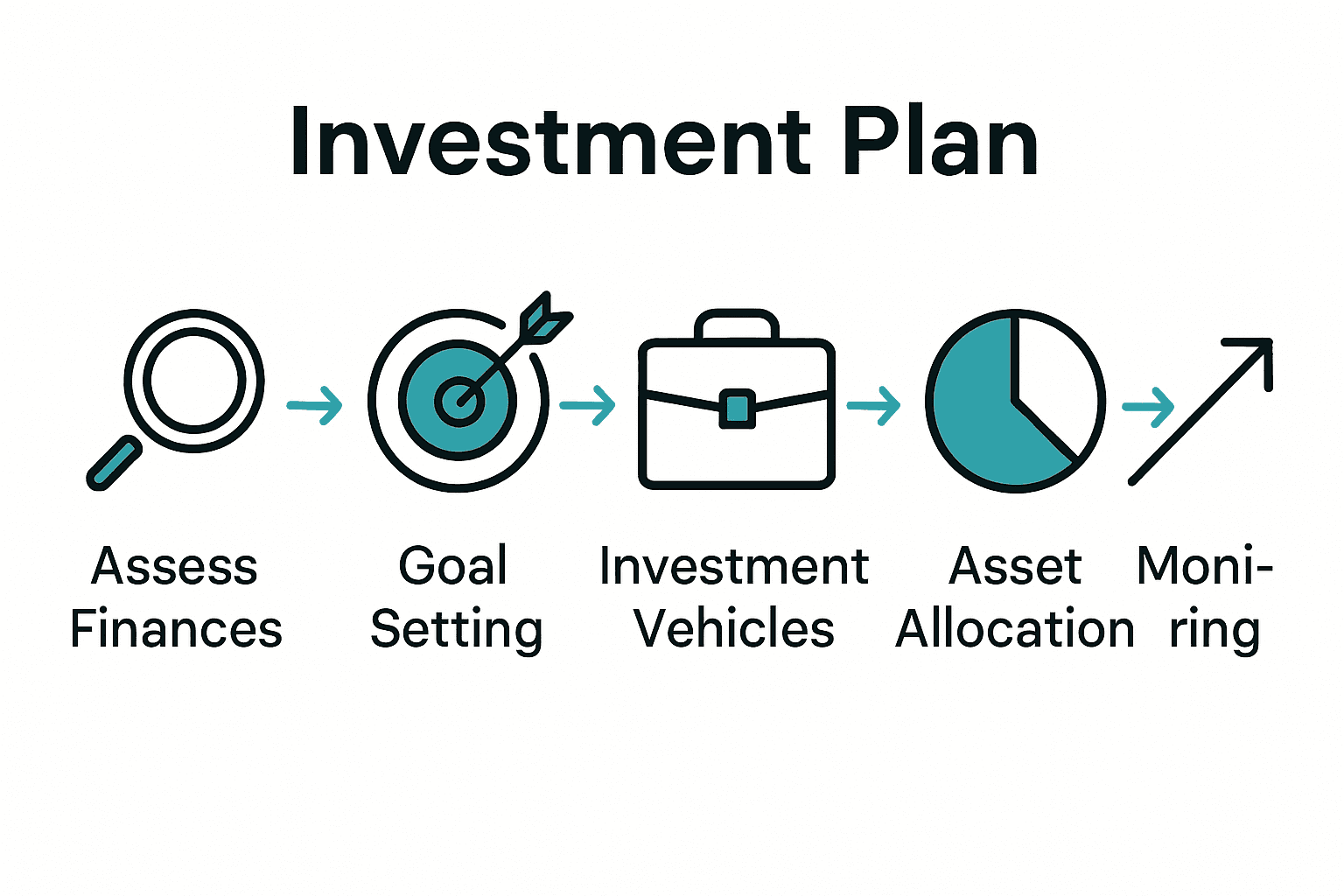

- Step 1: Assess Your Financial Situation

- Step 2: Define Clear Investment Goals

- Step 3: Select Suitable Investment Vehicles

- Step 4: Allocate Assets Strategically

- Step 5: Monitor and Adjust Your Plan

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess your financial situation first | Evaluate your current finances by gathering documents and understanding your income, expenses, and net worth. |

| 2. Define clear investment goals | Create specific, measurable, and realistic investment objectives based on your financial timeline and comfort with risk. |

| 3. Choose appropriate investment vehicles | Match investment options to your goals, risk tolerance, and desired returns; consider stocks, bonds, mutual funds, and ETFs. |

| 4. Strategically allocate your assets | Distribute investments across various asset classes to balance risk and returns, adjusting based on your risk profile. |

| 5. Monitor and adjust your plan regularly | Review and rebalance your investment portfolio at least once a year or after major life changes to stay aligned with goals. |

|

|

Step 1: Assess Your Financial Situation

Assessing your financial situation is the critical foundation of creating a successful investment plan. This initial step provides a comprehensive snapshot of your current financial landscape and helps you understand where you stand before making strategic investment decisions.

To thoroughly evaluate your financial health, start by gathering detailed financial documents including bank statements, pay stubs, tax returns, investment account information, and records of all outstanding debts. According to the Consumer Financial Protection Bureau, a comprehensive financial assessment should examine key aspects such as your ability to control finances, capacity to absorb financial shocks, and progress toward personal financial goals.

As you compile your financial information, focus on calculating three critical metrics: your total monthly income, comprehensive monthly expenses, and current net worth. Break down your income sources including salary, investments, side hustles, and passive income streams. Categorize expenses into fixed costs (rent, utilities, insurance) and variable expenses (entertainment, dining out, shopping). Subtract your total liabilities (debts, loans) from your total assets (cash, investments, property) to determine your current net worth.

Take special attention to identify potential financial vulnerabilities. Brookings Institution recommends examining income stability, debt levels, and savings capacity as key indicators of financial well being. Create an honest assessment of your financial strengths and weaknesses to guide your investment strategy.

Be prepared to make tough decisions. Your current financial situation might reveal areas needing immediate attention such as high-interest debt or insufficient emergency savings. This assessment is not about judgment but about creating a clear roadmap for financial improvement and future investment success.

Ready to move forward? The next step involves setting clear and achievable financial goals based on the comprehensive picture you have just created.

Step 2: Define Clear Investment Goals

Defining clear investment goals transforms your financial strategy from a vague aspiration to a targeted roadmap. This critical step helps you translate your financial dreams into actionable, measurable objectives that will guide every investment decision you make.

Start by creating specific and realistic investment goals that align with your unique financial situation and timeline. Government Finance Officers Association emphasizes the importance of developing investment objectives that match your individual risk tolerance and financial constraints. Break down your goals into three primary categories: short term (1-3 years), medium term (3-7 years), and long term (7+ years).

For each goal, quantify the exact amount of money you want to accumulate and the specific timeframe for achieving it. If you are saving for retirement, calculate the total amount you will need based on your desired lifestyle and expected expenses. For shorter term goals like purchasing a home or funding education, determine the precise dollar amount required. Consider factors such as inflation, potential investment returns, and your current savings rate.

When defining your investment goals, be honest about your risk tolerance. Some individuals are comfortable with more aggressive investment strategies that offer higher potential returns but also carry greater risk. Others prefer more conservative approaches that prioritize capital preservation. Your goals should reflect a balanced approach that matches your personal financial comfort level and long term objectives.

Remember that investment goals are not set in stone. As your life circumstances change your goals will evolve too. Build flexibility into your plan and commit to reviewing and adjusting your investment strategy annually. This approach ensures your financial plan remains dynamic and responsive to your changing needs.

With your investment goals now clearly defined, you are ready to move on to the next crucial step developing a strategic investment strategy that will help you turn these goals into reality.

Step 3: Select Suitable Investment Vehicles

Selecting the right investment vehicles is a crucial step in transforming your financial goals from abstract concepts to tangible opportunities. This stage involves carefully matching your unique financial objectives with investment options that align with your risk tolerance and expected returns.

Investor.gov provides a comprehensive overview of various investment products that can help you build a robust financial strategy. Understanding the characteristics of different investment vehicles is essential. Stocks offer potential for high returns but come with higher volatility, while bonds provide more stable income with lower risk. Mutual funds and exchange traded funds (ETFs) allow you to diversify your investments by pooling resources across multiple securities.

When selecting investment vehicles, consider your personal financial landscape. Young investors with longer time horizons might lean towards more aggressive options like growth stocks or emerging market funds. Those closer to retirement may prefer conservative investments such as government bonds or blue chip stock funds. The key is creating a balanced portfolio that spreads risk across different asset classes while maintaining alignment with your specific financial goals.

Pay close attention to fees, tax implications, and liquidity when choosing your investment vehicles. Some investments like mutual funds carry management expenses that can erode returns over time. ETFs often provide more cost effective options with greater transparency. Consider consulting with a financial advisor who can help you navigate the nuanced world of investment selection.

Dont forget to periodically review and rebalance your investment portfolio. As your life circumstances change your investment strategy should adapt. By remaining flexible and informed, you can optimize your investment vehicles to maximize potential returns while managing risk.

With your investment vehicles carefully selected, you are now prepared to develop a strategic allocation strategy that will help you achieve your financial objectives.

Step 4: Allocate Assets Strategically

Strategic asset allocation is the cornerstone of building a resilient investment portfolio that can weather market fluctuations while helping you achieve your financial objectives. This critical step involves intelligently distributing your investments across different asset classes to balance risk and potential returns.

Begin by understanding the fundamental asset classes: stocks, bonds, cash equivalents, and potentially alternative investments like real estate or commodities. Asset Allocation Strategies Guide can provide deeper insights into creating a balanced approach. A typical portfolio might allocate percentages based on your age and risk tolerance for example, younger investors might target 80% stocks and 20% bonds, while those near retirement might reverse those proportions.

Consider your personal risk profile when determining asset allocation. If you have a high risk tolerance and longer investment horizon, you can afford to be more aggressive with your stock allocations. Conservative investors or those closer to retirement should lean towards more stable investments like government bonds and blue chip stocks. The goal is creating a portfolio that can generate returns while protecting your principal investment.

Develop a systematic approach to rebalancing your portfolio annually. Market performance will naturally shift your asset percentages over time, so periodic adjustments help maintain your intended risk level. Some investors use the 5% rule meaning if any asset class deviates more than 5% from its target allocation, its time to realign your investments.

Remember that asset allocation is not a one time event but an ongoing process. Your investment strategy should evolve with your life stages, financial goals, and changing market conditions. Stay informed, be flexible, and dont hesitate to consult financial professionals who can provide personalized guidance.

With your assets strategically allocated, you are now ready to implement your investment plan and begin your journey toward financial growth.

Step 5: Monitor and Adjust Your Plan

Monitoring and adjusting your investment plan is a critical ongoing process that ensures your financial strategy remains aligned with your evolving goals and changing market conditions. This step transforms your investment approach from a static document to a dynamic roadmap that adapts to your life journey.

U.S. Securities and Exchange Commission emphasizes the importance of periodically reviewing and rebalancing investment portfolios. Set a consistent schedule for reviewing your investments at least once per year or after significant life events such as marriage, career change, or approaching a major financial milestone. During these reviews, assess how your current portfolio performance compares to your original financial objectives and risk tolerance.

Develop a systematic approach to tracking your investments. Utilize digital tools and investment platforms that offer comprehensive performance tracking and real time analytics. Look beyond simple returns and examine how each asset class is performing relative to your overall strategy. Pay special attention to individual investments that may have drifted significantly from their original allocation or are underperforming compared to market benchmarks.

Be prepared to make strategic adjustments when necessary. This doesnt mean reactive trading based on short term market fluctuations but rather thoughtful rebalancing to maintain your desired risk profile. Consider factors like changes in your personal financial situation, approaching retirement, or significant shifts in global economic conditions. Sometimes adjusting means reducing exposure to certain asset classes or diversifying into new investment vehicles that better match your current goals.

Remember that emotional decision making can be detrimental to long term investment success. Develop a disciplined approach that relies on data and your predefined strategy rather than market panic or overexcitement. Keep detailed records of your investment decisions and periodically evaluate the reasoning behind past adjustments to refine your future approach.

With a robust monitoring and adjustment strategy in place, you have transformed your investment plan from a static document into a living financial strategy that can grow and adapt alongside your personal journey.

Take Control of Your Financial Future Today

Building a solid investment plan requires more than just knowledge it demands clear goals, strategic choices, and ongoing adjustments. If you have felt overwhelmed by assessing your financial situation or uncertain about selecting the right investment vehicles this guide provides the clarity you need. Stop letting uncertainty hold you back from reaching your financial potential.

Discover how to move confidently through each step from defining achievable goals to smartly allocating your assets. Explore expert insights and customized guidance at finblog.com that will support you in monitoring and adjusting your investment plan as markets and personal goals evolve. Ready to transform your financial roadmap into a dynamic plan aligned with your aspirations? Visit finblog.com now and start your journey toward financial success with personalized advice and trusted resources at your fingertips.

Frequently Asked Questions

How do I assess my financial situation before creating an investment plan?

To assess your financial situation, gather financial documents like bank statements, pay stubs, tax returns, and debt records. Calculate your total monthly income, expenses, and net worth to get a clear picture of your financial health.

What should I include when defining my investment goals?

When defining your investment goals, categorize them by timeframes: short-term (1-3 years), medium-term (3-7 years), and long-term (7+ years). Specify the amount of money you want to accumulate for each goal and be clear about your risk tolerance to align your strategy accordingly.

How can I select suitable investment vehicles for my goals?

Select investment vehicles by matching them to your financial objectives and risk tolerance. Consider options like stocks for high growth potential, bonds for stable income, or mutual funds for diversification, based on your personal preferences and timeline.

What does strategic asset allocation involve in my investment plan?

Strategic asset allocation involves distributing your investments across various asset classes like stocks and bonds to balance risk and returns. Regularly review and adjust your allocations based on your risk profile and life changes, typically aiming for an allocation that reflects your age and risk comfort level.

How often should I monitor and adjust my investment plan?

You should monitor and adjust your investment plan at least once a year or following significant life events such as a job change. Set a consistent schedule for reviewing performance against your goals to ensure your strategy remains effective and responsive to your circumstances.