Markets opened on Wednesday under heavy pressure, with global stocks extending losses after Wall Street’s sharp pullback on valuation fears, CEO warnings, and renewed risk-off sentiment. Investors are now bracing for the Supreme Court’s landmark tariff ruling later today — a decision President Trump called “one of the most important in US history.”

Yesterday’s Recap: Tech-Led Slide & Valuation Warnings

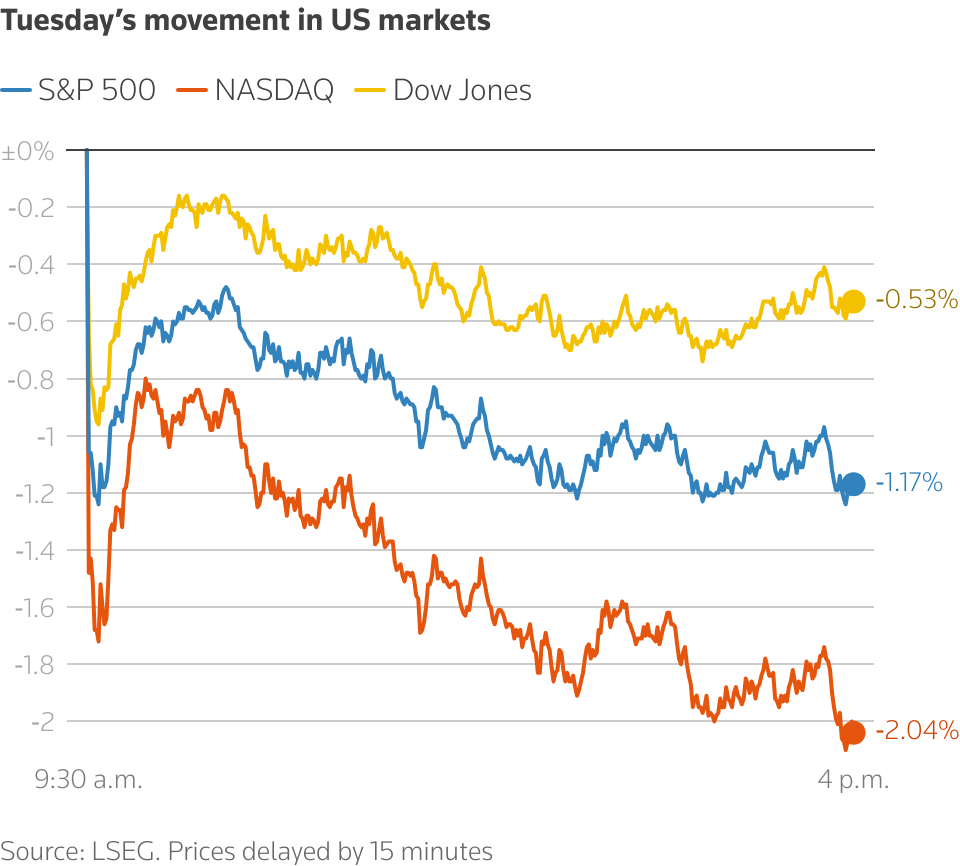

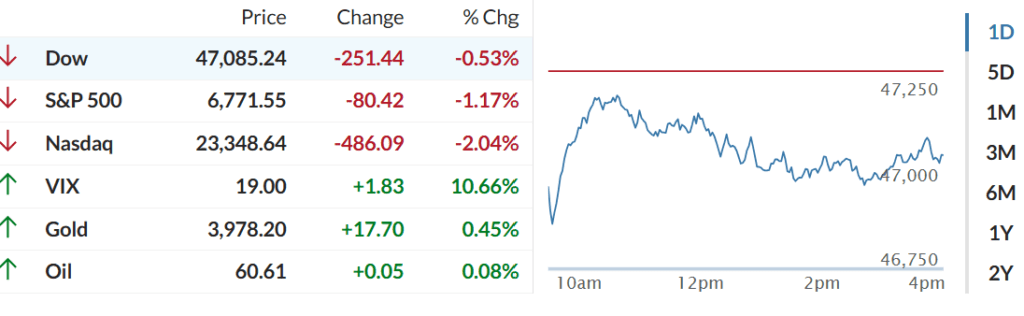

US markets sold off sharply Tuesday as concerns about overvalued tech and AI stocks rattled sentiment.

- S&P 500: −0.66%

- Nasdaq: −1.15%

- Dow Jones: −0.2%

Despite strong earnings from Palantir, Uber, and Super Micro Computer, investors punished high-multiple stocks amid warnings from top Wall Street executives. (More about: Markets Fall as CEOs Warn of Correction Ahead)

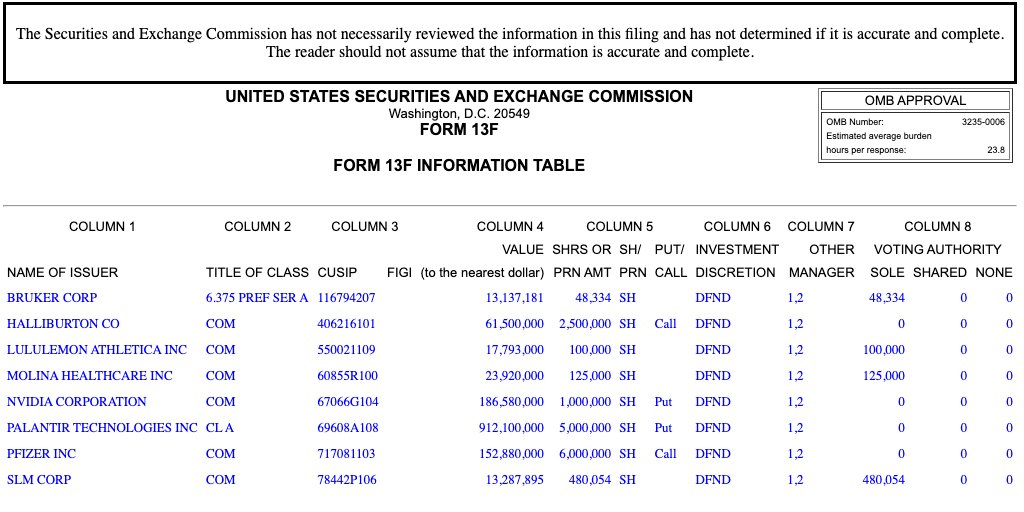

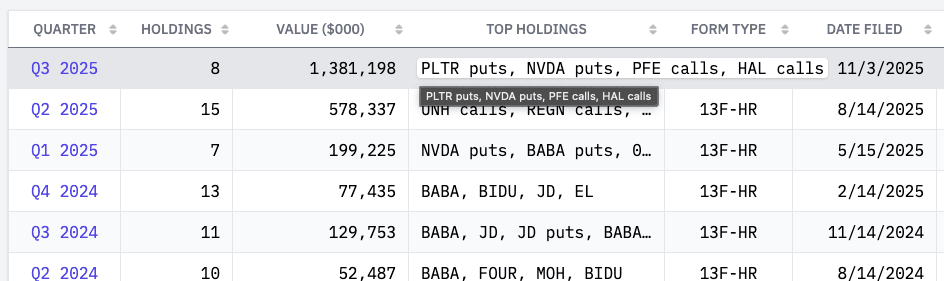

Plus, Michael Burry’s Scion Asset Management has revealed new bearish bets against major AI stocks, filing puts on Palantir ($PLTR) and Nvidia ($NVDA), alongside calls on Pfizer ($PFE) and Halliburton ($HAL). The move sent shockwaves through the market Tuesday, with Palantir plunging nearly 8% after Burry’s disclosure reignited fears of overvaluation in the AI trade. The famed “Big Short” investor controls over $1.3 billion in positions, around 80% of it reportedly tied to short bets on Nvidia and Palantir.

Palantir’s CEO called Burry’s move “madness,” while investors viewed it as a symbolic challenge to the ongoing AI bull run.

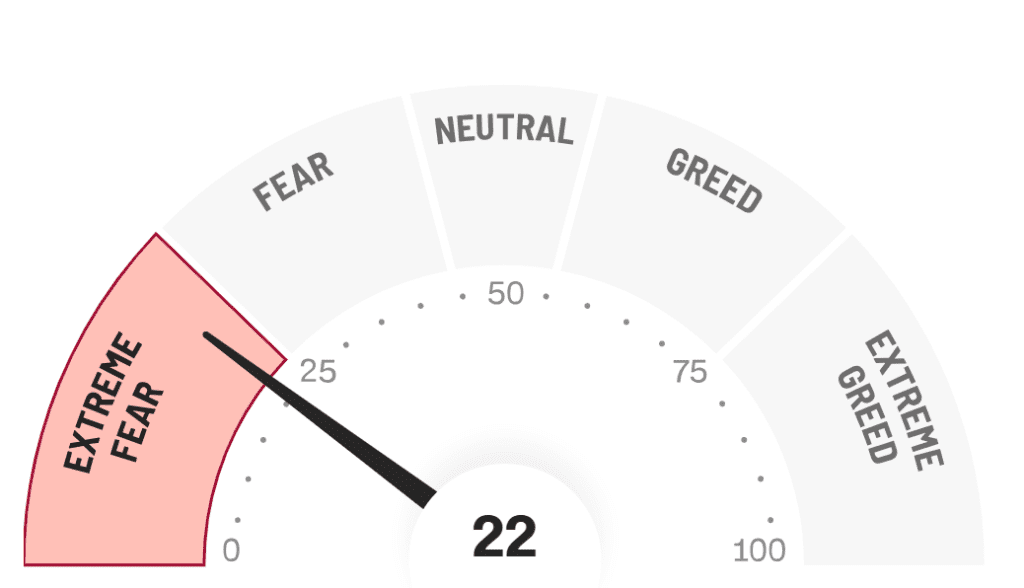

The CNN Fear & Greed Index dropped into “Extreme Fear” territory — a stark reversal from last week’s neutral readings.

Overnight: Asia and Europe Join the Selloff

The risk-off tone intensified overnight:

- Nikkei 225: −2.9% (biggest drop since April’s “Liberation Day” tariff shock)

- KOSPI: −2.3%

- SoftBank Group: −10.9%

- Samsung Electronics: −3.9%

- SK Hynix: −9.2%

In Europe, futures are pointing lower:

- DAX: −0.6%

- FTSE 100: −0.3%

- STOXX 600: −0.7%

But the outlook for European corporate health has substantially improved, the latest earnings forecasts showed on Tuesday, as fears of poor quarterly results have not been realised.

European firms are expected to report growth of 4.3% in third-quarter earnings, on average, according to LSEG I/B/E/S data, above the 0.4% increase analysts expected a week ago.

US stock futures mostly dropped Wednesday morning following a rough trading session that saw all three major averages close deeply in the red.

Dow Jones Industrial Average futures inched up 0.1%, while S&P 500 futures dropped 0.1%. Nasdaq 100 futures sank around 0.3%, as AI chip giant AMD (AMD) saw its shares fall over 3% after its fourth-quarter guidance beat estimates but still underwhelmed.

Safe-haven assets gained traction, gold rose to $3,962/oz, 10-year Treasury yields eased below 4.1%, and the yen strengthened modestly.

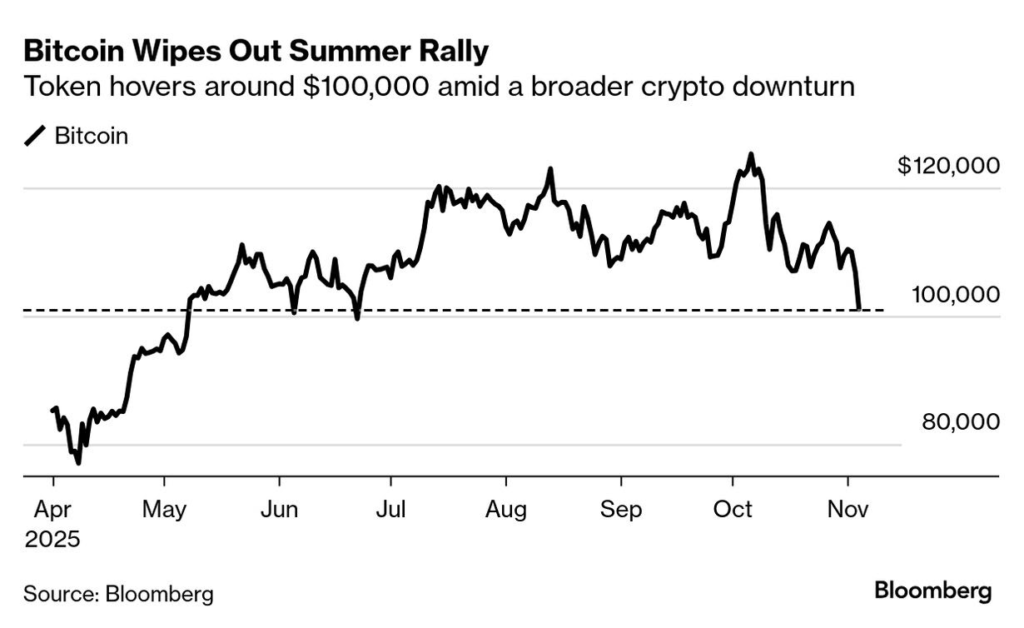

Bitcoin, which briefly broke below $100,000 for the first time since June, rebounded 1.8% to $102,100. It’s now over 20% off its all-time high just a month ago, marking a technical bear market. Ether slumped nearly 10%, while smaller altcoins lost up to 50% year-to-date.

The selloff stems from mid-October liquidations that erased billions in leveraged bets, leaving traders sidelined and open interest in Bitcoin futures well below pre-crash levels. Despite favorable funding rates, few are willing to re-enter. As a result, Bitcoin is up less than 10% in 2025, trailing stocks and once again failing as a portfolio hedge.

Today’s Key Events & Economic Calendar (ET)

| Category | Event / Company | Time (US ET) | Time (UK GMT) |

|---|---|---|---|

| Earnings (Europe) | Marks & Spencer Group, BMW, Novo Nordisk, Enel, Telecom Italia | During EU market hours | 8:00 AM – 5:00 PM |

| Economic Data (US) | ADP Nonfarm Employment Change | 9:15 AM | 2:15 PM |

| ISM Non-Manufacturing PMI / Prices | 10:00 AM | 3:00 PM | |

| S&P Global Composite PMI | 10:45 AM | 3:45 PM | |

| ISM Non-Manufacturing PMI (Final) | 11:00 AM | 4:00 PM | |

| Economic Data (Europe) | Germany: Industrial Orders, Manufacturing O/P, Consumer Goods SA (Sep), HCOB Services & Composite PMI (Oct) | — | Morning (EU) |

| France: Industrial Output (Sep), HCOB Services & Composite PMI (Oct) | — | Morning (EU) | |

| Economic Data (UK) | New Passenger Car Registrations (Oct), S&P Global Services & Composite PMI (Oct), Reserve Assets Total (Oct) | — | 9:00 AM – 1:00 PM |

| Debt Auctions | Germany: 16-year & 19-year Government Bonds | — | 10:00 AM – 12:00 PM |

| Key Event | US Supreme Court Tariff Decision — Expected ruling on legality of Trump’s emergency tariff powers, major potential market mover | 10:00 AM – 12:00 PM | 3:00 PM – 5:00 PM |

Pre-Market Earnings: Aurora Cannabis ($ACB), McDonald’s ($MCD), Unity Software ($U), and Lemonade ($LMND).

After-Market Earnings: AMC Enter ($AMC), Snap ($SNAP), Lucid Gr ($LCID), Robinhood Markets ($HOOD), Qualcomm ($QCOM), IonQ ($IONQ), Lyft ($LYFT), Fastly ($FSLY), ARM Holdings ($ARM), Joby Aviation ($JOBY), and Zevra Therapeutics ($ZVRA).

Meanwhile, the US government shutdown continues into its 35th day, delaying key reports like the official October jobs data, leaving both the Fed and investors “flying blind.”

Sentiment & Outlook

Fear is clearly back: valuations are rich, liquidity is tightening, and volatility is rising.

- Bloomberg’s market breadth data show only one-third of S&P 500 stocks above their 50-day moving average.

- Analysts warn that even strong corporate results may not reverse the risk-off trend until the tariff uncertainty clears.

Markets enter Wednesday in “extreme fear” mode.

The combination of valuation warnings, AI-stock fatigue, a record government shutdown, and today’s Supreme Court tariff case sets the stage for one of the most pivotal trading days of the month.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.